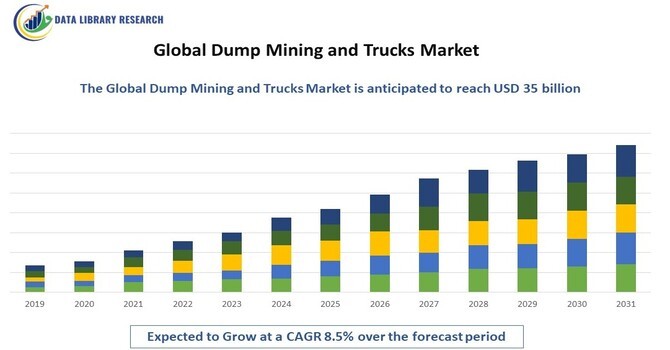

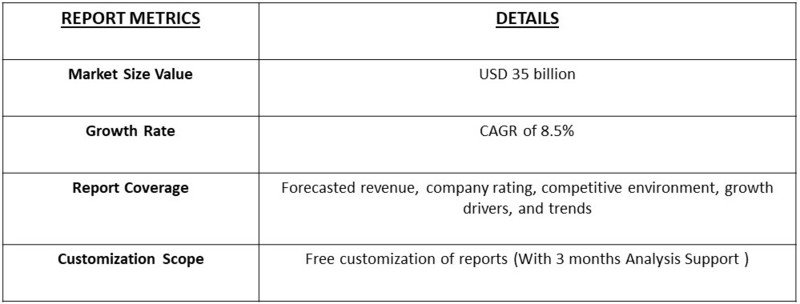

The global dump mining and trucks market was valued at approximately $20 billion in 2023 and is projected to reach around $35 billion by 2031, reflecting a compound annual growth rate (CAGR) of about 8.5% from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

The dump mining sector is crucial for the extraction and transportation of minerals, coal, and aggregates, with dump trucks serving as the backbone of these operations. As global demand for infrastructure development rises, particularly in emerging economies, the need for robust and efficient dump trucks is increasingly pressing. Rapid urbanization and industrialization in regions like Asia-Pacific and Latin America are driving mining activities, necessitating an expanded fleet to transport raw materials effectively. Technological advancements, such as automation and telematics, are enhancing operational efficiency and safety, allowing for real-time tracking and optimized fleet management. Additionally, the shift toward electric and hybrid dump trucks aligns with sustainability goals, reducing emissions and operational costs. As the sector adapts to these challenges, it continues to play a vital role in economic growth while prioritizing environmental stewardship. The ongoing evolution of the dump mining industry underscores its significance in meeting the resource demands of a rapidly developing world.

Market Trends

Key trends influencing the dump mining and trucks market include the rising adoption of electric and hybrid dump trucks, driven by a focus on sustainability and reduced operational costs. Additionally, the integration of advanced technologies such as GPS and telematics for fleet management is enhancing efficiency and safety in mining operations. Increasing investments in infrastructure projects, particularly in developing countries, are further stimulating demand for dump trucks. Moreover, the trend towards automation in mining operations is prompting manufacturers to innovate and develop advanced solutions that can handle complex tasks in challenging environments.

Market Segmentation

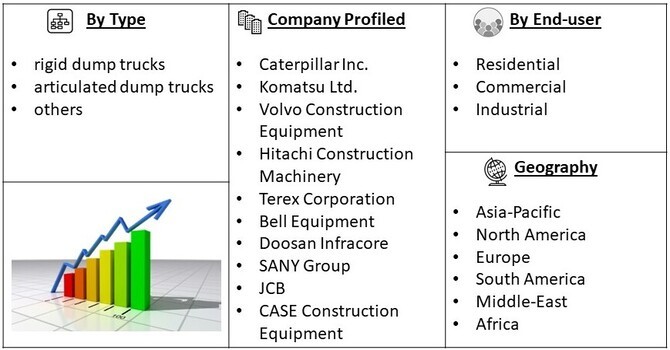

The global dump mining and trucks market is segmented by product type (rigid dump trucks, articulated dump trucks, and others), end-user (mining companies, construction firms, and others), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). This segmentation provides valuable insights into market dynamics, enabling stakeholders to identify growth opportunities in specific areas.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The increasing demand for essential minerals such as coal, copper, and iron ore is a key factor driving the growth of the dump mining and trucks market. These resources are fundamental to numerous industries, including construction, manufacturing, and energy production, making their availability critical as economies expand and urbanize. As industrial activities ramp up, the need for raw materials escalates. This surge is particularly evident in developing regions, where rapid urbanization leads to a greater requirement for infrastructure projects, housing, and transportation networks. Consequently, mining companies are under pressure to extract and deliver these materials efficiently and reliably. To meet this demand, companies are investing heavily in advanced dump trucks and mining technologies that can handle larger volumes while operating more efficiently. Innovations in vehicle design, such as enhanced payload capacities and improved fuel efficiency, are becoming vital. Moreover, the adoption of automation and smart technologies is allowing for more streamlined operations, reducing the time and labor required to transport materials from extraction sites to processing facilities. This focus on efficient transportation solutions not only helps meet current demand but also positions mining companies to adapt to future market fluctuations. By leveraging advanced dump trucks and optimizing logistics, these companies can ensure a steady supply of minerals while maintaining cost-effectiveness and competitiveness in a rapidly evolving marketplace. As a result, the dump mining and trucks market is poised for significant growth, driven by the relentless demand for essential raw materials that underpin modern economies.

The global emphasis on infrastructure development, especially in emerging economies, is significantly driving the demand for dump trucks. As countries prioritize upgrading and expanding their infrastructure to support economic growth, there is an urgent need for robust transportation solutions capable of moving large quantities of materials efficiently. Projects involving roads, bridges, and urban developments are particularly resource-intensive, requiring substantial inputs such as aggregates, concrete, and other construction materials. In many emerging markets, rapid urbanization is transforming landscapes, with cities expanding and new housing developments springing up to accommodate growing populations. This surge in construction activity directly correlates with the heightened need for dump trucks, which play a critical role in transporting essential materials from quarries and production sites to construction locations. Moreover, government initiatives aimed at improving infrastructure, such as public-private partnerships and increased funding for development projects, are further stimulating demand. These initiatives not only foster local job creation but also enhance overall economic stability, creating a favorable environment for mining and construction activities. The utilization of advanced dump trucks is essential in this context, as they provide the necessary capacity, durability, and efficiency to meet the growing demands of infrastructure projects. Innovations in truck design, including larger payload capacities and enhanced fuel efficiency, are making it possible to transport more materials with fewer trips, thereby reducing operational costs and environmental impact.

Market Restraints

The high cost of advanced dump trucks and associated technologies poses a significant restraint on the dump mining and trucks market. Modern dump trucks, equipped with features such as increased payload capacity, automation, and telematics systems, require substantial capital investment. For smaller mining companies and operations in developing regions, these financial barriers can be particularly daunting, restricting their ability to upgrade or expand their fleets. As a result, many companies may rely on older, less efficient vehicles, which can lead to higher operational costs, increased downtime, and reduced productivity. This reliance on outdated equipment can also limit their competitiveness in a market that increasingly favors efficiency and innovation. Furthermore, the lengthy return on investment associated with these advanced technologies may deter companies from making necessary upgrades, especially in volatile economic conditions where margins are tight. In essence, while technological advancements are crucial for improving efficiency and meeting rising demand, the associated costs can hinder the ability of many players in the market to fully capitalize on these opportunities. Addressing this financial challenge is essential for fostering growth and innovation in the dump mining and trucks sector.

The COVID-19 pandemic had a significant impact on the dump mining and trucks market, disrupting operations and supply chains while leading to delays in ongoing projects. With many mining sites temporarily shutting down or reducing their workforce to comply with health regulations, the demand for dump trucks experienced a decline. Additionally, restrictions on movement and transportation hindered the delivery of essential materials and equipment, exacerbating project backlogs. However, the pandemic also prompted a shift towards automation and digital solutions, as companies sought to enhance operational resilience and efficiency. As the market gradually recovers, the emphasis on technological advancements and improved safety protocols is expected to drive future growth, positioning the sector for a more adaptable and innovative approach in the post-pandemic landscape.

Segmental Analysis

The articulated dump trucks (ADTs) segment is poised to hold a significant share of the dump mining and trucks market, primarily due to their versatility and superior performance in navigating rough terrains. Unlike rigid trucks, articulated dump trucks feature a hinge between the cab and the trailer, allowing for greater flexibility and maneuverability in challenging off-road environments. This design is particularly advantageous in mining and construction sites where uneven ground, steep gradients, and tight spaces are common.

ADTs excel in transporting heavy loads across diverse landscapes, making them ideal for applications in both surface and underground mining operations. Their robust construction and advanced suspension systems ensure stability and control, even when loaded to capacity, enhancing safety and efficiency on-site. Additionally, many articulated dump trucks are equipped with powerful engines and advanced drivetrain technologies that further improve their performance in demanding conditions.

As mining operations increasingly expand into remote areas—often characterized by rough and unpaved roads—the demand for articulated dump trucks is expected to rise. These vehicles can traverse such terrains where traditional trucks may struggle, providing mining companies with the necessary reliability to ensure the smooth transportation of materials. Furthermore, the ability of ADTs to operate effectively in challenging conditions minimizes downtime and optimizes productivity, which is crucial for maintaining profitability in competitive markets.

The mining companies segment is anticipated to dominate the dump mining and trucks market, as these firms represent the primary end-users of dump trucks. Their core operations rely heavily on the efficient transport of materials, making dump trucks essential for moving mined resources such as coal, iron ore, and precious metals from extraction sites to processing facilities. *****To enhance operational efficiency, mining companies are making significant investments in fleet upgrades and expansions. As the demand for raw materials increases globally, these companies are under pressure to improve productivity while simultaneously reducing costs. Advanced dump truck technologies, including automated systems, telematics for real-time monitoring, and improved fuel efficiency, are becoming integral to optimizing their operations.

By adopting modern dump trucks, mining companies can streamline logistics, minimize downtime, and improve safety on site. Features such as enhanced payload capacities and superior maneuverability allow for more effective handling of challenging terrains, which is particularly important as mining operations often extend into remote and rugged areas. This focus on technological advancement not only helps in meeting immediate operational needs but also positions these companies competitively in an evolving market landscape.

Regional Analysis

North America is poised to maintain a dominant position in the global dump mining and trucks market, largely due to its well-established mining infrastructure and robust regulatory frameworks that support the industry. The region is home to a wealth of mineral reserves, including key resources such as coal, copper, and precious metals, which creates a steady demand for efficient transportation solutions like dump trucks.

Significant investments in technology and innovation further enhance North America's competitive edge. Many leading manufacturers of dump trucks and related equipment are based in this region, driving advancements in design, automation, and fuel efficiency. These innovations not only improve operational performance but also align with growing sustainability goals, as companies seek to reduce their environmental impact.

Moreover, favorable economic conditions, characterized by steady growth and an expanding construction sector, provide additional impetus for the dump mining and trucks market. As infrastructure projects proliferate, the demand for raw materials rises, necessitating the reliable and efficient transportation capabilities that modern dump trucks offer.

To Learn More About This Report - Request a Free Sample Copy

The dump mining and trucks market features several prominent players, including Caterpillar, Komatsu, Volvo Construction Equipment, and Hitachi Construction Machinery. These companies are focused on innovation, expanding their product portfolios, and forming strategic partnerships to enhance market presence. Emerging players are also entering the market, fostering competition and driving advancements in dump truck technologies. Research and development initiatives aimed at improving efficiency and sustainability are central to the competitive strategies of leading firms.

Here are ten major players in the dump mining and trucks market

These companies are key contributors to the dump mining and trucks market, driving innovation and offering a range of solutions to meet the needs of mining operations worldwide.

Recent Developments

Q1. What are the driving factors for the Global Dump Mining and Trucks Market?

The global dump mining and trucks market is primarily driven by several interrelated factors, including the increasing demand for minerals and resources, ongoing infrastructure development projects, and significant technological advancements in truck design and efficiency. As global economies expand and urbanization continues, the need for essential raw materials—such as coal, iron ore, copper, and aggregates—grows. This rising demand compels mining companies to enhance their operations, leading to greater investments in dump trucks that can efficiently transport these materials from extraction sites to processing plants or construction projects.

Q2. What are the restraining factors for the Global Dump Mining and Trucks Market?

Key challenges facing the dump mining and trucks market include high initial costs associated with advanced dump trucks, regulatory hurdles, and fluctuating commodity prices that can significantly impact mining operations. The investment required for state-of-the-art dump trucks, which often incorporate the latest technology for efficiency and safety, can be substantial. This financial barrier may deter smaller mining companies from upgrading their fleets, limiting their operational capabilities and competitiveness.

Q3. Which segment is projected to hold the largest share in the Global Dump Mining and Trucks Market?

The articulated dump trucks segment is projected to hold the largest share of the dump mining and trucks market, primarily due to their versatility and superior performance in challenging terrains. Unlike rigid dump trucks, articulated dump trucks feature a pivot joint between the cab and the dump box, allowing for greater maneuverability and stability, particularly in rough or uneven landscapes typical of mining and construction sites.

Q4. Which region holds the largest share of the Global Dump Mining and Trucks Market?

North America is expected to hold the largest share of the global dump mining and trucks market, bolstered by a robust mining infrastructure, significant investments in technology, and a strong demand for raw materials. The region is home to a well-established network of mining operations, characterized by advanced facilities and experienced personnel that facilitate efficient extraction and transportation processes. This infrastructure not only supports existing operations but also attracts new investments, enhancing the region's competitive edge.

Q5. Who are the prominent players in the Global Dump Mining and Trucks Market?

Prominent players in the dump mining and trucks market, such as Caterpillar, Komatsu, Volvo Construction Equipment, and Hitachi Construction Machinery, are recognized for their strong commitment to innovation and sustainability. These companies are at the forefront of developing advanced equipment designed to enhance operational efficiency and minimize environmental impact.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model