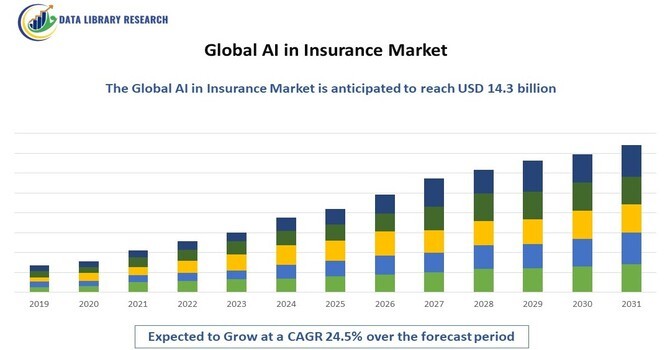

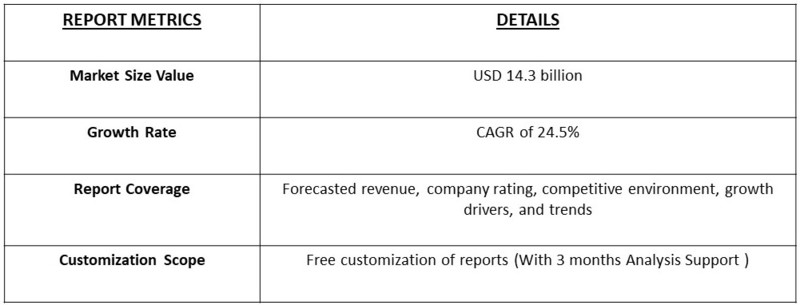

The global AI in Insurance market is expected to reach a market value of 2.4 billion in 2023, , market is projected to reach a value of 14.3 billion, with a CAGR of 24.5% from 2023 to 2031.

Get a Complete Analysis Of The Report - Download a Free Sample PDF

The Global AI in Insurance Market refers to the rapidly expanding adoption of artificial intelligence technologies within the insurance industry, aimed at enhancing operational efficiencies, customer experiences, and risk assessment models. Key AI applications include claims processing automation, fraud detection, underwriting, and personalized customer interactions. With increasing pressure for digital transformation and cost reduction, insurers are leveraging AI to streamline workflows, reduce human error, and offer more accurate pricing models. The market is expected to witness significant growth as AI continues to reshape the insurance landscape, driven by advancements in machine learning, predictive analytics, and natural language processing.

Global AI in Insurance Market is the industry's growing demand for operational efficiency and cost optimization. Insurers are increasingly adopting AI-driven automation to streamline claims processing, underwriting, and fraud detection, significantly reducing processing time and human error. Additionally, AI enhances customer experience through personalized interactions and predictive analytics, driving customer retention and satisfaction. Regulatory requirements for improved risk assessment and transparency further push insurers to leverage AI solutions. The rapid advancements in machine learning and data analytics also fuel innovation, making AI a critical tool for competitive differentiation.

The global AI in Insurance market is poised for exponential growth, driven by the increasing adoption of artificial intelligence and machine learning technologies. Key trends include the rise of cloud-based AI platforms, enabling insurers to scale their operations and reduce costs. Additionally, the market is witnessing a surge in the use of natural language processing (NLP) and computer vision to enhance customer experience and improve claims processing efficiency. Furthermore, the integration of IoT and AI is expected to revolutionize the way insurers assess and price risks. As the market continues to evolve, we anticipate a growing focus on Explainable AI (XAI) to ensure transparency and trust among customers.

For Detailed Market Segmentation - Get a Free Sample PDF

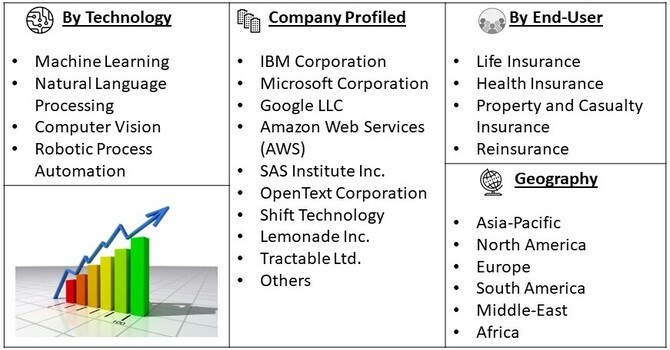

The Global AI in Insurance market is segmented By Component (Software, Services) By Technology (Machine Learning, Natural Language Processing, Computer Vision, Robotic Process Automation) By End User (Life Insurance, Health Insurance, Property and Casualty Insurance, Reinsurance) and geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report offers the market size and forecasts for revenue (USD million) for all the above segments.

The global AI in Insurance market is driven by the growing demand for personalized customer experiences. Insurers are recognizing the need to leverage AI-powered chatbots and virtual assistants to provide 24/7 support, enabling customers to access information and services at their convenience. For instance, AXA's chatbot, AXA Chat, has seen a 30% increase in customer engagement since its launch. Similarly, Allstate's virtual assistant, Allstate Digital, has reduced customer service calls by 20%. As customers become increasingly tech-savvy, insurers that adopt AI-powered customer experience solutions will be better equipped to retain customers and drive growth.

The proliferation of big data and analytics is another key driver of the global AI in Insurance market. Insurers are generating vast amounts of data from various sources, including IoT devices, social media, and claims data. By leveraging AI-powered analytics, insurers can gain insights into customer behavior, identify patterns, and make data-driven decisions. For instance, Liberty Mutual's data analytics platform has enabled the insurer to reduce claims costs by 15% and improve customer satisfaction by 20%. As data continues to grow in importance, insurers that can effectively harness AI-powered analytics will be well-positioned to gain a competitive edge.

One of the key restraints in the global AI in Insurance market is the concern over data quality and security. Insurers are grappling with the challenge of ensuring the accuracy, completeness, and integrity of their data, which is critical for AI-powered analytics and decision-making. Moreover, the increasing reliance on cloud-based solutions and IoT devices has raised concerns over data breaches and cyber attacks. For instance, a recent study by Accenture found that 70% of insurers are concerned about the security of their data in the cloud. As a result, insurers must invest in robust data governance and security measures to ensure the trustworthiness of their data and mitigate the risk of reputational damage.

The COVID-19 pandemic accelerated the adoption of AI in the insurance market as insurers faced increased claims volume, operational disruptions, and a need for remote customer engagement. AI-driven solutions helped streamline claims processing, enhance fraud detection, and improve digital customer interactions. The shift toward digitalization and automation became more urgent, prompting insurers to invest heavily in AI technologies to maintain operational efficiency and ensure business continuity. This surge in AI adoption is expected to have a lasting impact on the industry's digital transformation efforts.

Natural Language Processing (NLP) in the insurance sector has gained significant momentum, with insurers leveraging AI-driven chatbots, virtual assistants, and automated document analysis tools to enhance customer service and streamline operations. NLP enables the interpretation of unstructured text data, such as customer emails, claims reports, and policy documents, allowing insurers to automate responses and categorize inquiries. One notable development is the integration of NLP in call centers, reducing human intervention and allowing 24/7 customer support. Companies like Lemonade and Progressive have incorporated NLP to handle claims inquiries and policy changes with minimal manual input. The driving factors include rising customer expectations for fast, accurate responses, the growing need for cost reduction in customer service operations, and advancements in AI algorithms that improve NLP accuracy. The pandemic further accelerated NLP adoption as insurers were forced to scale remote services and automate customer interactions.

The adoption of AI for claims processing is transforming the insurance industry by automating labor-intensive tasks such as document verification, damage assessment, and payment approvals. Real-time AI tools can now assess damage through image recognition, reducing the time needed for manual inspections and accelerating the settlement process. Companies like Zurich and Allianz have implemented AI-driven claims automation, allowing faster processing and improving customer satisfaction. AI is also used to detect potential fraud during claims processing, minimizing losses. Driving factors for this sub-segment include the growing volume of insurance claims, increasing pressure to reduce processing times, and the need for enhanced fraud detection mechanisms. The integration of AI in claims processing not only improves efficiency but also helps insurers reduce operational costs and improve decision-making accuracy.

The Asia-Pacific region is expected to witness significant growth in the AI in Insurance market over the forecast period due to several key factors. Rapid digital transformation across emerging economies such as China, India, and Southeast Asian countries is driving the adoption of AI technologies in the insurance sector. Increasing internet penetration, smartphone usage, and the growing popularity of digital insurance platforms are pushing insurers to invest in AI-driven solutions for customer service, claims processing, and fraud detection. Governments in the region are also supporting AI adoption through favorable policies and initiatives promoting innovation and digitalization. Additionally, a rising middle-class population and growing awareness of insurance products are fueling demand for AI-enabled insurance solutions that provide personalized offerings and seamless customer experiences. These factors, combined with ongoing technological advancements and the expansion of cloud infrastructure, are expected to propel the AI in Insurance market across the Asia-Pacific region.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global AI in Insurance market is characterized by the presence of several established technology firms, insurance providers, and AI-focused startups, all competing to deliver advanced solutions across claims processing, underwriting, fraud detection, and customer service. Major players are increasingly focusing on partnerships, acquisitions, and the development of proprietary AI tools to differentiate their offerings and capture market share.

Key competitors in the market include

Recent Development

Q1. What are the driving factors for the Global AI in Insurance Market?

The Global AI in Insurance Market is primarily driven by the increasing need for operational efficiency and cost reduction within the insurance sector. AI technologies, such as machine learning and natural language processing, enable insurers to automate claims processing, underwriting, and customer service, significantly speeding up these processes. Additionally, AI enhances risk assessment and fraud detection, allowing insurers to improve their decision-making capabilities. The growing volume of data generated in the insurance industry also necessitates advanced analytics, which AI can provide. Furthermore, the rising demand for personalized customer experiences is pushing insurers to leverage AI to tailor products and services to individual customer needs.

Q2. What are the restraining factors for the Global AI in Insurance Market?

Despite its potential, the Global AI in Insurance Market faces several restraining factors. One significant challenge is the high initial investment required to implement AI technologies, which may deter smaller insurance companies with limited budgets. Concerns about data privacy and security are also critical, as the insurance sector deals with sensitive personal information, making regulatory compliance paramount. Additionally, the lack of skilled workforce capable of developing and managing AI systems can hinder adoption. There is also resistance to change from traditional insurance practices, which may slow the integration of AI solutions in some organizations. Moreover, the complexity of AI systems can create operational challenges during implementation.

Q3. Which segment is projected to hold the largest share in the Market?

The claims management segment is projected to hold the largest share in the Global AI in Insurance Market. This segment benefits from the significant potential of AI technologies to streamline and automate claims processing, leading to faster resolution times and improved customer satisfaction. AI-driven systems can analyze claims data, detect fraudulent activities, and assess damages more efficiently than traditional methods. As insurers increasingly focus on enhancing the claims experience for customers and reducing operational costs, the claims management segment is expected to continue dominating the market.

Q4. Which region holds the largest share in the Global AI in Insurance Market?

North America currently holds the largest share in the Global AI in Insurance Market, driven by the presence of major insurance companies and a robust technological infrastructure. The region is a leader in adopting advanced technologies, including AI, to enhance operational efficiency and customer experience. Additionally, regulatory support and a competitive landscape encourage innovation in the insurance sector. While Europe and Asia-Pacific are also growing rapidly in adopting AI solutions, North America’s established market, coupled with high investment in technology, positions it as the leading region in the AI in insurance landscape.

Q5. Which are the prominent players in the Global AI in Insurance Market?

Prominent players in the Global AI in Insurance Market include IBM, which offers AI-driven analytics and solutions tailored for the insurance industry. Salesforce is notable for its customer relationship management (CRM) platforms that incorporate AI capabilities to enhance customer engagement. Lemonade, a tech-driven insurance company, leverages AI to streamline the entire insurance process. Zebra Technologies focuses on data analytics and AI to improve claims management. Other significant players include Cognizant, Accenture, and Capgemini, all of which provide consulting and technology services to help insurers implement AI solutions. These companies are continuously innovating to meet the evolving needs of the insurance industry.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model