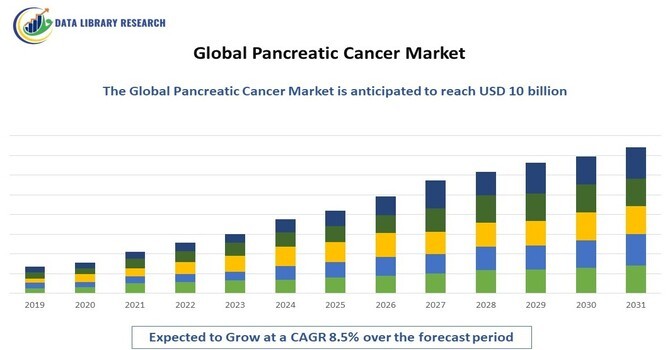

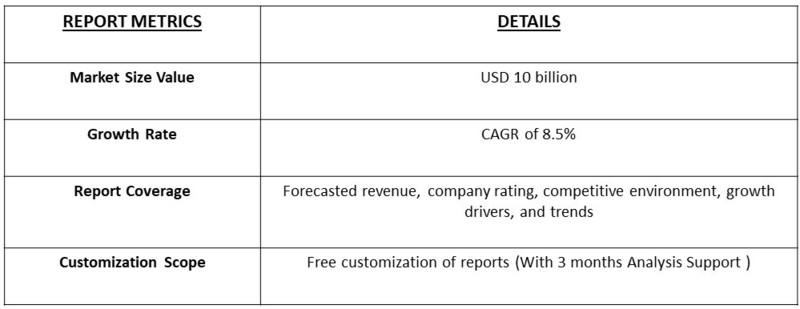

The global pancreatic cancer market was valued at approximately $5 billion in 2023 and is projected to reach around $10 billion by 2031, representing a compound annual growth rate (CAGR) of about 8.5% from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

Pancreatic cancer is one of the most aggressive forms of cancer, marked by the uncontrolled growth of pancreatic cells and often diagnosed at advanced stages, resulting in a high mortality rate. The rising incidence of this disease, driven by factors such as an aging population, obesity, smoking, and diabetes, underscores the urgent need for effective treatment solutions. Advancements in diagnostic techniques, including enhanced imaging modalities like MRI and CT scans, are facilitating earlier detection, which is crucial for improving patient outcomes.

Additionally, ongoing research into biomarkers holds promise for developing blood tests that could enable even earlier diagnosis. The treatment landscape is evolving, with traditional chemotherapy regimens like FOLFIRINOX and gemcitabine being complemented by newer targeted therapies aimed at specific genetic mutations, such as those in the KRAS gene. Immunotherapy is also gaining traction, offering hope through innovative approaches that harness the body’s immune system to combat cancer. Increased public and professional awareness, fueled by advocacy efforts and research funding, is leading to a more significant focus on pancreatic cancer, driving innovation in treatment and diagnosis. As pharmaceutical companies and research institutions invest heavily in this area, the pancreatic cancer market is poised for substantial growth. These advancements collectively represent a critical shift towards more effective management of pancreatic cancer, providing hope for improved survival rates and quality of life for patients facing this formidable disease.

Key trends in the pancreatic cancer market are significantly reshaping the landscape of diagnosis and treatment, primarily focusing on early detection and personalized medicine. Early diagnosis is crucial, as pancreatic cancer often presents with nonspecific symptoms, leading to late-stage identification and poor prognosis. Innovations in diagnostic imaging technologies, such as high-resolution MRI, CT scans, and endoscopic ultrasound, have improved the ability to visualize pancreatic tumors at earlier stages. Furthermore, advancements in biomarkers are paving the way for blood tests that could identify pancreatic cancer before clinical symptoms arise, allowing for timely intervention and improved survival rates.

The trend toward personalized medicine is also gaining momentum, driven by a deeper understanding of the genetic and molecular underpinnings of pancreatic cancer. Targeted therapies are being developed to specifically attack cancer cells based on individual genetic profiles, moving away from one-size-fits-all approaches. For instance, therapies targeting specific mutations like KRAS are under investigation, offering hope for improved efficacy and reduced side effects.

Additionally, immunotherapy is emerging as a promising avenue for treatment, with novel agents designed to activate the immune system against pancreatic cancer cells. This shift towards incorporating immune-based strategies signifies a transformative approach to managing this aggressive cancer type.

Market Segmentation

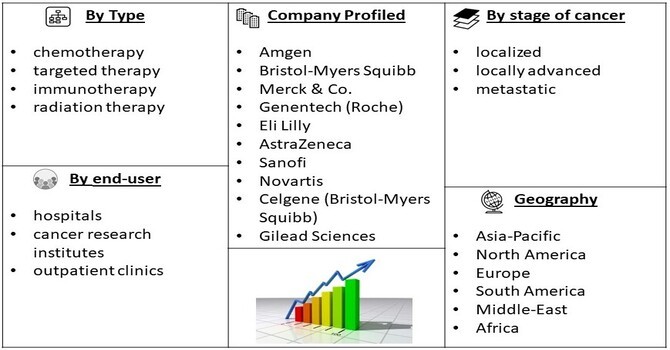

The global pancreatic cancer market is segmented by therapy type (chemotherapy, targeted therapy, immunotherapy, and radiation therapy), stage of cancer (localized, locally advanced, and metastatic), end-user (hospitals, cancer research institutes, and outpatient clinics), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). This segmentation provides insights into market dynamics, helping stakeholders identify growth opportunities in specific areas.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The rising incidence of pancreatic cancer is becoming a critical concern and a significant driver for market growth. Several factors contribute to the increasing prevalence of this aggressive disease. Age is a major risk factor, as pancreatic cancer is more commonly diagnosed in older adults, particularly those over 65. The global aging population means that a larger segment of the population is entering the high-risk age group. Additionally, lifestyle factors such as obesity and smoking are contributing to the rise in cases. Obesity is linked to chronic inflammation and insulin resistance, both of which can facilitate cancer development. Similarly, smoking is a well-established risk factor, with studies indicating that smokers are significantly more likely to develop pancreatic cancer than non-smokers.

Furthermore, genetic predisposition plays a vital role, with inherited mutations such as those in the BRCA2 gene and familial syndromes like Lynch syndrome increasing the risk. As awareness of these risk factors grows, healthcare systems are emphasizing the importance of early detection and effective management strategies. This shift is fostering initiatives aimed at educating both healthcare professionals and the public about symptoms and screening methods, leading to earlier diagnosis and better outcomes.

Technological advancements in treatment modalities are revolutionizing the landscape of pancreatic cancer care. The development of novel chemotherapeutic agents has expanded the arsenal available to oncologists, offering more effective treatment options for patients. For example, recent advancements have led to the introduction of combination therapies that can enhance efficacy while potentially mitigating side effects.

Targeted therapies are another area of significant innovation. These therapies focus on specific molecular targets associated with cancer cells, allowing for more precise treatment that minimizes damage to surrounding healthy tissues. By understanding the genetic makeup of tumors, researchers can design drugs that specifically attack cancer cells harboring particular mutations, such as KRAS.

Furthermore, immunotherapy is emerging as a promising frontier in the treatment of pancreatic cancer. This approach harnesses the body’s immune system to identify and destroy cancer cells. Various strategies, including immune checkpoint inhibitors and CAR-T cell therapy, are currently under investigation, aiming to improve patient responses to treatment.

The landscape is further enriched by ongoing clinical trials and research initiatives, which are crucial for driving innovation. These studies not only test new drugs and combinations but also explore biomarkers that can predict treatment responses, leading to more personalized care. As a result, patients have access to an increasingly diverse range of treatment regimens, improving overall survival rates and quality of life.

Market Restraints

One significant market restraint for the pancreatic cancer treatment market is the high cost of novel therapies. As advancements in treatment options, such as targeted therapies and immunotherapies, emerge, they often come with substantial financial implications. These cutting-edge therapies are typically the result of extensive research and development, which involves significant investment in clinical trials and regulatory approvals. This investment is reflected in the pricing of these therapies, making them costly for healthcare systems and patients alike.

The high costs associated with novel treatments can limit patient access, especially in low- to middle-income regions where healthcare resources are constrained. For many patients, the financial burden of these therapies can be prohibitive, leading to difficult choices between treatment and other essential expenses. This economic barrier is particularly concerning given that pancreatic cancer often requires aggressive and immediate intervention, and delays in treatment can negatively impact outcomes.

Moreover, the reimbursement landscape can further complicate access to these therapies. Not all insurance plans may cover the latest treatments, particularly if they are considered experimental or if the clinical evidence supporting their use is still evolving. This lack of coverage can lead to significant out-of-pocket costs for patients, creating disparities in access to care. In some cases, patients may be forced to forego effective treatment options simply due to financial constraints, resulting in worse health outcomes.

Segmental Analysis

The targeted therapy segment is poised to hold a significant share of the pancreatic cancer market due to its promising potential for improved efficacy and reduced side effects compared to traditional chemotherapy. Unlike conventional chemotherapy, which indiscriminately affects both cancerous and healthy cells, targeted therapies are designed to hone in on specific molecular targets associated with pancreatic cancer cells. This precision reduces the collateral damage often seen with chemotherapy, leading to fewer adverse effects and improved quality of life for patients during treatment. Recent advancements in understanding the molecular mechanisms underlying pancreatic cancer have been pivotal in the development of targeted agents. For instance, researchers have identified various genetic mutations and signaling pathways that drive tumor growth and progression in pancreatic cancer, such as mutations in the KRAS gene. This knowledge has paved the way for developing agents that specifically inhibit these pathways, effectively halting cancer cell proliferation while minimizing impact on normal cells. As a result, patients may experience enhanced treatment responses and longer survival rates.

Furthermore, ongoing clinical trials are expanding the landscape of targeted therapies, exploring combinations with immunotherapy or other treatment modalities to maximize therapeutic efficacy. The growing body of evidence supporting the effectiveness of these agents is expected to drive their adoption and integration into standard treatment protocols, further solidifying the targeted therapy segment's dominance in the market.

The hospital segment is anticipated to dominate the pancreatic cancer market, primarily because they provide comprehensive cancer care, including advanced diagnostic and treatment services. Hospitals are equipped with the necessary infrastructure, technology, and multidisciplinary teams to deliver integrated care to patients with complex conditions like pancreatic cancer.

One of the key advantages of hospitals is their ability to offer state-of-the-art diagnostic tools, such as advanced imaging techniques and endoscopic procedures, which are essential for accurate diagnosis and staging of pancreatic cancer. These capabilities allow healthcare providers to make informed treatment decisions, ensuring patients receive timely and appropriate care. Moreover, hospitals typically feature specialized oncology departments staffed with multidisciplinary teams, including medical oncologists, surgical oncologists, radiologists, and pathologists. This collaborative approach enhances patient outcomes by facilitating personalized treatment plans that consider the unique characteristics of each patient's cancer. The integration of various specialties allows for comprehensive management, from diagnosis through treatment and follow-up care.

The presence of cutting-edge technologies and innovative treatment modalities within hospital settings also drives demand for pancreatic cancer therapies. As hospitals invest in the latest advancements, such as targeted therapies and immunotherapies, they position themselves as leaders in cancer care. This investment not only improves treatment options available to patients but also enhances the reputation of the institutions as centers of excellence in oncology.

In summary, the targeted therapy segment's dominance stems from its ability to offer more effective and less toxic treatment options, while the hospital segment leads in market share due to its comprehensive care capabilities, advanced technologies, and collaborative approach to patient management. Together, these dynamics are shaping the future of pancreatic cancer treatment, ultimately aiming for better patient outcomes and quality of life.

Regional Analysis

North America is projected to maintain a dominant position in the global pancreatic cancer market, and several key factors underpin this leadership. One of the primary drivers is the high prevalence of pancreatic cancer in the region. Various lifestyle factors, such as obesity, smoking, and an aging population, contribute to the increasing incidence of this aggressive disease. As the population ages, the risk of developing pancreatic cancer rises, prompting a greater demand for effective diagnostic and treatment options.

The region also boasts an advanced healthcare infrastructure, characterized by state-of-the-art medical facilities, cutting-edge technology, and a well-trained workforce. This infrastructure facilitates the delivery of comprehensive cancer care, enabling timely diagnosis and access to the latest treatment modalities. Hospitals and specialized cancer centers in North America are equipped with advanced imaging techniques and innovative surgical options, which enhance the overall management of pancreatic cancer patients.

Moreover, significant investments in research and development play a crucial role in solidifying North America's leadership in the pancreatic cancer market. The presence of leading pharmaceutical and biotechnology companies in the region fosters a robust pipeline of innovative therapies. These companies are engaged in extensive clinical trials and research initiatives aimed at discovering new treatment options, such as targeted therapies and immunotherapies, which are critical for improving patient outcomes. The collaboration between academia and industry further accelerates the development of novel therapies and ensures that North American patients benefit from cutting-edge treatments.

Another vital aspect contributing to the region's dominance is the favorable reimbursement policies that support access to advanced treatment options. Many insurance plans in North America provide coverage for the latest therapies, including targeted and immunotherapies, making them accessible to a broader patient population. This financial support encourages healthcare providers to adopt these innovative treatments, knowing that patients can afford them. Consequently, the positive reimbursement environment promotes greater utilization of advanced cancer therapies, driving overall market growth.

To Learn More About This Report - Request a Free Sample Copy

The pancreatic cancer market is characterized by the presence of several prominent players, including Amgen, Bristol-Myers Squibb, Merck & Co., Genentech, and Eli Lilly. These companies play a pivotal role in shaping the landscape of pancreatic cancer treatment through their commitment to innovation and strategic growth initiatives.

Innovation is at the forefront of these companies’ strategies. As the understanding of pancreatic cancer evolves, these firms are investing heavily in the research and development of new therapeutic agents. This includes not only traditional chemotherapeutics but also cutting-edge treatments such as targeted therapies and immunotherapies. For instance, Merck’s development of immune checkpoint inhibitors has revolutionized the treatment landscape for various cancers, and ongoing research aims to extend these benefits to pancreatic cancer patients.

Expanding product portfolios is another crucial aspect of their competitive strategy. Leading companies are actively seeking to diversify their offerings by introducing novel agents that address unmet medical needs in pancreatic cancer treatment. This might involve repurposing existing drugs or developing combination therapies that leverage multiple mechanisms of action. For example, Bristol-Myers Squibb is exploring combinations of immunotherapies and targeted agents to enhance treatment efficacy in pancreatic cancer, addressing the unique challenges presented by this aggressive disease.

Here are the prominent players in the pancreatic cancer market

These companies are involved in the development of various therapeutic agents and treatment options for pancreatic cancer, focusing on innovations such as targeted therapies and immunotherapies.

Recent Developments

Q1. What are the driving factors for the Global Pancreatic Cancer Market?

The global pancreatic cancer market is experiencing significant growth, primarily driven by several key factors. First and foremost is the increasing incidence of pancreatic cancer, which is among the most aggressive and challenging forms of cancer to treat. As lifestyle factors such as obesity and smoking, along with genetic predispositions, contribute to a rise in cases, the demand for effective treatment solutions continues to escalate.

Q2. What are the restraining factors for the Global Pancreatic Cancer Market?

The global pancreatic cancer market faces several significant challenges that can hinder its growth and the development of effective treatment solutions. One of the most pressing issues is the high cost of treatment. Innovative therapies, including targeted treatments and immunotherapies, often come with substantial price tags that can limit accessibility for patients, particularly in regions with constrained healthcare budgets. This financial barrier may prevent many patients from receiving timely and necessary care, leading to poorer outcomes and exacerbating the burden of the disease.

Q3. Which segment is projected to hold the largest share of the Global Pancreatic Cancer Market?

The targeted therapy segment is expected to dominate the pancreatic cancer market, driven by its promising ability to enhance treatment efficacy while minimizing adverse side effects compared to traditional therapies. Targeted therapies are designed to specifically attack cancer cells by focusing on the unique genetic and molecular characteristics of tumors, thereby sparing healthy tissue and reducing the collateral damage often associated with conventional chemotherapy.

Q4. Which region holds the largest share of the Global Pancreatic Cancer Market?

North America is poised to dominate the pancreatic cancer market, primarily due to its advanced healthcare infrastructure, which includes state-of-the-art medical facilities, a network of specialized cancer centers, and access to cutting-edge diagnostic and treatment technologies. This robust infrastructure enables timely and effective patient care, crucial for addressing the complexities of pancreatic cancer, a disease that often requires multidisciplinary approaches for optimal management.

Q5. Who are the prominent players in the Global Pancreatic Cancer Market?

Key players in the global pancreatic cancer market, including Amgen, Bristol-Myers Squibb, Merck & Co., Genentech, and Eli Lilly, are at the forefront of innovation, significantly shaping the landscape of treatment options for this challenging disease. These companies leverage their extensive research capabilities and robust pipelines to develop novel therapies aimed at improving patient outcomes.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model