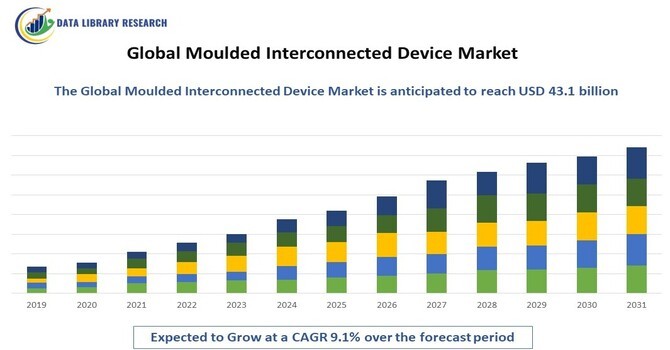

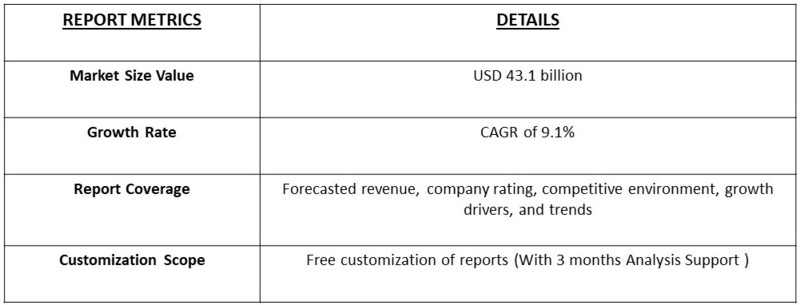

The market value of moulded interconnected devices (MIDs) is expected to reach 23.4 billion in 2023 and 43.1 billion in 2031, registering a Compound Annual Growth Rate (CAGR) of 9.1% during the forecast period, 2023-2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

The Moulded Interconnected Device (MID) Market refers to the specialized segment within electronics manufacturing that integrates mechanical and electronic functions directly into a single 3D plastic component. Utilizing advanced production techniques such as Laser Direct Structuring (LDS), MIDs enable compact, lightweight, and highly functional designs, reducing the need for traditional printed circuit boards. Key applications span industries including automotive, consumer electronics, medical devices, and industrial automation. As demand for miniaturization and smart devices grows, the MID market is poised for significant expansion, driven by innovations in material science and process technologies.

The Moulded Interconnected Device (MID) Market is driven by the growing demand for miniaturization and lightweight components across industries such as automotive, consumer electronics, and medical devices. The shift toward smart devices and IoT integration is accelerating the adoption of MIDs due to their ability to combine mechanical and electrical functions within a single, space-efficient part. Additionally, advancements in production technologies like Laser Direct Structuring (LDS) enable greater design flexibility and cost efficiency. Increased focus on sustainability and reducing electronic waste further propels the market, as MIDs help in reducing the overall material and energy footprint.

The Moulded Interconnected Device (MID) Market include the increasing integration of MID technology in automotive electronics for advanced driver-assistance systems (ADAS) and electric vehicle (EV) components. The rise of smart consumer devices, such as wearables and IoT-enabled home appliances, is further driving demand for compact and multifunctional MIDs. Advancements in 3D printing and Laser Direct Structuring (LDS) are enhancing design capabilities, allowing for greater customization and complexity. Additionally, the push toward greener electronics is encouraging the use of eco-friendly materials and manufacturing processes in MID production. These trends are collectively fostering innovation and growth within the MID market.

Market Segmentation

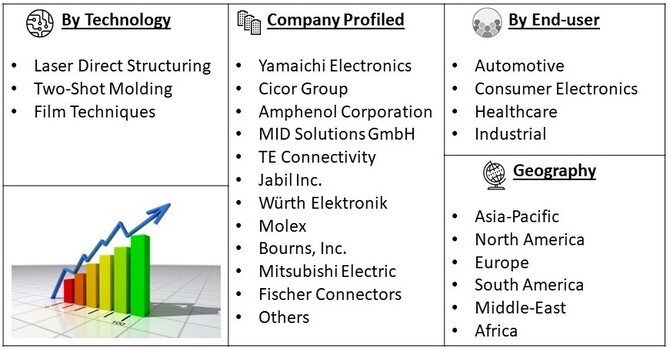

The Global moulded interconnected device Market is segmented by technology (Laser Direct Structuring, Two-Shot Molding, Film Techniques) End-user Industry (Automotive, Consumer Electronics, Healthcare, Industrial) and geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report offers the market size and forecasts for revenue (USD million) for all the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The growing adoption of Advanced Driver Assistance Systems (ADAS) and the rise of electric vehicles (EVs) are key drivers for the Moulded Interconnected Device (MID) market. ADAS features such as parking sensors, lane departure warning systems, and adaptive lighting require compact, lightweight, and highly integrated electronic components—areas where MIDs excel. Additionally, the shift to EVs is increasing the demand for efficient power management and electronic control units (ECUs). Major automakers like Tesla and BMW are incorporating MIDs into their next-generation vehicles to optimize space and improve energy efficiency. This trend is expected to accelerate as regulatory bodies worldwide push for higher safety standards and lower emissions, driving the need for sophisticated automotive electronics.

The rapid expansion of the Internet of Things (IoT) and the proliferation of smart consumer devices such as wearables, smart home systems, and personal electronics are fueling the MID market. Devices like Apple’s AirPods and Fitbit wearables rely on miniaturized components to offer enhanced functionality in a compact form factor. MIDs are ideal for this demand, as they allow manufacturers to integrate multiple functions into a single part, reducing weight and space while improving product performance. With global IoT spending expected to exceed $1 trillion by 2025, companies are increasingly turning to MIDs to meet the need for innovative, multifunctional, and connected devices that drive consumer engagement and convenience.

Market Restraints

One of the primary restraints in the Moulded Interconnected Device (MID) market is the high initial investment required for specialized equipment and the complexity of the manufacturing process. Technologies like Laser Direct Structuring (LDS) demand significant capital expenditure for laser systems and precise molding techniques, which can deter smaller manufacturers from adopting MIDs. Additionally, the design and production of MIDs require highly skilled expertise and intricate quality control, which increases operational costs. This challenge is particularly evident in emerging markets, where cost sensitivity remains a critical concern. For example, while global giants like Bosch and Siemens have successfully scaled MID production for advanced applications, many mid-tier companies struggle to justify the cost of transitioning from traditional PCB technologies. This high cost barrier limits widespread adoption, especially in cost-competitive industries.

The COVID-19 pandemic disrupted the Moulded Interconnected Device (MID) market by causing supply chain interruptions and delays in manufacturing activities, particularly in automotive and consumer electronics sectors. Temporary factory closures and reduced workforce availability slowed production, impacting demand for MIDs. However, the pandemic also accelerated the adoption of digitalization and smart devices, which spurred demand for compact, multifunctional electronic components. As economies recover, the MID market is expected to rebound, driven by increasing investments in automation, healthcare technology, and IoT-enabled devices.

Segmental Analysis

Laser Direct Structuring (LDS) is the most widely used technology in the Moulded Interconnected Device (MID) market, enabling manufacturers to create 3D circuit paths directly on molded plastic parts. This technology allows for precise circuit layouts and flexible designs, making it ideal for compact devices in industries like automotive, consumer electronics, and medical devices. Real-time developments show that companies such as LPKF Laser & Electronics AG are advancing LDS technology with faster, more efficient systems that can handle complex geometries. A key driving factor for LDS adoption is the rising demand for miniaturized and integrated electronics in advanced driver-assistance systems (ADAS), electric vehicles, and smart devices. As manufacturers seek to optimize space and reduce weight without compromising functionality, LDS technology is becoming critical for innovation in high-performance electronic components.

The automotive industry is a significant user of Moulded Interconnected Devices (MIDs), driven by the increasing demand for advanced driver-assistance systems (ADAS), infotainment controls, and electric vehicle (EV) components. MIDs allow automakers to incorporate multiple electronic functions into a single, lightweight component, crucial for reducing the overall weight of vehicles and improving energy efficiency. Companies like Continental and Bosch are integrating MIDs into automotive lighting, control units, and sensor systems. The growth of electric vehicles, coupled with stringent safety regulations and consumer demand for smart features, is propelling the use of MIDs in this segment. For instance, the push toward autonomous driving has led to higher MID adoption in systems like LIDAR and radar, driving innovation in automotive electronics.

The Asia-Pacific region is poised for substantial growth in the Moulded Interconnected Device (MID) market, driven by its position as a global manufacturing hub for electronics and automotive industries. Countries like China, Japan, and South Korea are seeing increased adoption of MIDs in consumer electronics, automotive components, and industrial automation due to the rising demand for miniaturized, multifunctional devices. The rapid expansion of the electric vehicle (EV) market in China and the growing investments in smart factories across the region are further propelling MID demand. Additionally, favorable government policies promoting advanced manufacturing technologies and increasing R&D investments in 3D circuitry are supporting market growth. For instance, leading companies such as Samsung and Foxconn are actively incorporating MID technology into their product lines, fueling the region’s market expansion.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Moulded Interconnected Device (MID) market is characterized by a mix of established global players and innovative regional manufacturers, all competing to capture market share across key industries such as automotive, consumer electronics, and healthcare. Leading companies like LPKF Laser & Electronics AG, Molex LLC, TE Connectivity, Harting Technology Group, and Panasonic Corporation dominate the market with advanced Laser Direct Structuring (LDS) technology and strong R&D capabilities.

Other key competitors include

Recent Development

Q1. What are the driving factors for the Global Moulded Interconnected Device (MID) Market?

The global Moulded Interconnected Device (MID) market is primarily driven by the increasing demand for miniaturization in electronic components. As industries strive to reduce the size and weight of devices, MIDs offer an effective solution by integrating multiple functions into a single component, thereby optimizing space and improving design flexibility. The rise of the Internet of Things (IoT) and smart devices further accelerates the need for compact, efficient connectivity solutions. Additionally, advancements in manufacturing technologies, such as injection molding and 3D printing, have made it easier and more cost-effective to produce MIDs, leading to wider adoption across various sectors, including automotive, consumer electronics, and telecommunications. The growing emphasis on automation and smart manufacturing also supports the MID market, as these devices enhance reliability and performance in complex electronic systems.

Q2. What are the restraining factors for the Global Moulded Interconnected Device (MID) market?

Despite its growth potential, the global MID market faces several challenges. One significant restraining factor is the high initial investment required for MID production and the associated technology. This can be a barrier for smaller manufacturers or startups looking to enter the market. Additionally, the complexity of designing and manufacturing MIDs may lead to longer development cycles, which can deter companies from adopting this technology. Quality control and reliability issues in high-stress environments, particularly in automotive and aerospace applications, may also limit acceptance. Furthermore, the market is competitive, with various alternatives available, which can hinder the growth of MIDs. Lastly, fluctuations in raw material prices can impact production costs and profit margins, posing challenges for manufacturers.

Q3. Which segment is projected to hold the largest share of the Global Moulded Interconnected Device (MID) market?

The automotive segment is projected to hold the largest share of the global Moulded Interconnected Device (MID) market. This growth is driven by the increasing incorporation of advanced electronics in vehicles, including infotainment systems, sensors, and control units. MIDs are particularly well-suited for automotive applications due to their ability to integrate multiple functions into a single, compact device, reducing weight and improving reliability. As the automotive industry shifts toward electric and autonomous vehicles, the demand for sophisticated electronic solutions will continue to rise. Moreover, stringent regulations regarding vehicle performance and safety are pushing manufacturers to adopt innovative technologies like MIDs to enhance system efficiency. As a result, the automotive sector is expected to remain a dominant force in the MID market.

Q4. • Which region holds the largest share of the Global Moulded Interconnected Device (MID) market?

North America is anticipated to hold the largest share of the global Moulded Interconnected Device (MID) market. This region benefits from a robust manufacturing base and strong technological advancements, particularly in the automotive and consumer electronics sectors. The presence of major players and innovation hubs fosters a competitive environment, driving the development and adoption of MID technologies. Additionally, the increasing focus on electric vehicles and smart devices aligns with the capabilities offered by MIDs, enhancing their market penetration. The demand for automation and IoT solutions further boosts the MID market in North America, as industries seek to improve efficiency and connectivity. With ongoing investments in research and development, the region is well-positioned to lead the MID market.

Q5. Which are the prominent players in the Global Moulded Interconnected Device (MID) market?

The global Moulded Interconnected Device (MID) market features several prominent players known for their innovation and market leadership. TE Connectivity stands out for its extensive product portfolio and commitment to developing advanced connectivity solutions across various sectors. Jabil Inc. is recognized for its expertise in manufacturing and engineering services, offering tailored MID solutions for diverse applications. Molex and Würth Elektronik also play crucial roles, focusing on integrating MIDs into their electronic components to enhance performance and reliability. Additionally, Mitsubishi Electric and Amphenol Corporation leverage their technological capabilities to provide high-quality MID solutions, particularly in the automotive and telecommunications industries. Emerging players and startups are also gaining traction, driving further innovation and competition. Through strategic partnerships and a focus on customer needs, these key players are shaping the future of the MID market.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model