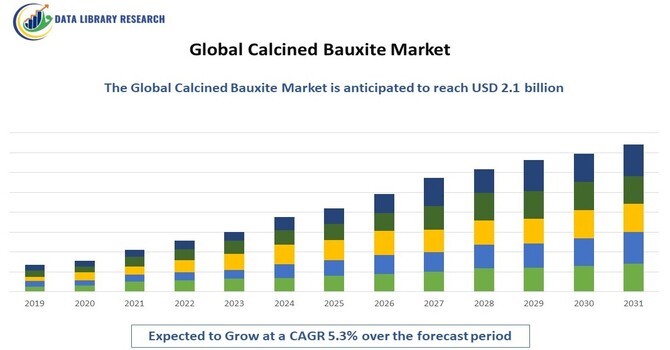

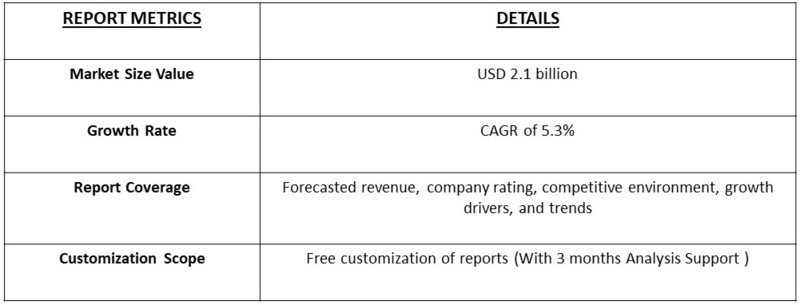

The global calcined bauxite market was valued at approximately USD 1.4 billion in 2023 and is projected to reach around USD 2.1 billion by 2031, growing at a compound annual growth rate (CAGR) of about 5.3% during the forecast period from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

The Calcined Bauxite Market refers to the global industry focused on the extraction, processing, and commercial utilization of bauxite ore that has been thermally treated to remove moisture, iron oxide, and other impurities. Calcined bauxite is a key raw material in high-temperature applications, including the production of refractories, abrasives, and as a proppant in hydraulic fracturing. The market encompasses various stakeholders, including mining companies, processing units, and end-user industries such as steel, cement, and construction. Growth in this market is primarily driven by increasing industrial demand for high-alumina content materials, superior thermal stability, and the expansion of infrastructure projects globally. Additionally, environmental regulations and sustainable mining practices also influence market dynamics.

The growth of the Calcined Bauxite Market is primarily driven by rising demand from the refractory industry, where high-alumina content is critical for heat-resistant applications in steel, cement, and glass manufacturing. Increasing infrastructure development and urbanization, particularly in emerging economies, are further boosting demand for calcined bauxite in construction materials. The expanding use of calcined bauxite as a proppant in hydraulic fracturing for oil and gas extraction also supports market growth. Additionally, stringent environmental regulations driving the adoption of more efficient, sustainable materials and advancements in mining technologies are further enhancing production efficiency and market expansion.

Key trends shaping the Calcined Bauxite Market include the increasing focus on sustainable mining practices and eco-friendly production processes to meet stringent environmental regulations. There's a growing demand for high-purity, high-alumina bauxite for advanced applications in refractories and abrasives, particularly in sectors like steel and cement. Technological advancements in processing techniques are also improving the efficiency and quality of calcined bauxite production. The rising use of calcined bauxite in infrastructure projects, driven by urbanization and industrialization in emerging markets, further contributes to market expansion. Additionally, the market is witnessing strategic mergers and acquisitions as companies seek to enhance their production capabilities and geographic presence.

Market Segmentation

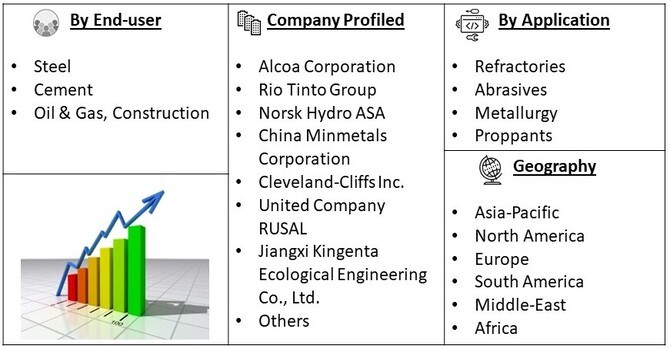

The Global Calcined Bauxite Market is segmented By Application (Refractories, Abrasives, Metallurgy, Proppants) By End-user Industry (Steel, Cement, Oil & Gas, Construction) and geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report offers the market size and forecasts for revenue (USD million) for all the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

One of the most significant drivers of the calcined bauxite market is the surge in infrastructure development, especially in rapidly industrializing countries such as China, India, and Southeast Asia. Governments in these regions are investing heavily in large-scale infrastructure projects, including roads, bridges, and urban housing, where calcined bauxite is used in construction materials due to its durability and high alumina content. For instance, China’s Belt and Road Initiative (BRI) continues to accelerate the demand for raw materials like calcined bauxite, as massive infrastructure networks are constructed across Asia, Europe, and Africa. The urbanization trend is also creating increased demand for steel and cement, key industries where calcined bauxite is a critical component in refractory materials.

The refractory industry, which relies heavily on high-alumina calcined bauxite for its heat-resistant properties, is seeing a significant boost from the growing global steel industry. With steel production rebounding after the pandemic-induced downturn, driven by automotive, construction, and industrial manufacturing sectors, there is a corresponding surge in demand for refractory-grade calcined bauxite. In 2023, global crude steel production crossed 1.8 billion metric tons, with China, India, and the U.S. leading production. As steel manufacturers push to increase efficiency and output, the need for high-quality refractory materials, which include calcined bauxite for furnace linings, is intensifying. This trend is further supported by stricter environmental regulations requiring advanced, longer-lasting refractories, contributing to market growth.

Market Restraints

A major restraint in the calcined bauxite market is the tightening of environmental regulations and mining restrictions, particularly in key producing regions such as China and India. Governments in these countries have implemented stricter controls on mining activities due to concerns over air and water pollution, habitat destruction, and carbon emissions. For example, China's crackdown on illegal mining operations and its focus on "green mining" practices has led to supply shortages and increased production costs. Additionally, global initiatives like the Paris Agreement are driving industries to adopt cleaner technologies, further raising compliance costs for calcined bauxite producers. This regulatory environment not only limits production capacity but also creates uncertainty in supply chains, pressuring companies to seek sustainable alternatives or source from regions with less stringent controls, potentially increasing operational costs.

The COVID-19 pandemic significantly disrupted the calcined bauxite market, primarily due to supply chain interruptions, reduced industrial activity, and declining demand from key sectors such as steel and construction. Lockdowns and restrictions on mining operations in major producing countries like China and India led to supply shortages, while decreased global construction activity and delays in infrastructure projects further dampened demand. However, as economies recovered and industrial activity resumed in 2021, demand rebounded, particularly from the steel and refractory industries, helping the market regain momentum. The pandemic also accelerated the shift towards more efficient and sustainable mining practices, as companies adapted to evolving regulatory and environmental requirements.

Segmental Analysis

The refractories segment holds a significant share of the calcined bauxite market, driven by its essential role in high-temperature industrial processes. Refractory-grade calcined bauxite is used in lining furnaces, kilns, and reactors in industries such as steel, cement, and glass manufacturing, where materials must withstand extreme heat. The growth of the global steel industry, which produced over 1.8 billion metric tons of crude steel in 2023, has been a key driver for this segment. Furthermore, the shift towards electric arc furnaces (EAF) in steelmaking, which require more durable refractories, is boosting demand for high-alumina calcined bauxite. Additionally, stricter regulations around emissions and energy efficiency in industrial processes are pushing manufacturers to adopt higher-quality refractory materials, which also aligns with the global trend towards reducing carbon footprints.

The rotary kiln segment is a prominent sub-segment in the calcined bauxite market, known for producing bauxite with a higher alumina content and superior quality, suitable for demanding applications such as refractories and abrasives. Rotary kilns, compared to shaft kilns, offer more controlled and consistent calcination, resulting in a more uniform product with better thermal and chemical stability. The growing preference for rotary kiln bauxite is driven by the increasing need for high-performance materials in the steel and cement industries. Real-time developments include the expansion of rotary kiln facilities in China and India, where infrastructure investments are surging. Additionally, advancements in kiln technology, aimed at reducing energy consumption and emissions, are aligning with global sustainability goals, making rotary kiln calcined bauxite a preferred choice for industries seeking both quality and compliance with environmental standards.

The Asia-Pacific region is projected to witness significant growth in the calcined bauxite market during the forecast period, driven by rapid industrialization, urbanization, and infrastructure development across key economies such as China, India, and Southeast Asia. China's massive infrastructure projects, including its Belt and Road Initiative, have accelerated the demand for construction materials, steel, and cement, all of which heavily rely on calcined bauxite for high-temperature applications. Similarly, India’s expanding manufacturing sector and its emphasis on large-scale infrastructure development, such as smart cities and industrial corridors, are boosting the need for high-alumina refractory materials. Additionally, favorable government policies supporting the mining and metallurgical sectors, along with increasing investments in oil and gas projects across the region, are further propelling market growth. The Asia-Pacific region's dominance in the production of calcined bauxite, coupled with rising demand from both domestic and export markets, positions it as a critical hub for future expansion in the global market.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the calcined bauxite market is characterized by a mix of established players and emerging companies vying for market share through strategic initiatives, including mergers, acquisitions, and technological advancements. Major players focus on enhancing production efficiency and product quality to meet the growing demand from various end-user industries, such as steel, cement, and refractories. Companies are also investing in sustainable practices to comply with environmental regulations and improve their market positioning.

In addition to these strategies, companies in the calcined bauxite market are increasingly prioritizing research and development (R&D) to drive innovation and create value-added products. By investing in R&D, firms aim to develop new grades of calcined bauxite that meet specific industry requirements, such as enhanced thermal stability or improved chemical properties. This focus on innovation not only helps companies stay ahead of competitors but also allows them to cater to specialized applications in emerging sectors like aerospace and electronics. Furthermore, collaborations with academic institutions and industry partners are becoming common as companies seek to leverage external expertise and accelerate the development of next-generation materials. As the market evolves, adaptability and a commitment to innovation will be crucial for players aiming to capture greater market share and meet the diverse needs of their customers.

Key competitors in the calcined bauxite market include

Recent Development

Q1. What are the driving factors for the Global Calcined bauxite Market?

The global calcined bauxite market is driven by the increasing demand from key industries such as steel, cement, and refractories, which require high-quality raw materials. Additionally, the growing emphasis on sustainable practices and the need for efficient production methods are further propelling market growth.

Q2. What are the restraining factors for the Global Calcined bauxite market?

Despite its growth, the calcined bauxite market faces challenges such as fluctuating raw material prices and strict environmental regulations that can increase operational costs. Moreover, the availability of alternative materials may limit the market's expansion in certain applications.

Q3. Which segment is projected to hold the largest share of the Global Calcined bauxite market?

The refractories segment is projected to hold the largest share of the global calcined bauxite market, driven by its essential role in high-temperature industrial processes where durability and performance are critical.

Q4. Which region holds the largest share of the Global Calcined bauxite market?

Asia-Pacific, particularly China, holds the largest share of the global calcined bauxite market due to its extensive industrial base, significant production capabilities, and high demand for calcined bauxite in various applications.

Q5. Which are the prominent players in the Global Calcined bauxite market?

Key players in the global calcined bauxite market include companies like China Bauxite Group, Jiangxi Jinlin Bauxite Mining Co., Ltd., and Alcoa Corporation, among others. These firms are recognized for their extensive production capabilities, technological advancements, and strategic initiatives aimed at enhancing market presence.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model