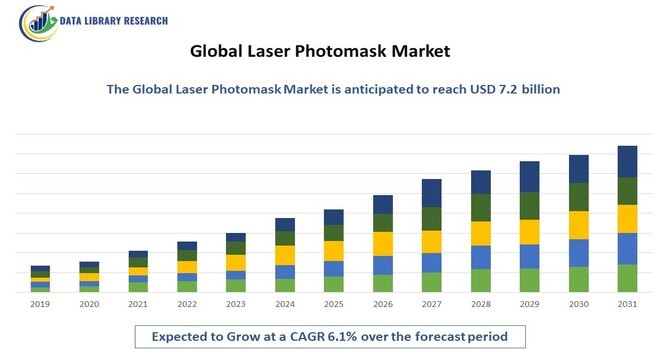

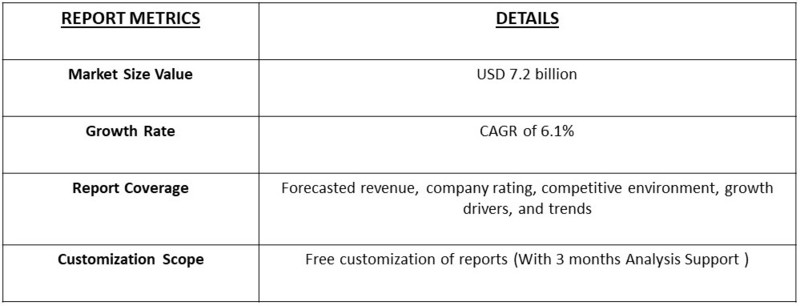

The global laser photomask market was valued at approximately $4.5 billion in 2023 and is projected to reach around $7.2 billion by 2031, growing at a compound annual growth rate (CAGR) of 6.1% from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

Photomasks are vital in semiconductor manufacturing, acting as precise templates for transferring complex circuit designs onto silicon wafers. With the surge in demand for electronics and the rapid evolution of industries like automotive, consumer electronics, and telecommunications, the laser photomask market is experiencing significant growth. The adoption of advanced technologies such as AI, IoT, and 5G is driving the need for more powerful semiconductors, directly boosting the demand for photomasks. Moreover, innovations like extreme ultraviolet (EUV) lithography are transforming the sector by enabling finer, more accurate patterning, essential for the miniaturization of chips. As industries push for higher performance and efficiency, the photomask market plays a critical role in supporting the development of cutting-edge semiconductors capable of meeting these evolving requirements.

The laser photomask market is also benefiting from increased investments in semiconductor research and development, as companies strive to innovate and maintain a competitive edge. As demand for faster, smaller, and more energy-efficient chips grows, particularly in the fields of artificial intelligence, machine learning, and high-performance computing, the precision and complexity of photomasks become even more critical. Photomask manufacturers are focusing on improving resolution, durability, and cost-effectiveness, ensuring that they meet the stringent requirements of next-generation semiconductor production. Furthermore, the growing shift toward autonomous vehicles, smart cities, and advanced telecommunications networks is amplifying the need for state-of-the-art photomask technologies. As the semiconductor industry continues to push the boundaries of performance, photomasks remain an indispensable tool for achieving the intricate designs needed for advanced microchips.

The laser photomask market is witnessing several key trends, including the increasing demand for advanced photomask technologies to support high-density integrated circuits (ICs). Additionally, the emergence of EUV lithography is pushing manufacturers to develop photomasks capable of handling smaller design nodes, ensuring higher precision in semiconductor production. As the electronics industry continues to focus on miniaturization, the requirement for photomasks with higher accuracy is becoming critical. Furthermore, the trend of outsourcing photomask production to specialized suppliers is gaining traction, as semiconductor manufacturers seek cost-effective and efficient solutions.

Market Segmentation

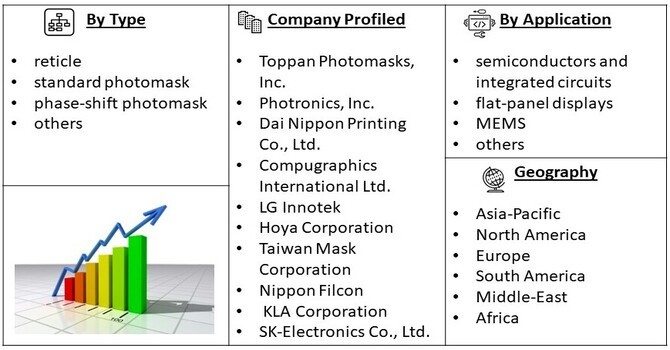

The global laser photomask market is segmented by type (reticle, standard photomask, phase-shift photomask, and others), application (semiconductors and integrated circuits, flat-panel displays, MEMS, and others), and region (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). This segmentation provides detailed insights into various market drivers and enables stakeholders to target specific growth opportunities.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The rising demand for semiconductors, driven by advancements in technologies like AI, 5G, and IoT, is a key factor propelling the laser photomask market. As industries transition towards automation and connectivity, the need for smaller, more efficient chips intensifies. This trend is particularly pronounced in sectors such as automotive (for autonomous vehicles), healthcare (for medical devices), and consumer electronics. Consequently, the demand for advanced photomasks, which are critical in the semiconductor manufacturing process, is expected to grow. Innovations such as EUV lithography are enabling manufacturers to produce highly complex and miniaturized circuit patterns, further driving the adoption of laser photomasks.

With consumers demanding faster, smaller, and more power-efficient devices, electronics manufacturers are focusing on chip miniaturization. The laser photomask market is expected to benefit from this trend, as smaller devices require more intricate and precise circuit designs. This miniaturization trend is prevalent across multiple industries, including smartphones, wearable devices, and laptops, resulting in increased reliance on photomasks for semiconductor fabrication.

The surge in flat-panel display production, particularly in Asia-Pacific, is boosting the demand for laser photomasks. Flat-panel displays are widely used in televisions, smartphones, and monitors, and advancements in display technologies such as OLED and QLED are driving the need for more advanced photomask solutions. This demand is further supported by the growing consumer preference for high-definition displays and ultra-thin screens.

Market Restraints

One of the primary challenges facing the laser photomask market is the high cost associated with the production of advanced photomasks, particularly for EUV lithography. The capital investment required for producing these photomasks can be prohibitive, especially for smaller semiconductor manufacturers. Additionally, the complexity involved in fabricating photomasks for smaller nodes increases production time, which can lead to delays in the semiconductor supply chain. These factors, along with stringent quality control measures, create significant financial and operational hurdles for manufacturers in this market.

The COVID-19 pandemic had a mixed impact on the laser photomask market. On one hand, supply chain disruptions delayed semiconductor manufacturing, leading to a temporary reduction in photomask demand. On the other hand, the pandemic accelerated digital transformation across various industries, driving the need for more electronics, and subsequently, more semiconductors. This digital surge mitigated some of the negative effects of the pandemic, positioning the photomask market for growth in the post-pandemic period as demand for semiconductor-driven technologies increases.

Segmental Analysis

The semiconductors and integrated circuits segment holds the largest share of the laser photomask market due to the crucial role photomasks play in semiconductor manufacturing. As the industry advances toward smaller nodes, such as 7nm and below, the need for high-precision photomasks has intensified. These smaller nodes enable more transistors on a chip, improving performance and energy efficiency, especially in cutting-edge technologies like AI, 5G, and autonomous vehicles. Additionally, the flat-panel display segment is experiencing rapid growth, driven by increasing demand for OLED and QLED technologies in consumer electronics such as smartphones and TVs. These advanced displays require highly accurate photomasks to achieve their superior image quality and resolution. The rising adoption of foldable screens, wearables, and higher-definition displays (4K, 8K) further boosts this demand. Both segments are expected to drive the laser photomask market as industries demand more complex and sophisticated electronic devices.

The growth of the standard photomask market is driven by several key factors, primarily the increasing demand for semiconductors across various industries. As sectors like automotive, consumer electronics, telecommunications, and data centers expand, the need for high-performance integrated circuits and chips is rising, fueling the photomask market. Additionally, the rapid adoption of advanced technologies such as AI, IoT, and 5G networks is driving the production of more complex and smaller semiconductor nodes, which require highly accurate photomasks. The shift towards smaller nodes and more precise circuit designs further emphasizes the importance of photomasks in achieving high-efficiency chip manufacturing. Moreover, innovations in photomask materials and production techniques, such as advancements in extreme ultraviolet (EUV) lithography, are enhancing photomask performance and precision, supporting the industry's miniaturization trends. As industries continue to digitize and evolve, the demand for photomasks is expected to remain strong, especially in regions like Asia-Pacific, where semiconductor and electronics manufacturing is a major driver.

Regional Analysis

Asia-Pacific is expected to dominate the laser photomask market, largely due to its robust electronics and semiconductor manufacturing presence, with major contributions from countries like China, South Korea, Taiwan, and Japan. These nations are home to leading semiconductor companies and have strong manufacturing ecosystems that drive demand for advanced photomasks used in chip fabrication. Additionally, the region leads in flat-panel display production, particularly with the growing adoption of OLED, QLED, and other high-definition display technologies in consumer electronics. This positions Asia-Pacific as a key hub for photomask innovation and production. Meanwhile, North America and Europe are also poised for steady growth, fueled by their focus on cutting-edge semiconductor research and development. These regions continue to push technological advancements in photomask technology, especially in applications like AI, IoT, and 5G, further supporting global market expansion. This combination of strong manufacturing bases and R&D investments makes Asia-Pacific the dominant force while enabling growth in other regions.

To Learn More About This Report - Request a Free Sample Copy

Key players in the laser photomask market are increasingly focusing on innovation and strategic partnerships to enhance their market presence and gain a competitive edge. Technological advancements in Extreme Ultraviolet (EUV) photomasks are at the forefront of this competition, as EUV technology enables the production of more precise, smaller semiconductor nodes, which are crucial for next-generation devices like 5G, AI, and high-performance computing. Companies are collaborating with leading semiconductor manufacturers to tailor photomask solutions that meet the complex requirements of advanced chip designs. These collaborations help streamline the production process and optimize photomask performance. Additionally, market leaders are heavily investing in research and development to improve photomask accuracy, durability, and efficiency, ensuring they meet the growing demands of cutting-edge technologies. Innovations aimed at reducing manufacturing costs and enhancing throughput are also key areas of focus, helping companies stay competitive in a fast-evolving market. These efforts are driving growth and intensifying competition as companies seek to meet the semiconductor industry's rapid advancements.

Here are ten major players in the laser photomask market

Recent Developments

Q1. What are the driving factors for the Global Laser Photomask Market?

The global laser photomask market is primarily driven by the growing demand for semiconductors due to advancements in technologies like AI, IoT, and 5G, coupled with the trend toward miniaturization in electronics. Additionally, the rise in flat-panel display production and the adoption of EUV lithography are key drivers.

Q2. What are the restraining factors for the Global Laser Photomask Market?

High production costs associated with advanced photomasks, particularly for EUV lithography, present a significant restraint. The complexity of fabricating precise photomasks for smaller nodes and the associated capital investment also hinder market growth.

Q3. Which segment holds the largest share in the Global Laser Photomask Market?

The semiconductors and integrated circuits segment holds the largest market share, as photomasks are essential for fabricating high-performance, miniaturized semiconductor devices

Q4. Which region holds the largest share of the Global Laser Photomask Market?

Asia-Pacific is expected to dominate the market due to its robust electronics and semiconductor manufacturing industries and strong production capabilities in flat-panel displays.

Q5. Who are the prominent players in the Global Laser Photomask Market?

Leading players include Toppan Photomasks, Inc., Photronics, Inc., Dai Nippon Printing Co., Ltd., Hoya Corporation, and LG Innotek, among others.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model