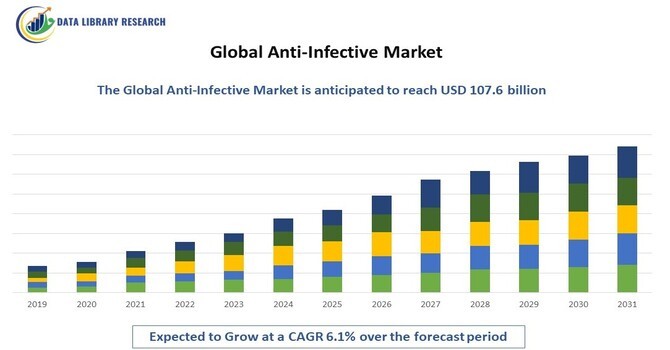

The global anti-infective market is poised for significant growth, with an expected market value of USD 68.2 billion in 2023, projected to reach USD 107.6 billion by 2031, reflecting a compound annual growth rate (CAGR) of 6.1% from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

This growth is driven by the increasing prevalence of infectious diseases, rising awareness of antibiotic resistance, and ongoing advancements in pharmaceutical research. Anti-infectives include many medications used to treat infections caused by bacteria, viruses, fungi, and parasites.

Anti-infectives are a broad category of medications designed to prevent, treat, or manage infections caused by various pathogens, including bacteria, viruses, fungi, and parasites. This category encompasses several classes of drugs, such as antibiotics, antivirals, antifungals, and antiparasitics, each targeting specific infections. Antibiotics, for example, are effective against bacterial infections, while antivirals focus on viral pathogens. The development and use of anti-infectives are critical in modern medicine, as they help combat infectious diseases that can lead to severe health complications or mortality. With the rise of antibiotic resistance and emerging infectious diseases, ongoing research and innovation in anti-infective therapies are essential to ensure effective treatment options remain available. Overall, anti-infectives play a vital role in public health and disease management, highlighting the need for responsible usage and stewardship.

These drugs are vital in addressing public health challenges posed by infectious agents, including hospital-acquired infections (HAIs) and emerging pathogens. The market encompasses a variety of product types, including antibiotics, antiviral agents, antifungals, and antiparasitics, each targeting specific infectious diseases. With the ongoing demand for effective treatment options and the constant evolution of pathogens, the anti-infective market remains a dynamic and essential sector of the global healthcare landscape.

The anti-infective market is experiencing several notable trends that are shaping its future. One significant trend is the increasing focus on antibiotic stewardship programs aimed at curbing antibiotic resistance through more judicious use of existing drugs and the development of new classes of anti-infectives. Additionally, the rise of personalized medicine is driving research towards tailored therapies that address individual patient profiles and specific infections. The integration of technology, such as artificial intelligence and machine learning, is enhancing drug discovery and development processes, allowing for faster identification of effective treatments. Furthermore, growing investment in research and development for new anti-infective agents is expected to lead to the introduction of innovative therapies. The COVID-19 pandemic has also accelerated the exploration of antiviral medications, prompting a renewed focus on infectious disease preparedness and rapid-response capabilities.

Market Segmentation

The global anti-infective market is segmented by product type (antibiotics, antivirals, antifungals, and antiparasitics), by application (hospital-acquired infections, community-acquired infections, and others), and by geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa). Each segment reflects varying growth dynamics influenced by factors such as disease prevalence, healthcare infrastructure, and regulatory environments, offering a comprehensive view of market opportunities and challenges.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The increasing prevalence of infectious diseases is a significant driver of growth in the anti-infective market. Several factors contribute to this rise, including rapid urbanization, which fosters crowded living conditions that facilitate the spread of pathogens. Additionally, increased global travel allows for the swift transmission of infections across borders, exposing populations to diseases that may not be endemic to their regions. Changing lifestyles, such as alterations in dietary habits and hygiene practices, can further exacerbate vulnerability to infections. Moreover, the resurgence of previously controlled diseases, such as tuberculosis and measles, underscores the critical need for effective anti-infective treatments. These diseases, once thought to be declining due to vaccination and treatment efforts, are re-emerging due to factors like vaccine hesitancy and the evolution of drug-resistant strains. The emergence of new pathogens, highlighted by the COVID-19 pandemic, has also placed additional strain on healthcare systems and has raised awareness of the importance of robust anti-infective therapies. **** The World Health Organization (WHO) has issued warnings about the alarming rise of antibiotic-resistant infections, a growing public health crisis that complicates treatment options and increases morbidity and mortality rates. This situation has created a pressing demand for the development of new anti-infective therapies, as current antibiotics may fail against resistant strains. The urgent need for innovative solutions reinforces the market's focus on research and development to discover novel agents that can effectively combat these evolving threats, ensuring that healthcare providers can continue to manage and treat infectious diseases effectively.

Innovations in drug discovery and development are playing a crucial role in accelerating the availability of new anti-infective agents, a necessity given the rising challenge of infectious diseases. Technologies such as genomics and proteomics enable researchers to analyze the genetic and protein profiles of pathogens, allowing for the identification of novel targets for anti-infective therapies. This detailed understanding of microbial mechanisms and host interactions opens up new avenues for therapeutic intervention, leading to the design of more effective treatments.

High-throughput screening technologies further streamline the discovery process by allowing scientists to test thousands of compounds quickly for their potential efficacy against specific pathogens. This rapid assessment can significantly shorten the timeline for identifying promising candidates for further development. As a result, pharmaceutical companies can bring innovative anti-infective agents to market more efficiently.

In addition to discovering new drugs, the development of combination therapies is enhancing treatment efficacy while also addressing the growing problem of antibiotic resistance. By using multiple agents that target different pathways or mechanisms, combination therapies can achieve greater effectiveness and reduce the likelihood of pathogens developing resistance. Improved formulations, such as sustained-release or targeted delivery systems, are also being developed to optimize therapeutic outcomes and minimize side effects.

Market Restraints

While antibiotic resistance poses a significant challenge, it also acts as a restraint on the anti-infective market. The emergence of multi-drug-resistant organisms complicates treatment regimens, leading to increased healthcare costs and a higher burden on healthcare systems. As existing antibiotics become less effective, the need for new drugs becomes more urgent, yet the development process can be lengthy and costly. Regulatory hurdles and the need for extensive clinical trials further complicate the introduction of new anti-infectives into the market. The high cost associated with the development of new anti-infective drugs is another significant restraint. The lengthy and complex process of clinical trials, coupled with the need for robust safety and efficacy data, can deter investment in anti-infective research. Additionally, the uncertainty of market return on investment, given the potential for antibiotic stewardship programs to limit the use of newly developed drugs, poses a challenge for pharmaceutical companies.

The COVID-19 pandemic has had a profound impact on the global anti-infective market. Initially, the pandemic caused disruptions in healthcare services, leading to a decline in elective procedures and outpatient visits, which affected the sales of certain anti-infective agents. However, it also spurred an accelerated focus on antiviral research, with significant investment directed toward developing treatments for viral infections. The pandemic highlighted the importance of rapid response capabilities for infectious diseases, leading to increased funding for research and development of both existing and novel anti-infectives. As the world emerges from the pandemic, the anti-infective market is expected to recover and evolve, with a heightened emphasis on preparedness for future infectious disease outbreaks.

Segmental Analysis

The antibiotics segment is projected to maintain a leading position in the anti-infective market throughout the forecast period, primarily due to the escalating incidence of bacterial infections worldwide. Antibiotics are essential for treating a wide range of infections, from common ailments to life-threatening conditions, underscoring their critical role in healthcare. However, the rising prevalence of antibiotic resistance poses a significant challenge, as many commonly used antibiotics become less effective against resistant bacterial strains.

This urgent situation has created a pressing demand for novel antibiotics capable of effectively targeting these resistant organisms. Researchers are increasingly focused on discovering new classes of antibiotics and exploring innovative approaches, such as combination therapies, which can enhance treatment efficacy and minimize resistance development. These efforts not only aim to replenish the dwindling antibiotic arsenal but also to provide more effective treatment options for patients facing resistant infections.

Furthermore, the growing emphasis on antibiotic stewardship programs is positively impacting the market. These programs promote the responsible use of antibiotics, encouraging healthcare providers to optimize prescribing practices while preserving the effectiveness of existing antibiotics. Increased awareness of the importance of stewardship helps mitigate the spread of resistance, ensuring that antibiotics remain a viable treatment option for future generations. Collectively, these dynamics indicate that the antibiotics segment will continue to be a focal point of investment and innovation within the anti-infective market, with ongoing research and development efforts driving significant growth in response to evolving bacterial threats.

The antiviral segment of the market is poised for significant growth, primarily due to the rising incidence of viral infections such as HIV, hepatitis, and influenza. Recent global health challenges, particularly the COVID-19 pandemic, have shifted attention toward coronaviruses, emphasizing the urgent need for effective antiviral therapies. As a result, there is a heightened focus on research and development aimed at discovering and optimizing new antiviral agents. Ongoing R&D efforts are critical in this context, as they aim to address both existing viral threats and emerging ones, fostering innovation in antiviral treatments. The successful rollout of COVID-19 vaccines and the development of various therapeutic options have not only provided immediate public health benefits but have also increased awareness among healthcare providers and the general public regarding the critical role of antiviral therapies in disease management. **** This heightened awareness is driving demand for innovative antiviral solutions, leading to increased investment in this sector. Additionally, the growing recognition of the potential for antivirals to prevent and treat viral infections is spurring collaborations among pharmaceutical companies, research institutions, and government agencies. Together, these factors create a robust environment for the antiviral segment, indicating that it will play a vital role in the future of infectious disease treatment and prevention.

North America is expected to command a substantial portion of the global anti-infective market, thanks to its advanced healthcare infrastructure, a high incidence of infectious diseases, and strong research and development initiatives. The region is home to leading pharmaceutical companies that drive continuous innovation in drug development, which further strengthens its market position. Additionally, favorable reimbursement policies and significant healthcare spending improve access to anti-infective treatments, contributing to the overall growth of the market in North America. These factors collectively highlight the region's crucial role in addressing infectious diseases and advancing therapeutic solutions, ensuring it remains a leader in the anti-infective sector.

Moreover, the increasing focus on combating antibiotic resistance in North America is prompting both public and private sectors to invest in the development of new anti-infective therapies. Collaborative efforts among research institutions, healthcare providers, and pharmaceutical companies are fostering a dynamic environment for innovation. The rising awareness of the importance of infection control, especially following the COVID-19 pandemic, has led to heightened demand for effective anti-infective treatments. Additionally, a growing aging population susceptible to infections is further driving market growth. Together, these trends position North America as a critical player in the global anti-infective market, poised for continued expansion and advancement in therapeutic options.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the global anti-infective market is characterized by the presence of several established pharmaceutical companies alongside emerging players focused on innovative drug development. Major players like Pfizer, Merck & Co., and GlaxoSmithKline dominate the market with their comprehensive portfolios of anti-infective agents. These companies invest heavily in research and development to address the challenges posed by antibiotic resistance and the need for novel therapies. Other notable players include Johnson & Johnson, Roche, and Novartis, which are also actively involved in developing new anti-infective treatments. The competitive strategies include collaboration with research institutions, aggressive marketing efforts, and the exploration of niche markets to expand their reach. The increasing focus on personalized medicine and patient-centric approaches is also driving competition in the anti-infective market.

The global anti-infective market features several major players dedicated to combating infectious diseases through innovative therapies. Leading companies include Pfizer, known for its extensive portfolio of antibiotics and antivirals; Merck, recognized for its focus on resistant bacterial infections; and GlaxoSmithKline, which develops next-generation therapies for various infections. Johnson & Johnson and Roche emphasize public health and antiviral treatments, respectively.

Novartis, AstraZeneca, and AbbVie are also key contributors, focusing on innovative anti-infective solutions. Other significant players include Bristol Myers Squibb, Sanofi, Amgen, Eli Lilly, and generic-focused companies like Teva and Mylan, which enhance access to essential medications. Emerging firms such as Bausch Health and Zydus Cadila contribute to the diverse landscape, ensuring a comprehensive approach to addressing the challenges of infectious diseases worldwide.

Anti-Infective Market Companies:

Recent Development

Q1. What are the driving factors for the global anti-infective market?

The global anti-infective market is driven by the increasing prevalence of infectious diseases, advancements in pharmaceutical research, and rising awareness of antibiotic resistance. The ongoing need for effective treatments, especially in light of emerging pathogens, further fuels market growth.

Q2. What are the restraining factors for the global anti-infective market?

The anti-infective market faces challenges from antibiotic resistance, high costs of drug development, and competition from alternative treatments. Regulatory hurdles and the need for extensive clinical trials can also hinder the introduction of new therapies.

Q3. Which segment is projected to hold the largest share in the global anti-infective market?

The antibiotics segment is expected to dominate the global anti-infective market due to the rising incidence of bacterial infections and the critical role antibiotics play in treatment.

Q4. Which region holds the largest share of the global anti-infective market?

North America is projected to hold the largest share of the global anti-infective market, driven by advanced healthcare infrastructure, high prevalence of infectious diseases, and robust research activities.

Q5. Who are the prominent players in the global anti-infective market?

Major players in the global anti-infective market include Pfizer, Merck & Co., GlaxoSmithKline, Johnson & Johnson, Roche, Novartis, AstraZeneca, and AbbVie, among others. These companies are known for their innovative therapies and strong R&D initiatives.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model