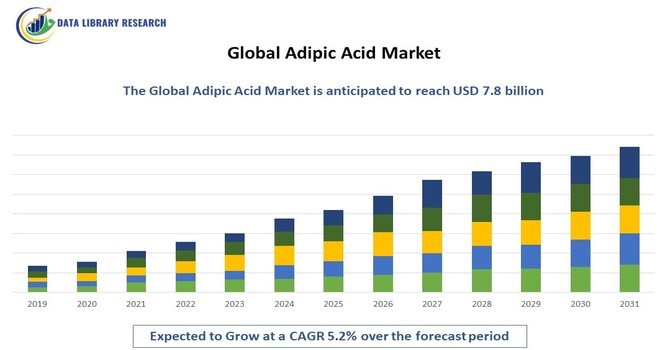

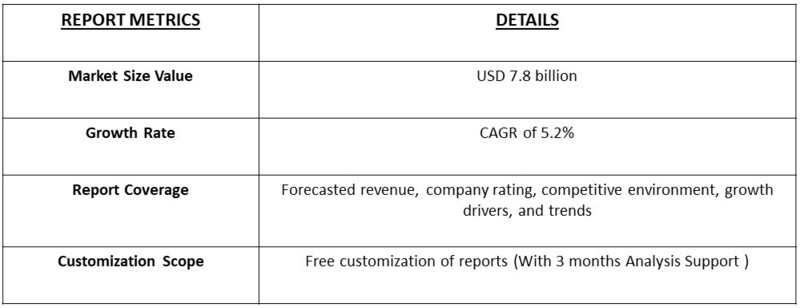

The global adipic acid market was valued at approximately USD 5.2 billion in 2023 and is projected to reach around USD 7.8 billion by 2031, growing at an expected compound annual growth rate (CAGR) of about 5.2% during the forecast period from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

The adipic acid market refers to the global trade and production of adipic acid, a key dicarboxylic acid primarily used in the manufacture of nylon 6,6, polyurethane, and plasticizers. It is a critical raw material in the polymer industry, especially in the production of synthetic fibers and resins. The market is influenced by demand from various end-use industries, including automotive, textiles, and electronics, where adipic acid is integral to the production of high-performance materials. Additionally, the market dynamics are shaped by advancements in bio-based adipic acid and sustainability trends, as companies seek to reduce reliance on petrochemical sources. The market's growth is supported by innovation, industrial expansion, and increasing focus on eco-friendly alternatives.

Key drivers propelling the adipic acid market include the rising demand for nylon 6,6 in automotive and textile industries, where lightweight materials and high-performance fibers are prioritized for fuel efficiency and durability. The growing use of adipic acid in polyurethane foams, particularly in the construction and furniture sectors, further accelerates market demand. Additionally, increasing regulatory pressures to adopt environmentally sustainable practices have driven innovations in bio-based adipic acid production. The expanding electronics and consumer goods industries, where adipic acid-based materials are used for high-quality plasticizers and resins, also contribute to market growth.

Emerging trends in the adipic acid market include a strong shift towards bio-based adipic acid production as industries focus on reducing carbon footprints and embracing sustainability. Technological advancements in nylon production, driven by demand for lightweight and durable materials in the automotive and aerospace sectors, are influencing market dynamics. Additionally, innovations in the development of high-performance polyurethanes and plasticizers are creating new applications for adipic acid. Regulatory policies aimed at reducing emissions and enhancing eco-friendly materials are also accelerating the adoption of green alternatives in the market. Furthermore, the growing interest in circular economy practices is encouraging recycling initiatives in adipic acid-related industries.

Market Segmentation

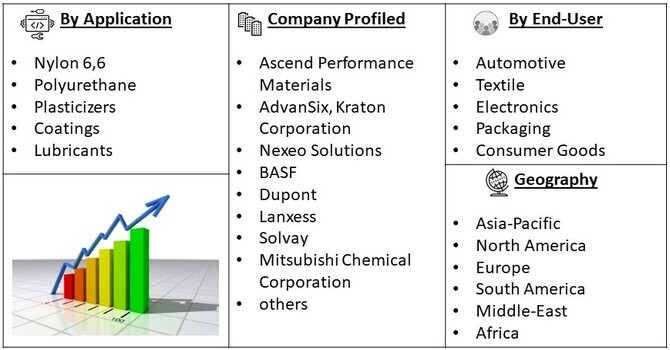

The Global Adipic Acid Market is segmented By Application (Nylon 6,6, Polyurethane, Plasticizers, Coatings, Lubricants) By End-use Industry (Automotive, Textile, Electronics, Packaging, Consumer Goods) and geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report offers the market size and forecasts for revenue (USD million) for all the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The global shift towards lightweight materials in the automotive industry is a key driver of the adipic acid market, as nylon 6,6—one of its primary applications—is widely used in vehicle components to improve fuel efficiency and reduce emissions. As automakers face stringent environmental regulations, particularly in the EU and North America, the demand for high-performance materials like nylon 6,6 is surging. For example, the European Union's push to reduce average CO2 emissions for new cars to 55g/km by 2030 has led to increased usage of nylon in parts such as engine covers, intake manifolds, and airbag containers. Additionally, the industrial sector's focus on enhancing durability and performance in high-stress environments further boosts demand for nylon-based materials, positioning adipic acid as a critical input in these innovations.

With the global movement towards sustainability, there is a notable shift towards bio-based adipic acid production, driven by consumer and regulatory pressures for greener alternatives. Bio-based adipic acid, derived from renewable sources like glucose, is gaining traction as companies seek to reduce their carbon footprints. For instance, industry leaders like Cathay Industrial Biotech and Verdezyne have made significant investments in developing bio-based processes, which have now reached commercial scale. Governments are also encouraging this transition, with countries like Germany offering subsidies for bio-based chemical production. As a result, bio-based adipic acid is expected to account for a growing share of the market, supported by increasing end-user demand from sectors such as consumer goods and packaging, which prioritize eco-friendly raw materials.

Market Restraints

A significant restraint for the adipic acid market is the volatility in raw material prices, particularly petroleum-based feedstocks such as cyclohexane, which are subject to fluctuations in crude oil prices. This creates uncertainty for manufacturers, affecting profit margins and pricing strategies. For instance, during the oil price shocks of 2022, driven by geopolitical tensions such as the Russia-Ukraine conflict, the cost of petroleum derivatives spiked, leading to increased production costs for adipic acid. Moreover, supply chain disruptions, exacerbated by events like the COVID-19 pandemic, have led to delays in sourcing critical raw materials, further straining the market. These challenges are particularly pressing in regions reliant on imported feedstocks, such as Europe and Asia-Pacific, making the industry more vulnerable to global market dynamics.

The COVID-19 pandemic had a mixed impact on the global adipic acid market. On one hand, disruptions in supply chains, factory shutdowns, and reduced industrial activity, particularly in the automotive and textile sectors, led to a temporary decline in demand for nylon 6,6 and polyurethane applications. Key markets in Europe and North America witnessed significant slowdowns in production, while logistical challenges further exacerbated delays. On the other hand, the demand for medical supplies and protective equipment, which use adipic acid-based materials, saw a spike, partially offsetting the downturn. As economies recovered post-pandemic, the market began to stabilize, with a renewed focus on bio-based adipic acid solutions as companies shifted towards more sustainable and resilient supply chains.

Segmental Analysis

Bio-based adipic acid is gaining significant momentum as industries shift towards more sustainable chemical processes. This segment is driven by the rising environmental concerns and regulatory pressures to reduce carbon emissions and reliance on fossil fuels. Companies like Verdezyne and Rennovia have been pioneering in developing bio-based adipic acid derived from renewable resources such as plant sugars, offering a greener alternative to the traditional petroleum-based process. For example, Verdezyne successfully produced bio-adipic acid through fermentation processes, which could help companies meet sustainability targets. Government policies, particularly in the EU and the US, are fostering bio-based chemical production by offering incentives and subsidies. With increasing consumer demand for eco-friendly products in sectors like textiles, automotive, and packaging, bio-based adipic acid is poised for rapid growth. The market is also influenced by advancements in biotechnology, improving the cost-competitiveness and scalability of bio-based processes, making it an attractive option for manufacturers.

Nylon 6,6, which relies on adipic acid as a core ingredient, remains a key growth area within the market, particularly driven by its extensive use in the automotive and textile industries. The demand for nylon 6,6 in automotive applications continues to rise due to its lightweight, high-strength properties, which help manufacturers meet fuel efficiency and emission reduction targets. For instance, major automakers like BMW and Ford have increasingly integrated nylon 6,6 into vehicle components such as airbags, engine covers, and electrical connectors, aligning with stricter environmental regulations, particularly in Europe. The textile industry also sees sustained demand for nylon 6,6 in durable clothing and performance fabrics. Technological advancements in polymer processing, coupled with increasing investments in expanding production capacities—such as Invista’s multi-million-dollar investments in China to boost nylon 6,6 output—are further driving this segment. As global industrial activity rebounds post-pandemic, the nylon 6,6 sub-segment is expected to experience significant growth.

The Asia-Pacific region is poised for substantial growth in the adipic acid market, driven by rapid industrialization, urbanization, and increasing demand from key end-use sectors such as automotive, textiles, and consumer goods. Countries like China and India, with their expanding manufacturing bases and rising middle-class populations, are major contributors to this growth. China, as the largest producer and consumer of adipic acid, continues to invest heavily in expanding its production capacity to meet domestic demand and export needs. For example, companies such as Shandong Haili Chemical have scaled up production to cater to the growing automotive and textile sectors. Additionally, the region’s growing focus on sustainable solutions is fostering the development of bio-based adipic acid, supported by government policies promoting green technologies. The increasing adoption of electric vehicles (EVs) in countries like Japan and South Korea, where lightweight materials like nylon 6,6 are critical for EV efficiency, further drives demand. These factors, combined with rising infrastructure development, position Asia-Pacific as a key growth region for the adipic acid market.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the global adipic acid market is characterized by a mix of established players and emerging companies focused on innovation and sustainability. The established players in the global adipic acid market, such as BASF, DuPont, and INVISTA, dominate through their extensive manufacturing capabilities and well-established supply chains. These companies leverage their experience and resources to invest heavily in research and development, aiming to innovate and enhance production processes. Their strong market presence allows them to maintain competitive pricing while ensuring consistent quality. Additionally, these players are increasingly focusing on sustainability initiatives, such as developing bio-based adipic acid alternatives and optimizing production methods to reduce environmental impact, aligning their strategies with the growing demand for eco-friendly chemicals.

Key competitors include

Recent Development

Q1. What are the primary drivers of the Antimicrobial Textiles market?

The antimicrobial textiles market is primarily driven by the increasing awareness of hygiene and infection control, particularly in healthcare settings and public spaces. The rise in healthcare-associated infections (HAIs) has created a demand for fabrics that can inhibit microbial growth, making antimicrobial textiles essential for hospitals and clinics. Additionally, the growing trend towards active lifestyles has spurred interest in antimicrobial sportswear, which helps minimize odors and enhance comfort. Environmental concerns and the desire for sustainable solutions are also driving innovation in this sector, as manufacturers seek eco-friendly antimicrobial agents and processes.

Q2. Which segment is anticipated to hold the largest market share?

The healthcare segment is anticipated to hold the largest market share in the antimicrobial textiles market, fueled by the critical need for infection prevention and control. Hospitals and medical facilities require textiles that resist microbial growth to significantly reduce the risk of HAIs. Antimicrobial bed linens, surgical gowns, and protective clothing are in high demand, as they contribute to maintaining a sterile environment. The ongoing focus on patient safety and the adoption of stringent hygiene protocols further bolster the growth of this segment, making it a key driver in the overall market landscape.

Q3. What challenges does the market face?

The antimicrobial textiles market faces several challenges, including regulatory hurdles related to the safety and efficacy of antimicrobial agents used in textiles. Concerns over antimicrobial resistance and the environmental impact of chemical treatments are becoming more prominent. Additionally, the market is characterized by intense competition and rapid technological advancements, which necessitate continuous innovation from manufacturers. These factors can lead to increased costs and complicate the product development process, making it essential for companies to stay ahead in terms of research and regulatory compliance.

Q4. Which region is expected to hold the largest share of the market?

North America is expected to hold the largest share of the antimicrobial textiles market, driven by its advanced healthcare infrastructure and high standards for hygiene and infection control. The region benefits from significant investment in research and development, which fosters innovation in antimicrobial technologies. Strong regulatory frameworks support the adoption of antimicrobial textiles across various sectors, including healthcare, hospitality, and consumer products. Additionally, growing consumer awareness and demand for high-quality, safe textiles contribute to the region's dominance in the market.

Q5. Who are the prominent players in the market?

Key players in the antimicrobial textiles market include DuPont, 3M, and Milliken & Company, known for their extensive research and development capabilities and strong market presence. Other notable companies include BASF, Ahlstrom-Munksjö, and Trevira, all of which are actively engaged in advancing antimicrobial technologies. These companies focus on innovation, quality, and sustainability, aiming to meet the evolving needs of consumers and industries. Strategic partnerships, mergers, and acquisitions are also common among these players as they seek to enhance their market share and expand their product offerings.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model