Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Cold Chain Food Safety Testing Service Market involves testing and monitoring food products kept at controlled temperatures during storage and transport. It ensures food safety, quality, and compliance with regulations by detecting contaminants or spoilage, supporting industries like dairy, meat, seafood, and frozen foods worldwide. The increase demand for temperature-controlled testing and monitoring across the supply chain. Heightened regulatory scrutiny and stricter food-safety standards worldwide together with more frequent high-profile recalls and outbreaks are forcing producers, importers and retailers to invest more in third-party testing and certification to maintain compliance and protect brand value.

The Global Cold Chain Food Safety Testing Service Market is rapidly evolving with advancements like real-time IoT monitoring, which tracks temperature, humidity, and other conditions to trigger instant alerts for deviations. AI, machine learning, and predictive analytics enhance spoilage prediction and route optimization, while blockchain ensures transparent end-to-end traceability. On-site rapid testing technologies—such as portable kits, lab-on-a-chip devices, and CRISPR-based sensors—enable faster contamination detection, reducing reliance on central labs. Additionally, sustainability and eco-friendly cold chain practices are gaining momentum, driving efficiency, reducing waste, and strengthening global food safety and consumer trust.

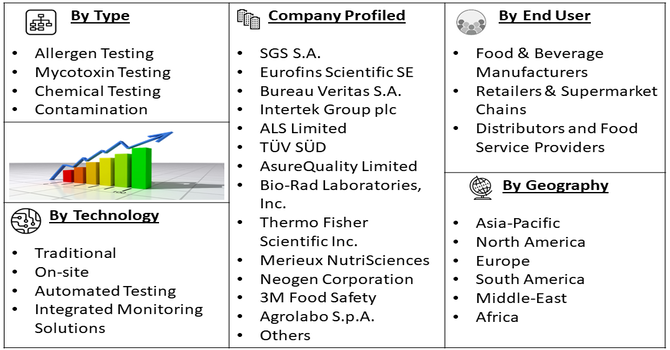

Segmentation: Global Cold Chain Food Safety Testing Service Market is segmented By Type of Test (Allergen Testing, Mycotoxin Testing, Chemical Testing, Contamination), Food (Meat & Poultry, Seafood / Aquatic Products, Dairy Products, Fruits & Vegetables, Frozen Foods, Delicatessen), Technology (Traditional, On-site, Automated Testing, and Integrated Monitoring Solutions), End-User (Food & Beverage Manufacturers, Retailers & Supermarket Chains, Distributors, and Food Service Providers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The key drivers propelling the Global Cold Chain Food Safety Testing Service Market is the tightening of international food safety standards and regulatory frameworks. Governments and global agencies such as the FDA (U.S.), FSSAI (India) are enforcing strict compliance for temperature-sensitive products, requiring regular microbial, chemical, and contaminant testing throughout the cold chain.

For instance, in February 2024, the CDC reported that about 48 million Americans suffered from foodborne illnesses each year, with 128,000 hospitalizations and 3,000 deaths—highlighting a largely preventable public health issue. The FDA’s Food Safety Modernization Act (FSMA) addressed this challenge by shifting the U.S. food safety system from reactive responses to preventive measures, establishing clear standards across every stage of the global food supply chain. This increasing regulatory rigor, mirrored by similar initiatives worldwide, led to the rising stringency of global food safety regulations. As a result, it drove higher demand for advanced cold chain food safety testing services, as companies worked to ensure compliance, traceability, and real-time monitoring to prevent contamination and protect consumers. This regulatory pressure compels manufacturers, distributors, and retailers to partner with accredited laboratories and third-party testing providers to ensure compliance and prevent costly recalls or bans.

The increasing international trade in perishable goods—such as seafood, dairy, meat, fruits, and vegetables—combined with the rapid expansion of cold chain infrastructure is significantly driving market growth. As global supply chains become more complex, ensuring consistent temperature control and contamination prevention across multiple nodes has become critical. The surge in e-commerce grocery delivery, frozen food consumption, and ready-to-eat meals also heightens the need for continuous testing to verify product integrity during transport and storage. For instance, in February 2025, Maersk announced its fourth U.S. cold-storage warehouse near the Port of New York and New Jersey, which boosted demand for cold chain food safety testing services to ensure product quality and compliance. Consequently, rising cold chain volumes directly translate into higher testing frequency, bolstering demand for advanced, rapid, and integrated food safety testing services.

Market Restraints:

Another significant challenge is the lack of uniform global standards and testing protocols across countries, which creates inconsistencies in testing outcomes and complicates international trade compliance. Variations in sample collection methods, permissible contamination levels, and certification norms can delay clearance and increase administrative burdens. Moreover, there is a shortage of trained professionals with expertise in advanced testing technologies such as PCR-based assays, next-generation sequencing, and rapid diagnostics. This skills gap limits the capacity and scalability of testing service providers, especially in emerging markets, restraining the overall growth potential of the cold chain food safety testing industry.

The Global Cold Chain Food Safety Testing Service Market had a significant socio-economic impact by enhancing food security, reducing waste, and supporting public health worldwide. By ensuring the safety and quality of temperature-sensitive foods, it minimized losses from spoilage and contamination, leading to greater consumer confidence and fewer foodborne illnesses. Economically, it created jobs across testing laboratories, logistics, and technology sectors while encouraging innovation in sensors, diagnostics, and data analytics. Developing nations benefited through improved export capabilities and compliance with international safety standards, boosting trade opportunities. Overall, the market played a key role in strengthening food supply resilience, protecting livelihoods, and promoting sustainable growth across the global food and logistics ecosystem.

Segmental Analysis:

This growth is primarily driven by the increasing occurrence of chemical contaminants such as pesticide residues, antibiotics, preservatives, and heavy metals in perishable and frozen food products. As consumers and regulators become more aware of the health risks associated with chemical exposure, stringent safety regulations are being enforced globally to ensure compliance with maximum residue limits (MRLs). Consequently, food producers and exporters are investing heavily in advanced chemical testing methods such as chromatography, spectrometry, and rapid detection kits to verify the purity and safety of their products. Moreover, the expanding international trade of frozen and processed foods, coupled with growing consumer demand for transparency and clean-label products, is further fueling the adoption of chemical testing across the cold chain. This segment’s growth is also supported by the integration of automated testing platforms and real-time analytics, enabling faster, more precise detection of chemical hazards and enhancing overall food safety assurance.

This growth is primarily attributed to the rising global demand for protein-rich diets, increasing consumption of processed and frozen meat products, and the growing international trade of poultry and livestock-based foods. Meat and poultry products are highly perishable and prone to microbial contamination such as Salmonella, E. coli, and Listeria monocytogenes, making rigorous safety testing essential throughout the cold chain. Regulatory authorities worldwide are enforcing stricter hygiene and residue control standards for meat exports, compelling producers and distributors to adopt comprehensive safety testing protocols. Furthermore, advancements in rapid testing technologies—such as molecular diagnostics and biosensors—are improving detection accuracy and speed, allowing for real-time monitoring of contamination risks. The expansion of cold storage infrastructure and the proliferation of meat processing facilities in emerging markets further bolster this segment’s growth, as maintaining quality and compliance becomes critical to ensuring consumer safety and brand integrity.

This growth is fueled by the increasing accountability placed on manufacturers to ensure product quality, regulatory compliance, and consumer safety from production to distribution. As manufacturers handle large volumes of perishable goods such as dairy, meat, seafood, and frozen foods, maintaining strict temperature control and hygiene standards across the cold chain is critical. Regulatory bodies worldwide are imposing more stringent food safety testing requirements, compelling manufacturers to integrate comprehensive, third-party testing services into their quality assurance processes. Additionally, the growing demand for export certification, traceability, and clean-label verification further drives testing adoption among producers. The segment’s growth is also supported by technological advancements such as automated testing platforms, IoT-based monitoring, and digital reporting systems that enhance efficiency and transparency in safety compliance. Consequently, food and beverage manufacturers are increasingly prioritizing reliable cold chain testing partnerships to prevent contamination risks, safeguard brand reputation, and meet evolving consumer and regulatory expectations.

North America is expected to witness the highest growth over the forecast period in the Global Cold Chain Food Safety Testing Service Market. This robust growth is driven by the region’s well-established cold chain infrastructure, stringent food safety regulations, and high consumer awareness regarding food quality and safety. Regulatory authorities such as the U.S. Food and Drug Administration (FDA) and the Canadian Food Inspection Agency (CFIA) are enforcing rigorous compliance standards for perishable and temperature-sensitive products, which increases the demand for regular testing and monitoring services. Additionally, the growing consumption of processed, frozen, and ready-to-eat foods, coupled with the rapid expansion of e-commerce and last-mile cold chain delivery, is further boosting the adoption of advanced testing solutions. North America also leads in the integration of innovative technologies such as IoT-based real-time monitoring, automated testing platforms, and blockchain-enabled traceability, enabling enhanced safety, faster decision-making, and improved supply chain transparency. These factors collectively position North America as the fastest-growing region in the global cold chain food safety testing service market.

| Report Matrics | Details |

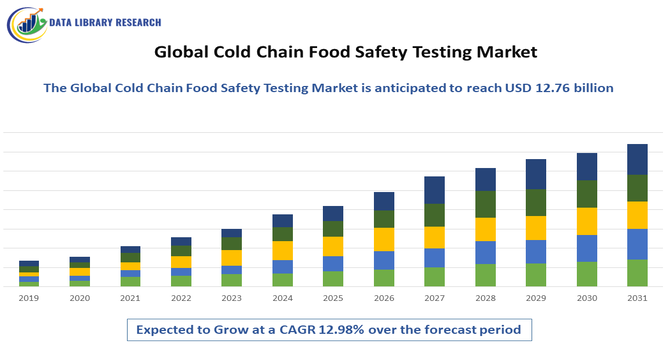

| Market Size Value | USD12.76 billion |

| Growth Rate | CAGR of 12.98 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The Global Cold Chain Food Safety Testing Service Market is characterized by a diverse and competitive landscape, encompassing a range of companies offering testing services, technologies, and solutions to ensure the safety and quality of temperature-sensitive food products throughout the supply chain. The market features a mix of established multinational corporations, specialized testing laboratories, and emerging technology-driven firms, all striving to meet the growing demand for food safety compliance and traceability.

Key Players in the Market:

Recent Development

Q1. What the main growth driving factors for this market?

The main drivers include the increasing incidence of foodborne illnesses and a corresponding rise in consumer awareness regarding food safety. Additionally, the globalization of complex food supply chains and the implementation of stringent government food safety regulations—like the U.S. FSMA—compel food manufacturers to adopt comprehensive, rigorous testing protocols across the entire cold chain, thereby fueling market expansion.

Q2. What are the main restraining factors for this market?

The primary restraints are the high operational and capital costs associated with maintaining the cold chain and advanced testing. This includes significant energy expenses for refrigeration and the substantial investment required for sophisticated testing equipment (e.g., LCMS, GCMS). Furthermore, a lack of skilled manpower and limited availability of certified maintenance centers for advanced tools, particularly in developing regions, can also hinder market growth.

Q3. Which segment is expected to witness high growth?

The rapid food safety testing technology segment is anticipated to witness high growth. This is driven by the urgent industry need for faster turnaround times and on-site analysis for real-time decision-making. Testing applications for processed food and the residues and contamination test type are also projected to see significant growth due to regulatory stringency and rising consumer demand for clean-label products.

Q4. Who are the top major players for this market?

The global cold chain food safety testing service market is dominated by major Testing, Inspection, and Certification (TIC) companies. The top major players include SGS S.A., Eurofins Scientific SE, Bureau Veritas, Intertek Group PLC, ALS Limited, and Mérieux NutriSciences. These firms leverage their extensive global network of laboratories and advanced analytical technologies to offer comprehensive testing and compliance solutions.

Q5. Which country is the largest player?

North America, primarily the United States, is consistently identified as the largest regional player for the overall food safety testing market. This dominance is due to a well-developed cold chain infrastructure, the adoption of advanced testing technologies, and the enforcement of highly stringent regulatory frameworks, such as the Food Safety Modernization Act (FSMA).

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model