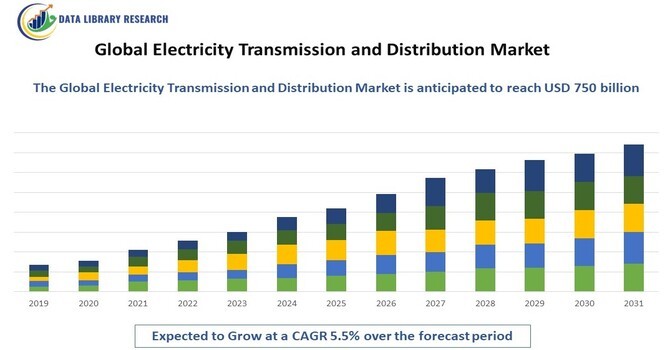

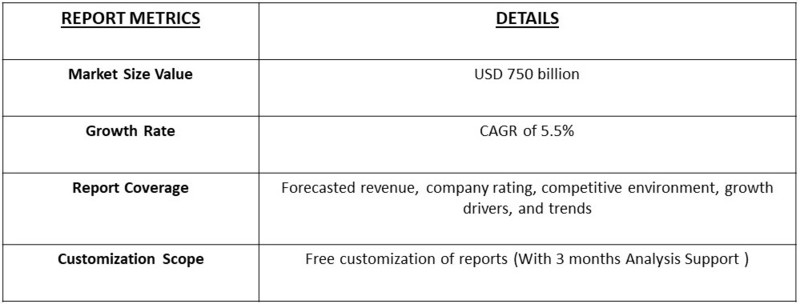

The global electricity transmission and distribution market was valued at approximately $500 billion in 2023 and is projected to reach around $750 billion by 2031, representing a compound annual growth rate (CAGR) of about 5.5% from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

The electricity transmission and distribution sector is a critical component of the overall energy system, comprising the networks and technologies essential for transporting electricity from generation sources, such as power plants and renewable energy facilities, to end-users, which include residential, commercial, and industrial consumers. This sector plays a vital role in ensuring reliable electricity supply and is increasingly becoming more complex due to several key factors.

One of the primary drivers of growth in this market is the increasing global demand for electricity. As populations grow and urban areas expand, the need for energy continues to rise. This demand is further fueled by the proliferation of digital devices, electric vehicles, and a general shift towards more energy-intensive lifestyles. Meeting this escalating demand requires significant investments in transmission and distribution infrastructure to enhance capacity and reliability.

Another major trend is the shift toward renewable energy sources. With a global push for sustainability and reduced carbon emissions, more power is being generated from renewable sources such as solar, wind, and hydroelectric systems. However, these energy sources are often intermittent and geographically dispersed, necessitating advancements in transmission systems to efficiently transport electricity from remote generation sites to urban centers. This transition demands the development of new transmission lines, substations, and grid interconnections, which can facilitate the integration of renewable energy into the existing grid.

Key trends influencing the electricity transmission and distribution market include the increasing adoption of smart grid technologies, which enable real-time monitoring and management of electricity flows, enhancing system efficiency and reliability. The integration of renewable energy sources into the grid is also a major trend, leading to investments in new transmission lines and infrastructure upgrades. Additionally, energy storage solutions are gaining traction, allowing for better management of supply and demand fluctuations. Growing regulatory frameworks aimed at reducing greenhouse gas emissions are prompting utilities to explore more sustainable and efficient energy solutions. Collaborative efforts among stakeholders, including government agencies, utilities, and technology providers, are fostering innovation and investment in the sector.

Market Segmentation

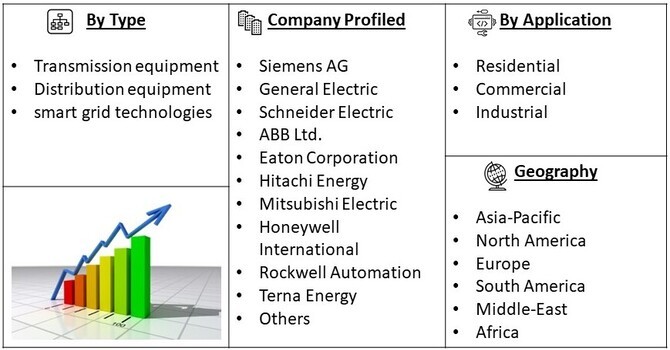

The global electricity transmission and distribution market is segmented by product type (transmission equipment, distribution equipment, and smart grid technologies), application (residential, commercial, and industrial), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). This segmentation provides insights into market dynamics, enabling stakeholders to identify opportunities for growth and development in specific areas.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The escalating global demand for electricity is fundamentally reshaping the electric transmission and distribution market, primarily fueled by urbanization, population growth, and rapid economic development. As cities expand and more individuals transition from rural to urban living, the need for reliable and consistent electricity supply intensifies. This urban influx increases energy consumption in residential, commercial, and industrial sectors, necessitating the development of robust transmission and distribution networks. Industries are expanding their operations and adopting energy-intensive technologies, which further amplifies electricity demand. As manufacturing processes become more automated and advanced, the reliance on stable energy sources becomes critical to maintaining productivity and efficiency. Similarly, the rise of digital technologies and electric vehicles adds new layers of demand on the existing grid, requiring utilities to upgrade and expand their infrastructure. Moreover, as more households gain access to electricity—particularly in developing regions—the pressure on transmission and distribution networks increases significantly. This trend calls for substantial investments in infrastructure, such as new transmission lines, substations, and grid enhancements, to ensure that electricity can be delivered reliably and efficiently to all consumers. Utilities must focus on modernizing aging infrastructure while expanding capacity to accommodate future growth.

The transition to renewable energy sources is significantly transforming the electric transmission and distribution landscape. With an increasing share of solar and wind power being integrated into the grid, utilities face the challenge of managing the intermittent and variable nature of these energy sources. This necessitates enhancements in transmission capabilities to ensure that energy can be effectively delivered from generation sites, often located far from consumption centers. As a result, substantial investments in grid modernization are required to upgrade existing infrastructure, enabling smarter, more responsive systems that can handle fluctuating energy outputs. Additionally, energy storage solutions, such as batteries, play a vital role in stabilizing the grid by storing excess energy generated during peak production times for use when demand rises. This integration of renewables and advanced technologies not only supports a more sustainable energy ecosystem but also drives market growth by fostering innovations that enhance reliability, efficiency, and resilience. Overall, the shift toward renewable energy is paving the way for a more dynamic and robust electric transmission and distribution network, positioning utilities to meet future energy demands effectively.

Market Restraints

One significant restraint for the electricity transmission and distribution market is the high capital investment required for infrastructure development and modernization. Upgrading aging grid systems, implementing smart grid technologies, and integrating renewable energy sources necessitate substantial financial resources. This can be particularly challenging for utilities operating in regions with limited budgets or regulatory constraints, leading to delays in necessary upgrades and expansions. Additionally, the complexity of navigating regulatory approvals and permitting processes can further hinder investment and slow the pace of modernization, ultimately impacting the overall efficiency and reliability of electricity delivery systems.

The COVID-19 pandemic had a profound effect on the electric transmission and distribution market, causing significant project delays and supply chain disruptions that hindered the timely delivery of essential services. Many utility companies grappled with operational challenges, including workforce shortages and the need to implement stringent safety protocols, which impacted maintenance and development efforts. However, the pandemic also acted as a catalyst for digital transformation within the sector. Utilities increasingly turned to remote monitoring and management technologies to ensure uninterrupted service delivery and improve operational efficiency, enabling them to adapt to the new normal. As economies begin to recover, there is a renewed focus on infrastructure investment aimed at enhancing grid reliability and resilience. This strategic emphasis not only addresses the vulnerabilities exposed during the pandemic but also sets the stage for potential growth in the market, as stakeholders prioritize modernization and the integration of smart technologies to future-proof energy delivery systems. Ultimately, the lessons learned during this period may foster a more resilient and adaptive electric transmission and distribution landscape.

Segmental Analysis

The smart grid technologies segment is projected to capture a substantial share of the electric transmission and distribution market, fueled by the escalating demand for enhanced grid efficiency and reliability. These advanced technologies empower utilities to monitor, control, and optimize energy flows in real-time, leading to significant improvements in operational performance and a reduction in outages. By integrating smart grid solutions, utilities can leverage data analytics and automated systems to proactively manage energy distribution, which not only improves service reliability but also facilitates quicker responses to issues as they arise. The increasing deployment of advanced metering infrastructure (AMI) and demand response programs further underpins the growth of this segment, as they allow for more precise energy usage tracking and better consumer engagement. Additionally, as more utilities become aware of the potential for smart technologies to bolster grid resilience and sustainability, investments in these solutions are anticipated to rise. This growing focus on modernization and efficiency solidifies the smart grid segment's critical role in the future landscape of the electric transmission and distribution market, positioning it as a key driver for innovation and improved service delivery.

The utilities segment is anticipated to occupy a substantial share of the electric transmission and distribution market, primarily due to its essential role in the delivery of electricity. Utilities are tasked with the crucial responsibilities of maintaining and upgrading the transmission and distribution infrastructure, ensuring a reliable power supply for residential, commercial, and industrial consumers. As global electricity demand escalates, utilities are making significant investments in modernizing their networks, which includes adopting smart technologies that enhance efficiency and responsiveness. This modernization effort often involves integrating renewable energy sources, enabling utilities to create a more resilient and sustainable energy grid. Moreover, the increasing complexity of energy demands—driven by factors such as urbanization, population growth, and the shift towards decentralized energy production—further underscores the need for robust utility infrastructure. As utilities focus on developing infrastructure that can accommodate these changes, their pivotal role becomes even more pronounced, positioning the utilities segment as a key driver of market growth. This commitment ensures that electricity remains accessible, reliable, and adaptable to future energy needs, reinforcing the importance of utilities in the overall transmission and distribution landscape.

Regional Analysis

North America is poised to maintain a leading position in the global electricity transmission and distribution market, primarily due to its well-established infrastructure and substantial investments in modernization efforts. The region's high levels of electricity consumption, combined with aging transmission and distribution networks, create a pressing need for upgrades and enhancements to ensure reliable power delivery. As utilities grapple with these challenges, the increasing integration of renewable energy sources—such as wind and solar—into the grid has become a pivotal factor driving investments in new transmission lines and smart grid technologies. These advancements not only enhance grid reliability but also facilitate the efficient management of variable energy sources. Additionally, government initiatives aimed at promoting energy efficiency, sustainability, and resilience are further fueling market growth in North America. Policies that encourage the adoption of smart technologies, demand response programs, and energy storage solutions are reinforcing the region's commitment to a modernized energy landscape. As a result, North America's proactive approach to infrastructure investment and innovative technologies positions it as a crucial player in shaping the future of electric transmission and distribution, ultimately ensuring that energy remains accessible and reliable for all consumers.

To Learn More About This Report - Request a Free Sample Copy

The electricity transmission and distribution market features prominent players such as Siemens AG, General Electric, Schneider Electric, ABB Ltd., and Eaton Corporation. These companies focus on innovation, expanding their product portfolios, and forming strategic partnerships to enhance market presence. Additionally, emerging players are entering the market, fostering competition and driving advancements in technology. Research and development initiatives aimed at improving efficiency, safety, and sustainability are central to the competitive strategies of leading firms.

Here are ten major players in the global electricity transmission and distribution market

Recent Developments

Q1. What are the driving factors for the Global Electricity Transmission and Distribution Market?

The global electric transmission and distribution market is driven by rising electricity demand due to population growth and urbanization, the integration of renewable energy sources, and technological advancements in smart grid solutions. These factors contribute to a pressing need for robust and efficient energy infrastructure to meet modern energy needs.

Q2. What are the restraining factors for the Global Electricity Transmission and Distribution Market?

Despite its growth potential, the electric transmission and distribution market faces challenges such as high implementation costs for advanced technologies, regulatory complexities that can delay project execution, and the need for significant investments in infrastructure. Additionally, competition from alternative energy sources may impact traditional utility operations.

Q3. Which segment is projected to hold the largest share in the Global Electricity Transmission and Distribution Market?

The smart grid technologies segment is projected to hold the largest share in the global electric transmission and distribution market, driven by increasing demand for improved grid efficiency and reliability. As utilities adopt advanced technologies for monitoring and management, the smart grid segment's prominence is expected to grow significantly.

Q4. Which region holds the largest share of the Global Electricity Transmission and Distribution Market?

North America is anticipated to hold the largest share of the global electric transmission and distribution market, bolstered by advanced infrastructure, high electricity consumption, and ongoing investments in modernization and renewable energy integration.

Q5. Which are the prominent players in the Global Electricity Transmission and Distribution Market?

Prominent players in the global electric transmission and distribution market include Siemens AG, General Electric, Schneider Electric, ABB Ltd., and Eaton Corporation. These companies are actively engaged in innovation and collaboration to advance technologies that enhance the efficiency and reliability of electric utilities.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model