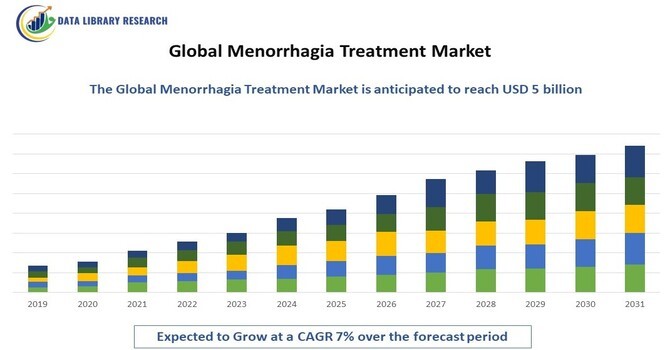

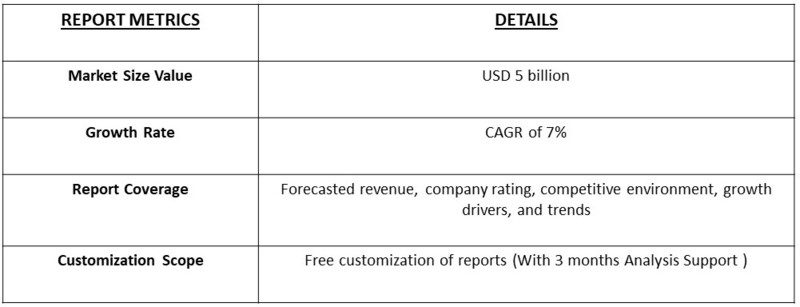

The global menorrhagia treatment market was valued at approximately $3 billion in 2023 and is projected to reach around $5 billion by 2031, reflecting a compound annual growth rate (CAGR) of about 7% from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

Menorrhagia, characterized by excessive menstrual bleeding, affects a significant number of women worldwide, leading to substantial impacts on their quality of life and health. The rising awareness regarding women's health issues, advancements in treatment options, and increasing healthcare expenditure are key factors driving market growth. With the development of innovative treatment modalities, including pharmaceutical therapies, minimally invasive procedures, and surgical interventions, the menorrhagia treatment market is becoming increasingly significant in the landscape of women's healthcare.

The growth of the global menorrhagia treatment market is primarily driven by several key factors, including the increasing prevalence of uterine conditions such as fibroids and polyps, which contribute to heavy menstrual bleeding. Rising awareness of women's health issues and the importance of managing menorrhagia has led more women to seek effective treatment options. Additionally, advancements in diagnostic technologies facilitate earlier detection and intervention, improving patient outcomes. The growing preference for minimally invasive procedures and the development of innovative pharmaceutical therapies, such as hormonal treatments and intrauterine devices, further enhance treatment accessibility and efficacy. Favorable reimbursement policies and improved access to healthcare services also play a crucial role in supporting market growth, as they enable more women to receive timely and effective care for their symptoms.

Key trends shaping the menorrhagia treatment market include the growing preference for minimally invasive surgical options and the increasing adoption of hormonal therapies. Advancements in endometrial ablation techniques and intrauterine devices (IUDs) have transformed treatment paradigms, providing effective alternatives to traditional surgeries. Furthermore, rising awareness and education about menorrhagia among healthcare professionals and patients are facilitating earlier diagnosis and intervention. Collaborative efforts between healthcare providers and pharmaceutical companies are leading to the development of tailored therapeutic solutions that better address the needs of women experiencing heavy menstrual bleeding. As more women seek effective treatments to manage their symptoms, the market is expected to witness sustained growth.

Market Segmentation

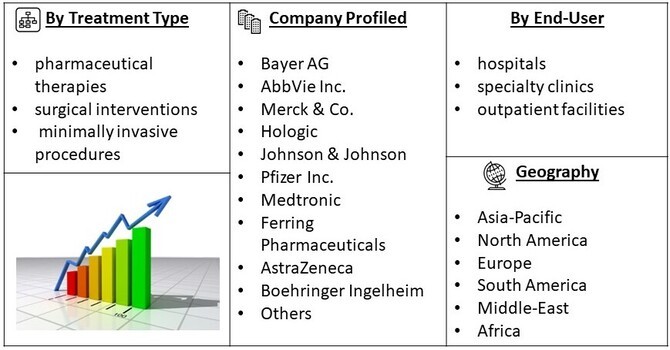

The global menorrhagia treatment market is segmented by treatment type (pharmaceutical therapies, surgical interventions, and minimally invasive procedures), end-user (hospitals, specialty clinics, and outpatient facilities), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). This segmentation offers insights into market dynamics and enables stakeholders to identify growth opportunities in specific areas. The pharmaceutical therapies segment, which includes medications such as nonsteroidal anti-inflammatory drugs (NSAIDs), hormonal treatments, and antifibrinolytics, is expected to dominate the market due to their widespread use and efficacy in managing symptoms.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The rising incidence of uterine conditions, particularly fibroids and polyps, is a significant driver of the menorrhagia treatment market. As these conditions are commonly associated with heavy menstrual bleeding, their prevalence contributes directly to the demand for effective treatment options. Factors such as age, obesity, and hormonal imbalances further exacerbate the occurrence of these conditions, particularly among women in their reproductive years. The aging population is also experiencing a higher prevalence of such disorders, prompting healthcare systems to prioritize the diagnosis and management of menorrhagia. This growing patient population is increasingly seeking solutions to manage their symptoms, which in turn stimulates market growth as healthcare providers expand their treatment offerings. Additionally, improved awareness among healthcare professionals about the implications of untreated menorrhagia is leading to more proactive management strategies, thereby driving demand for various therapeutic options.

Technological innovations and advancements in treatment options are crucial drivers of growth in the menorrhagia treatment market. The development of minimally invasive procedures, such as endometrial ablation and hysteroscopic myomectomy, offers effective alternatives to traditional surgical approaches, allowing for reduced recovery times and lower complication rates. Similarly, the introduction of novel pharmaceutical therapies, including hormonal treatments and intrauterine devices, provides women with more effective means to manage heavy menstrual bleeding. These advancements not only enhance treatment efficacy but also improve patient satisfaction and quality of life. Furthermore, ongoing research into targeted therapies aims to address the underlying hormonal imbalances that cause menorrhagia, promising even more personalized treatment options. As healthcare providers increasingly adopt these innovative approaches, the market is expected to witness significant growth, driven by the dual goals of improving patient outcomes and enhancing the overall management of menorrhagia.

One of the primary restraints affecting the menorrhagia treatment market is the high cost associated with advanced treatment options and procedures. Many innovative therapies, including minimally invasive surgical techniques and specialized pharmaceuticals, can be prohibitively expensive for patients, particularly in developing regions where healthcare budgets are constrained. This financial barrier limits access to effective treatment for many women suffering from menorrhagia, resulting in delayed diagnoses and unmanaged symptoms. Additionally, the complexity of regulatory approvals for new therapies can further increase costs, discouraging manufacturers from investing in the development of new solutions. While insurance coverage for certain treatments exists, variability in reimbursement policies across regions often leaves patients with significant out-of-pocket expenses. As a result, the high cost of care remains a critical challenge, hindering the overall growth of the market and preventing many women from receiving timely and effective management of their condition.

Market Restraints

One of the primary restraints affecting the menorrhagia treatment market is the high cost associated with advanced treatment options and procedures. Many innovative therapies, including minimally invasive surgical techniques and specialized pharmaceuticals, can be prohibitively expensive for patients, particularly in developing regions where healthcare budgets are constrained. This financial barrier limits access to effective treatment for many women suffering from menorrhagia, resulting in delayed diagnoses and unmanaged symptoms. Additionally, the complexity of regulatory approvals for new therapies can further increase costs, discouraging manufacturers from investing in the development of new solutions. While insurance coverage for certain treatments exists, variability in reimbursement policies across regions often leaves patients with significant out-of-pocket expenses. As a result, the high cost of care remains a critical challenge, hindering the overall growth of the market and preventing many women from receiving timely and effective management of their condition.

The COVID-19 pandemic significantly affected the menorrhagia treatment market, primarily due to the widespread postponement of elective procedures and routine healthcare visits. As healthcare systems shifted their focus to managing acute COVID-19 cases, many non-essential medical services were temporarily halted. This disruption resulted in delays for women seeking diagnosis and treatment for menorrhagia, leading to exacerbated symptoms and additional health complications, such as anemia and decreased quality of life. The backlog of patients awaiting treatment further strained healthcare resources, creating challenges in timely interventions. Despite these setbacks, the pandemic catalyzed a notable shift toward telemedicine and virtual consultations. Many healthcare providers quickly adapted to digital platforms, enabling women to receive ongoing care from the safety and comfort of their homes. This transition allowed for remote monitoring of symptoms, medication management, and educational support, helping to bridge the gap created by the disruption of in-person visits. Patients who might have previously hesitated to seek help were more willing to engage in virtual consultations, leading to earlier interventions and a better understanding of their conditions.

As healthcare systems begin to recover from the pandemic's impact, there is a renewed emphasis on improving access to care and enhancing women's health services. The lessons learned during this period are prompting investments in digital health technologies and integrated care models that prioritize women's health. This focus not only aims to address the backlog of patients but also seeks to ensure that women have consistent access to necessary treatments in the future. The combination of improved access to telehealth and a commitment to advancing women's health initiatives is expected to drive growth in the menorrhagia treatment market, ultimately leading to better health outcomes and increased patient satisfaction. As the landscape of healthcare continues to evolve, these changes will likely play a critical role in shaping the future of menorrhagia management.

Segmental Analysis

Minimally invasive procedures are anticipated to maintain a dominant position in the global menorrhagia treatment market due to their numerous advantages over traditional surgical options. Techniques such as endometrial ablation and hysteroscopic myomectomy offer effective solutions for managing heavy menstrual bleeding with significantly reduced recovery times, less pain, and smaller incisions. These procedures often lead to shorter hospital stays, allowing patients to return to their daily activities more quickly, which is increasingly appealing to women seeking effective yet convenient treatment options. Furthermore, the advancements in technology and techniques have improved the safety and efficacy of these procedures, contributing to their growing popularity among both healthcare providers and patients. As awareness of these benefits continues to spread, more healthcare facilities are adopting minimally invasive methods, which reinforces their position in the market. The combination of positive patient outcomes, increased satisfaction, and the ongoing development of innovative technologies is expected to solidify the dominance of minimally invasive procedures in the treatment of menorrhagia.

Hospitals are anticipated to maintain a dominant position in the global menorrhagia treatment market due to their comprehensive capabilities in delivering specialized care. Equipped with advanced medical technologies and multidisciplinary teams, hospitals can offer a wide range of diagnostic and treatment options for women suffering from heavy menstrual bleeding. The presence of specialized gynecological units allows for tailored care, from initial evaluation to post-operative support, ensuring that patients receive holistic management of their conditions. Additionally, hospitals are often at the forefront of adopting new treatment modalities, including minimally invasive procedures, which enhances their appeal to patients seeking effective and modern interventions. The integration of advanced imaging and diagnostic tools within hospital settings also facilitates timely and accurate diagnoses, enabling healthcare providers to implement appropriate treatment strategies. As patient safety and quality of care remain paramount, hospitals continue to invest in training and resources that enhance their capabilities in managing menorrhagia, solidifying their crucial role in the market. This emphasis on comprehensive care, coupled with a commitment to innovation, positions hospitals as key players in the ongoing advancement of menorrhagia treatment options.

Regional Analysis

North America is poised to maintain a dominant position in the global menorrhagia treatment market, fueled by its advanced healthcare infrastructure and a high level of awareness surrounding women's health issues. The region boasts cutting-edge medical facilities equipped with the latest technologies, enabling the effective diagnosis and treatment of conditions contributing to menorrhagia, such as uterine fibroids. Furthermore, significant investments in research and development are fostering innovation in treatment modalities, and enhancing the availability of effective solutions. The prevalence of uterine conditions in North America drives demand for comprehensive treatment options, while favorable reimbursement policies provide healthcare providers with the financial support needed to adopt and implement innovative therapies.

In Europe, the market is witnessing steady growth as governments and healthcare organizations increasingly prioritize women's health initiatives. Investments in advancing treatment technologies and raising awareness about menorrhagia are leading to improved healthcare access and management strategies. Meanwhile, the Asia-Pacific region is emerging as a lucrative market, characterized by rising awareness of women's health issues and enhancing access to healthcare services. As economic development progresses, more women are seeking effective treatments for menorrhagia, creating a growing demand for both surgical and pharmaceutical interventions. Overall, the combination of increased awareness, evolving healthcare infrastructure, and supportive policies across these regions is expected to drive sustained growth in the menorrhagia treatment market globally.

To Learn More About This Report - Request a Free Sample Copy

The menorrhagia treatment market is characterized by a dynamic landscape of prominent players, including Bayer AG, AbbVie Inc., Merck & Co., Hologic, and Johnson & Johnson, each committed to advancing treatment options for heavy menstrual bleeding. These established companies are focusing heavily on innovation, consistently investing in research and development to enhance their product portfolios with new therapies and technologies. This commitment to innovation not only aims to improve treatment efficacy but also seeks to address the diverse needs of women experiencing menorrhagia, ensuring that they have access to effective and safe solutions.

In addition to their internal efforts, these companies are increasingly forming strategic collaborations and partnerships with healthcare providers, research institutions, and technology firms. Such collaborations facilitate the exchange of knowledge and resources, allowing for the development of cutting-edge therapies and diagnostic tools. For instance, partnerships focused on developing minimally invasive procedures or advanced pharmaceutical solutions are becoming more common, reflecting the industry's shift toward patient-centered care.

Moreover, the entry of emerging players into the menorrhagia treatment market is fostering healthy competition and driving further advancements. These new entrants often bring innovative approaches and fresh perspectives, which can challenge established practices and inspire improvements across the sector. As these companies vie for market share, they contribute to an environment that prioritizes research initiatives aimed at enhancing treatment efficacy and patient outcomes.

Leading firms are also prioritizing the collection of real-world data and patient feedback to inform their product development strategies. This focus on patient-centered insights ensures that the treatments not only address clinical needs but also resonate with patients’ preferences and experiences. By continually adapting to the evolving landscape of women’s health, these companies are positioning themselves to remain at the forefront of the menorrhagia treatment market, ultimately enhancing the quality of care for women worldwide.

Here are ten major players in the menorrhagia treatment market

These companies are key players in driving innovation and advancing treatment options in the menorrhagia treatment market.

Q1. What are the driving factors for the Global Menorrhagia Treatment Market?

The global menorrhagia treatment market is significantly driven by the increasing prevalence of uterine conditions such as fibroids and polyps, which are common causes of heavy menstrual bleeding. As these conditions become more recognized and diagnosed, the demand for effective treatment solutions rises. Additionally, there is a growing awareness of women’s health issues, spurred by health campaigns and educational initiatives that empower women to understand and advocate for their health. This heightened awareness encourages more women to seek medical attention for menorrhagia, leading to an increase in consultations and treatment requests.

Q2. What are the restraining factors for the Global Menorrhagia Treatment Market?

Despite its growth potential, the menorrhagia treatment market encounters several significant challenges that could impede progress. One major issue is the high cost associated with advanced therapies and procedures, which can limit patient access, particularly in low-resource settings where healthcare budgets are constrained. Many women may be unable to afford necessary treatments, leading to untreated conditions and worsened health outcomes.

Q3. Which segment is projected to hold the largest share in the Global Menorrhagia Treatment Market?

The pharmaceutical therapies segment is projected to hold the largest share in the global menorrhagia treatment market, driven by the widespread use and effectiveness of various medications in managing heavy menstrual bleeding. Nonsteroidal anti-inflammatory drugs (NSAIDs) are commonly prescribed to alleviate pain and reduce menstrual flow, providing immediate relief for many women. Their accessibility and relatively low cost make them a preferred choice for initial management of menorrhagia.

Q4. Which region holds the largest share of the Global Menorrhagia Treatment Market?

North America is poised to hold the largest share of the global menorrhagia treatment market, primarily due to its advanced healthcare infrastructure, which includes state-of-the-art hospitals and specialized clinics equipped with the latest technologies for diagnosing and treating uterine conditions. This robust infrastructure facilitates the efficient delivery of care and ensures that women have access to a wide range of treatment options for menorrhagia. Additionally, the region experiences a high prevalence of uterine conditions, such as fibroids and polyps, which are common contributors to heavy menstrual bleeding. As these conditions become more widely recognized and diagnosed, the demand for effective treatment solutions increases, driving growth in the market.

Q5. Which are the prominent players in the Global Menorrhagia Treatment Market?

The global menorrhagia treatment market is characterized by several key players, including Bayer AG, AbbVie Inc., Merck & Co., Hologic, and Johnson & Johnson, all of which are dedicated to advancing women's health solutions. These companies prioritize innovation, investing heavily in research and development to create new therapies and improve existing treatments for heavy menstrual bleeding. By focusing on cutting-edge technologies, they aim to address the diverse needs of women experiencing menorrhagia.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model