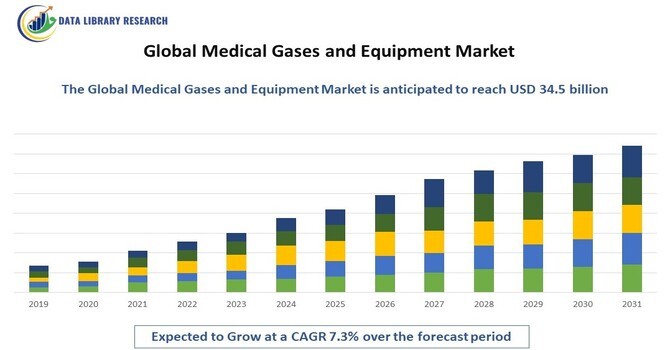

The global medical gases and equipment market was valued at approximately $20.5 billion in 2023 and is projected to reach around $34.5 billion by 2031, representing a compound annual growth rate (CAGR) of about 7.3% from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

Medical gases, including oxygen, nitrogen, nitrous oxide, and carbon dioxide, are essential in healthcare settings for a variety of applications, such as anesthesia, respiratory therapy, and surgical procedures. Equipment associated with medical gases includes storage tanks, gas delivery systems, and flow regulators, which ensure safe and efficient administration to patients. The increasing prevalence of chronic respiratory diseases, the growing number of surgical procedures, and advancements in healthcare infrastructure are significant factors driving the market growth.

The growth of the global medical gases and equipment market is primarily driven by several key factors. Firstly, the increasing prevalence of chronic respiratory diseases, such as COPD and asthma, necessitates a greater demand for oxygen therapy and respiratory support, propelling market expansion. Additionally, a rise in the number of surgical procedures, coupled with the growing awareness of the importance of anesthesia, further fuels the demand for medical gases. Technological advancements in gas delivery systems, including portable oxygen concentrators, enhance patient accessibility and improve treatment outcomes. Furthermore, the aging population is contributing to a higher incidence of health issues requiring medical gas interventions. The expansion of healthcare infrastructure, especially in emerging markets, is also facilitating increased access to medical gases and equipment. Lastly, the shift towards home healthcare services is promoting the adoption of portable medical gas solutions, broadening the market's reach and potential.

The medical gases and equipment market is witnessing several key trends contributing to its growth. The rising incidence of respiratory disorders, coupled with an aging population, is increasing the demand for oxygen therapy and respiratory support. Additionally, technological advancements in gas delivery systems and safety measures are enhancing the efficacy and safety of medical gases. The shift towards home healthcare services is also promoting the use of portable medical gases and equipment, expanding the market's reach. Furthermore, increased investments in healthcare infrastructure, particularly in developing regions, are driving demand for medical gases and related equipment.

Market Segmentation:

The Global Medical Gases and Equipment Companies and market is segmented by Product Type (Medical Gases and Medical Gas Equipment), Application (Respiratory Applications, Anesthesia Applications, Critical Care, Home Healthcare and Other Applications), End User (Hospital, Ambulatory Care, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report offers the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Driving Factors

The increasing prevalence of chronic respiratory conditions like COPD and asthma is significantly driving the demand for medical gases, especially oxygen therapy. These conditions are often exacerbated by environmental factors, such as pollution and smoking, leading to more patients requiring consistent respiratory support. As the global population ages, the number of individuals affected by these respiratory diseases is projected to rise, further intensifying the need for effective management solutions. Healthcare providers are responding by investing in advanced medical gas systems and equipment that can deliver safe, reliable oxygen therapy. Innovations in technology, such as portable oxygen concentrators, enable patients to receive care in various settings, including at home, enhancing their quality of life. Additionally, increased awareness about the benefits of oxygen therapy is encouraging more patients to seek treatment. This combination of rising incidence, technological advancements, and aging demographics underscores the critical importance of medical gases in modern healthcare, driving sustained growth in the market.

Innovations in gas delivery systems are revolutionizing the administration of medical gases, particularly with the introduction of portable oxygen concentrators. These devices allow patients to receive oxygen therapy conveniently at home or while on the go, significantly enhancing their mobility and independence. Improved safety measures, such as advanced monitoring systems and automatic shut-off features, ensure that patients receive a consistent and safe supply of gases, minimizing the risk of complications. These technological advancements not only enhance patient outcomes by providing timely and adequate respiratory support but also build confidence among healthcare providers in recommending these solutions. The ease of use and effectiveness of modern gas delivery systems encourage more patients to adhere to prescribed therapies, ultimately leading to better management of chronic respiratory conditions. Additionally, as healthcare providers recognize the benefits of these innovations, they are increasingly integrating them into treatment protocols, further driving adoption. Overall, these advancements are transforming the landscape of medical gases, making treatment more accessible and effective for patients in need.

Despite its promising growth potential, the medical gases and equipment market encounters several significant challenges. Regulatory complexities and stringent compliance requirements can delay the introduction of new products, making it difficult for companies to navigate the approval processes necessary for market entry. Additionally, the high installation and maintenance costs associated with gas delivery systems can be a barrier for healthcare facilities, especially those in low-income regions where budget constraints are prevalent. This limits accessibility to essential medical gases and equipment, affecting patient care. Moreover, the increasing competition from alternative therapies and emerging technologies, such as telehealth and non-invasive respiratory devices, may divert attention and resources away from traditional gas-based treatments. These factors combined create a challenging environment for stakeholders, necessitating strategic approaches to overcome barriers and sustain market growth.

The COVID-19 pandemic profoundly impacted the medical gases and equipment market, fundamentally altering its dynamics. The surge in hospitalizations due to respiratory complications associated with the virus resulted in an unprecedented demand for medical gases, particularly oxygen, as healthcare systems struggled to provide adequate support to patients. This spike in demand highlighted the critical importance of reliable gas delivery systems in emergency settings. However, the pandemic also exposed vulnerabilities within the market, including significant supply chain disruptions and shortages of essential equipment, which hampered healthcare facilities' ability to respond effectively. In response to these challenges, there has been a notable shift towards the adoption of telehealth and homecare services. Patients increasingly receiving care in their homes, where portable medical gas solutions and remote monitoring systems can enhance their quality of life while reducing hospital burdens. This transformation is likely to lead to lasting changes in how medical gases are delivered and managed, creating new opportunities for innovation and investment in the sector. Companies may focus on developing more efficient gas delivery systems, integrating digital health technologies, and improving patient education to navigate the evolving landscape. As the market adapts to these changes, the emphasis on resilience and flexibility in supply chains will become paramount, ensuring better preparedness for future healthcare challenges.

Segmental Analysis

The medical gases segment holds a significant market share, primarily driven by the essential role these gases play in healthcare settings. Oxygen, as the most widely used medical gas, is critical for treating patients with respiratory conditions, emergencies, and during surgical procedures. The growing prevalence of chronic respiratory diseases, coupled with an aging population, has further intensified the demand for medical gases. Additionally, the increasing use of nitrous oxide in anesthesia and sedation enhances its market presence. Regulatory frameworks ensuring the safety and efficacy of medical gases contribute to this segment's stability and growth. Innovations in gas delivery systems, such as portable oxygen concentrators and advanced cylinder technologies, are also expanding accessibility and use. Overall, the medical gases segment remains a cornerstone of the healthcare industry, underpinning effective patient care across various applications.

The respiratory applications segment is a major contributor to the medical gases and equipment market, reflecting the critical need for effective respiratory support in healthcare. With a rise in chronic respiratory diseases like COPD and asthma, there is an increasing demand for oxygen therapy and other respiratory interventions. This segment includes various applications, such as home oxygen therapy, emergency respiratory support, and continuous positive airway pressure (CPAP) therapies. The development of innovative delivery systems, such as nebulizers and portable oxygen concentrators, enhances the efficacy and convenience of respiratory treatments. Additionally, the growing emphasis on home healthcare solutions is propelling the adoption of medical gases for respiratory applications, allowing patients to receive care in comfortable settings. This trend underscores the importance of respiratory applications in improving patient outcomes and quality of life, solidifying its significant market share.

The hospitals segment commands a significant share of the medical gases and equipment market, primarily due to the critical role hospitals play in providing comprehensive patient care. Hospitals are key consumers of medical gases, using them extensively in various departments, including emergency rooms, operating theaters, and intensive care units. The high volume of surgical procedures and emergency interventions necessitates a reliable supply of medical gases, particularly oxygen and anesthetic gases. Furthermore, the increasing focus on patient safety and quality of care drives hospitals to invest in advanced gas delivery systems and safety protocols. As healthcare systems continue to evolve and expand, hospitals are increasingly adopting innovative technologies, such as integrated gas management systems, to optimize their operations. The growing number of hospitals and healthcare facilities globally further supports this segment's growth, positioning it as a pivotal player in the overall medical gas market.

Regional Analysis

The North America segment is poised to hold a significant market share in the medical gases and equipment market, bolstered by several critical factors. Firstly, the region benefits from advanced healthcare infrastructure, featuring state-of-the-art facilities and a well-established network of healthcare providers equipped to deliver high-quality care. This infrastructure not only supports the effective delivery of medical gases but also facilitates rapid adoption of new technologies.

Moreover, the high prevalence of respiratory diseases, such as COPD and asthma, amplifies the demand for medical gases, particularly oxygen therapy. This growing patient population drives healthcare providers to seek reliable and innovative solutions for respiratory support. The robust regulatory frameworks in North America also play a vital role, ensuring that medical gases and equipment meet stringent safety and efficacy standards. This regulatory rigor fosters trust among providers and patients alike, encouraging the adoption of advanced gas delivery systems.

Additionally, the region’s emphasis on technological innovations enhances patient care by improving treatment outcomes and overall healthcare efficiency. Ongoing investments in research and development lead to the creation of novel gas delivery solutions, including portable and smart systems that cater to evolving patient needs. As healthcare continues to prioritize patient-centric approaches, North America is expected to maintain its leadership position in the medical gases and equipment market, driving sustained growth and innovation in the sector.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the medical gases and equipment market is characterized by a mix of established players and emerging companies focused on innovation and expanding their product offerings. Major pharmaceutical and medical device companies, such as Air Liquide, Linde, and Praxair, dominate the market, leveraging their extensive distribution networks and technological expertise to deliver high-quality medical gases. These companies invest significantly in research and development to introduce advanced gas delivery systems and improve safety features, enhancing patient outcomes. Additionally, regional players are also gaining traction by focusing on niche markets and providing tailored solutions. Strategic partnerships, mergers, and acquisitions are common as companies aim to broaden their market reach and diversify their product lines. The emphasis on regulatory compliance and quality assurance further intensifies competition, compelling firms to maintain high standards and innovate continually. As the market evolves, companies that prioritize customer-centric approaches and adapt to changing healthcare needs are well-positioned to thrive in this dynamic environment.

Prominent Players Key players in the global medical gases and equipment market include major companies such as

Recent Developments

Q1. What are the driving factors for the Global Medical Gases and Equipment Market?

The global medical gases and equipment market is driven by several key factors. The rising prevalence of chronic respiratory conditions, such as COPD and asthma, has significantly increased the demand for medical gases, particularly oxygen therapy. Additionally, the aging population is more susceptible to various health issues, further propelling the need for effective respiratory support. Technological advancements in gas delivery systems, including portable and smart devices, enhance patient care and facilitate easier management of respiratory conditions. Furthermore, the increasing focus on home healthcare solutions is driving the demand for medical gases outside traditional hospital settings. Regulatory support and safety standards also promote the market, ensuring that medical gases are delivered effectively and safely. Lastly, the ongoing development of new applications and therapies for medical gases, such as their use in anesthesia and critical care, continues to expand market opportunities.

Q2. What are the restraining factors for the Global Medical Gases and Equipment Market?

Despite its growth potential, the global medical gases and equipment market faces several restraining factors. One major challenge is the regulatory complexities surrounding the approval and distribution of medical gases, which can delay product introduction and increase compliance costs. Additionally, the high installation and maintenance costs of advanced gas delivery systems may limit accessibility, particularly in low-income regions or smaller healthcare facilities. Competition from alternative therapies and emerging technologies can also pose challenges, as healthcare providers may opt for less expensive or more versatile options. Furthermore, supply chain vulnerabilities, highlighted during events like the COVID-19 pandemic, can impact the availability of critical equipment and gases. Lastly, the lack of awareness and understanding of medical gases in some healthcare sectors may hinder market growth and adoption.

Q3. Which segment is projected to hold the largest share in the Global Medical Gases and Equipment Market?

The medical gases segment is projected to hold the largest share in the global medical gases and equipment market. This dominance is primarily driven by the widespread use of gases like oxygen, which is essential for treating a variety of conditions, particularly respiratory diseases. The increasing prevalence of chronic respiratory conditions and the growing elderly population significantly contribute to the demand for medical gases. Additionally, the segment benefits from continuous advancements in gas delivery technologies, enhancing both safety and efficiency. Oxygen therapy, in particular, is gaining prominence in home healthcare settings, further bolstering the medical gases segment's market share. As healthcare systems evolve to prioritize patient-centered care, the focus on effective gas management and delivery is expected to grow, solidifying this segment's leading position in the market.

Q4. Which region holds the largest share of the Global Medical Gases and Equipment Market?

North America is anticipated to hold the largest share of the global medical gases and equipment market, driven by several key factors. The region boasts a well-established healthcare infrastructure, advanced medical technology, and high standards of patient care, facilitating the effective use of medical gases. The prevalence of chronic respiratory diseases and a growing elderly population in North America significantly increase the demand for medical gases, particularly oxygen therapy. Additionally, the presence of major players in the medical gases industry, along with ongoing research and development initiatives, contributes to the region's market leadership. Regulatory frameworks in North America further ensure the quality and safety of medical gases, enhancing provider and patient trust. As healthcare continues to innovate and expand, North America's emphasis on advanced treatment solutions is likely to maintain its significant market share.

Q5. Which are the prominent players in the Global Medical Gases and Equipment Market?

The global medical gases and equipment market features several prominent players that drive innovation and competition. Leading companies include Air Liquide, Linde, Praxair, and BOC Healthcare, all of which have established extensive distribution networks and a diverse portfolio of medical gases and equipment. These firms invest heavily in research and development to enhance their product offerings and improve patient outcomes. Additionally, companies like Messer Group and Air Products are also significant contributors, focusing on niche markets and tailored solutions for healthcare providers. Strategic partnerships, mergers, and acquisitions among these players further bolster their market positions, enabling them to expand their geographic reach and product lines. As the market evolves, these prominent companies are well-positioned to leverage their expertise and resources to meet the increasing demand for medical gases and equipment.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model