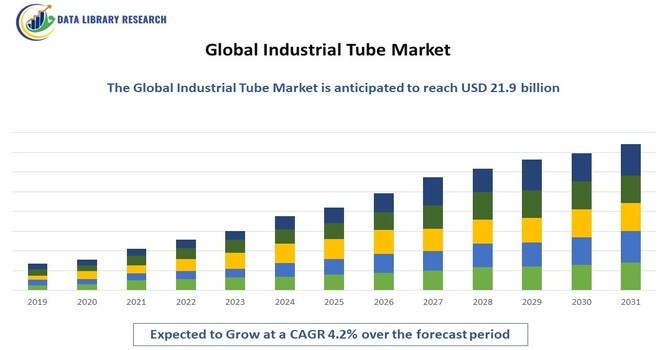

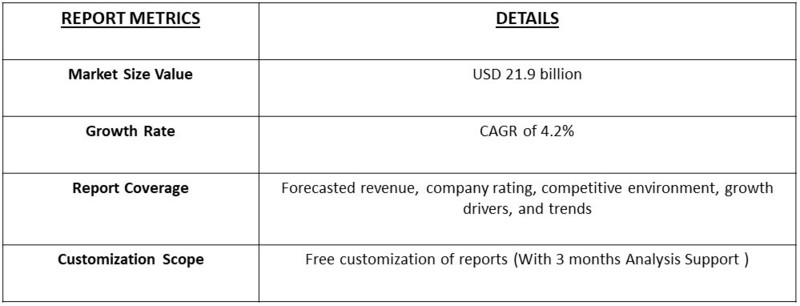

According to recent market research, the Global Industrial Tube Market is projected to reach a market value of USD 14.8 billion in 2023, growing at a compound annual growth rate (CAGR) of 4.2% from 2023 to 2031, reaching to USD 21.9 billion by 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

The Industrial Tube Market encompasses the production and distribution of tubular products used in various industrial applications, including manufacturing, construction, and automotive sectors. These tubes are typically made from materials such as steel, aluminum, plastic, and copper, and are utilized for conveying fluids, structural support, and mechanical components. The market is driven by the demand for lightweight, high-strength materials that enhance operational efficiency and reduce production costs. Technological advancements in manufacturing processes, such as precision tube forming and automated welding, are also contributing to market growth. Increasing infrastructure development and industrial activities globally further bolster the demand for industrial tubes.

Industrial Tube Market include the growing demand for infrastructure development, which requires robust and reliable tubular products for construction and manufacturing applications. The increasing emphasis on energy efficiency and lightweight materials across industries, particularly in automotive and aerospace sectors, is driving the adoption of high-strength, lightweight tubes. Additionally, advancements in manufacturing technologies are enhancing production capabilities and reducing costs, further stimulating market growth. The rise in industrial automation and the need for efficient fluid transport systems also contribute to the demand for industrial tubes. Finally, regulatory standards promoting safety and quality in construction and manufacturing processes are propelling the market forward.

The Industrial Tube Market is witnessing a paradigm shift towards sustainable and eco-friendly solutions, driven by increasing environmental concerns and regulatory pressures. Key trends shaping the market include the adoption of advanced materials such as high-strength, high-temperature, and corrosion-resistant alloys, as well as the growing demand for precision-engineered tubes with complex geometries. Additionally, the market is seeing a trend towards digitalization, with the integration of Industry 4.0 technologies such as IoT, AI, and data analytics to optimize tube manufacturing and inspection processes. Furthermore, the market is also witnessing a shift towards regionalization, with manufacturers focusing on local production to reduce logistics costs and improve supply chain efficiency.

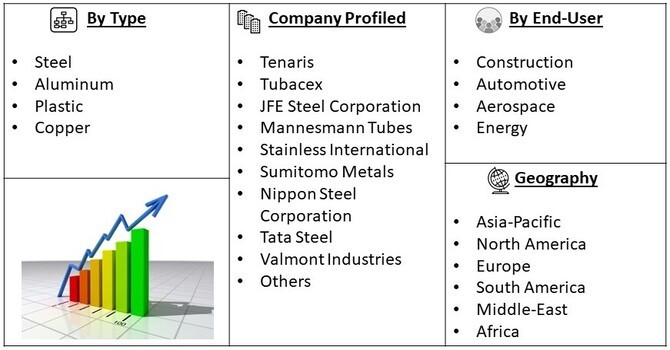

The Global Industrial Tube Market is segmented by Material Type (Steel, Aluminum, Plastic, Copper) End-use Industry (Construction, Automotive, Aerospace, Energy) and geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report offers the market size and forecasts for revenue (USD million) for all the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

The Industrial Tube Market is being driven by the growing demand for oil and gas exploration and production. The increasing global energy demand and the need for sustainable energy sources are driving the growth of the oil and gas industry, leading to a surge in demand for industrial tubes used in drilling, extraction, and transportation of oil and gas. According to the International Energy Agency, global oil and gas production is expected to increase by 10% by 2025, driving the demand for industrial tubes. As a result, tube manufacturers are investing in research and development to develop high-strength, high-temperature, and corrosion-resistant alloys that can withstand the harsh conditions of oil and gas exploration. Advancements in material science and manufacturing technologies

The development of new materials such as advanced high-strength steel, titanium, and ceramic composites is enabling the production of tubes with improved strength, corrosion resistance, and durability. Additionally, advancements in manufacturing technologies such as 3D printing, laser cutting, and robotic welding are improving the efficiency and precision of tube manufacturing processes. According to a recent survey, 70% of tube manufacturers reported that advancements in materials science and manufacturing technologies were key drivers of growth in the market.

One of the key restraints in the Industrial Tube Market is the fluctuating raw material prices, which can significantly impact the cost of production and profitability of tube manufacturers. The prices of raw materials such as steel, copper, and aluminum are subject to fluctuations in global demand and supply, which can lead to price volatility. According to a recent report, the prices of steel, for example, have increased by 15% in the past year, driven by increased demand from the construction and automotive industries. This price volatility can make it challenging for tube manufacturers to maintain stable production costs and pricing, which can impact their competitiveness in the market. As a result, tube manufacturers are focusing on developing strategies to mitigate the impact of raw material price fluctuations, such as diversifying their raw material suppliers and investing in cost-reduction initiatives.

The COVID-19 pandemic significantly affected the Industrial Tube Market, initially causing disruptions in production and supply chains due to lockdowns and restrictions. Key sectors like construction, automotive, and energy faced project delays and reduced demand, leading to a slowdown in sales. However, as restrictions eased, a rebound in industrial activity emerged, driven by increased government investments in infrastructure and the recovery of the automotive sector. The pandemic also accelerated trends toward automation and digitalization, prompting manufacturers to enhance operational efficiency. Overall, while the market faced challenges during the peak of the pandemic, it showed resilience and adaptability, positioning itself for future growth.

The steel tube sub-segment is a cornerstone of the Industrial Tube Market, known for its strength, durability, and versatility across various applications. Steel tubes are widely used in construction for structural supports, in automotive for frames and exhaust systems, and in oil and gas for pipelines. Recent developments include advancements in high-strength low-alloy (HSLA) steels, which provide improved performance while reducing weight. Additionally, the increasing focus on sustainability has driven the adoption of recycled steel in manufacturing processes, aligning with global environmental goals. The demand for steel tubes is primarily driven by the rapid growth in the construction sector, infrastructure projects, and automotive production, especially with the rise of electric vehicles, which require innovative lightweight solutions.

The aluminum tube sub-segment is experiencing significant growth due to aluminum's lightweight nature and corrosion resistance, making it ideal for applications in the automotive, aerospace, and construction industries. Recent innovations include the development of aluminum alloys that enhance strength while maintaining a low weight, crucial for improving fuel efficiency in vehicles. The shift towards electric vehicles (EVs) has further accelerated demand for aluminum tubes, as manufacturers seek to reduce the weight of battery enclosures and structural components. Driving factors include increasing regulatory pressures for emissions reductions, the need for sustainable materials, and the expansion of infrastructure projects across emerging markets. The aluminum tube segment is well-positioned to benefit from these trends, contributing to the overall growth of the Industrial Tube Market.

The Asia-Pacific region is projected to witness significant growth in the Industrial Tube Market over the forecast period, driven by rapid urbanization, industrialization, and increasing infrastructure development. Countries like China, India, and Japan are leading this growth, supported by substantial investments in construction, energy, and automotive sectors. The ongoing expansion of the manufacturing base and a rising middle-class population are fueling demand for various industrial applications. Additionally, government initiatives aimed at enhancing infrastructure and promoting renewable energy sources are creating new opportunities for the industrial tube sector. The growing trend towards lightweight materials in industries such as automotive and aerospace further drives the demand for specialized tubes. With a robust economic outlook, the Asia-Pacific region is poised to become a key player in the global industrial tube market.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Industrial Tube Market is characterized by a mix of established players and emerging companies focused on innovation and meeting diverse customer needs. Key manufacturers are investing in advanced manufacturing technologies and sustainable practices to enhance product quality and operational efficiency. The market is driven by increasing demand across sectors such as construction, automotive, and energy, prompting companies to expand their production capacities and diversify their product offerings.

Major competitors in the market include

Recent Development

Q1. What are the driving factors for the Global Industrial Tube Market?

The Global Industrial Tube Market is primarily driven by the increasing demand for tubes across various end-use industries, including automotive, construction, and manufacturing. The growth in infrastructure development and urbanization globally has led to a surge in demand for steel and plastic tubes for applications such as plumbing, HVAC systems, and structural support. Additionally, advancements in manufacturing technologies, including precision machining and enhanced material properties, are facilitating the production of high-quality tubes that meet industry standards. The rising focus on lightweight materials in the automotive sector, coupled with the growing emphasis on energy efficiency and sustainability, is also propelling market growth. Moreover, the expansion of the oil and gas industry necessitates durable and reliable tubing solutions, further driving demand.

Q2. What are the restraining factors for the Global Industrial Tube Market?

Despite its growth potential, the Global Industrial Tube Market faces several restraining factors. One major challenge is the volatility in raw material prices, particularly for metals like steel and aluminum, which can impact production costs and profit margins. Additionally, the market is sensitive to economic fluctuations, and any downturn in manufacturing or construction activities can lead to reduced demand for industrial tubes. Stringent environmental regulations regarding emissions and waste disposal can also increase operational costs for manufacturers. Moreover, competition from alternative materials, such as composites and polymers, may limit the growth of traditional metal tube applications. Lastly, the global supply chain disruptions, exacerbated by events like the COVID-19 pandemic, can affect availability and pricing of raw materials.

Q3. Which segment is projected to hold the largest share in the Market?

The steel tube segment is projected to hold the largest share in the Global Industrial Tube Market. Steel tubes are widely used across various industries due to their strength, durability, and resistance to corrosion, making them suitable for applications in construction, automotive, and oil and gas sectors. The versatility of steel tubes, combined with their ability to be customized for specific applications, enhances their demand in both structural and mechanical applications. As industries continue to focus on building robust and long-lasting infrastructure, the steel tube segment is expected to maintain its dominant position in the market.

Q4. Which region holds the largest share in the Global Industrial Tube Market?

North America currently holds the largest share in the Global Industrial Tube Market, driven by a well-established manufacturing sector and significant investments in infrastructure development. The region's strong automotive and aerospace industries contribute to the high demand for industrial tubes, particularly steel and aluminum variants. Additionally, ongoing projects in construction and energy sectors further bolster the market. While Europe and Asia-Pacific are also important regions for industrial tube demand, North America's advanced technological capabilities and focus on innovation position it as the leader in this market.

Q5. Which are the prominent players in the Global Industrial Tube Market?

Prominent players in the Global Industrial Tube Market include Tenaris, a leading manufacturer of steel tubes for the energy industry. Tube Supply specializes in providing a wide range of tubing products for various applications. U.S. Steel is known for its extensive portfolio of steel products, including industrial tubes. Tata Steel offers innovative steel solutions for diverse industries. Other significant players include Zekelman Industries, Nucor Corporation, and JFE Steel Corporation, which focus on high-quality tube manufacturing. Additionally, Alcoa Corporation plays a vital role in the aluminum tube segment. These companies are continually investing in technology and innovation to enhance their product offerings and meet the evolving needs of their customers.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model