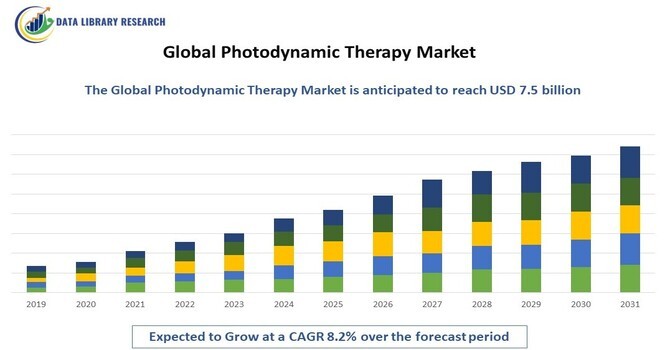

The global photodynamic therapy (PDT) market was valued at approximately USD 4.1 billion in 2023 and is projected to reach around USD 7.5 billion by 2031, reflecting a compound annual growth rate (CAGR) of about 8.2% from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

Photodynamic therapy is a minimally invasive treatment that utilizes light-sensitive compounds, known as photosensitizers, and light exposure to induce a photochemical reaction that destroys cancerous cells. PDT is increasingly recognized for its efficacy in treating various cancers, skin disorders, and other medical conditions. The rising prevalence of cancer and the demand for effective and less invasive treatment modalities are key drivers for the growth of this market. Furthermore, ongoing advancements in PDT technologies, including the development of novel photosensitizers and light delivery systems, are expanding the therapeutic applications and improving patient outcomes.

In addition to its established applications in oncology, photodynamic therapy (PDT) is gaining traction in treating non-cancerous conditions, such as acne, psoriasis, and age-related macular degeneration. This broadening scope of use is attributed to the therapy's ability to selectively target abnormal cells while minimizing damage to surrounding healthy tissue, which enhances patient safety and satisfaction. The integration of PDT with other treatment modalities, such as immunotherapy and laser therapy, is also being explored to enhance therapeutic efficacy and improve clinical outcomes. As research continues to unveil the potential benefits of PDT across various medical fields, increased investment in clinical trials and technological innovations is expected to drive market growth further, positioning PDT as a versatile and valuable option in modern medical treatment.

Key trends shaping the photodynamic therapy market include the increasing adoption of PDT in dermatology and oncology due to its targeted action and minimal side effects compared to traditional therapies. Innovations in photosensitizer development, such as the use of nanoparticles and combination therapies, are enhancing the efficacy and specificity of PDT, leading to improved treatment results. Additionally, the integration of PDT with other treatment modalities, such as immunotherapy and chemotherapy, is gaining traction, offering synergistic effects that enhance therapeutic outcomes. The growing focus on personalized medicine is also influencing the PDT landscape, with tailored treatment plans being developed based on individual patient profiles. Furthermore, the expansion of clinical applications beyond oncology, including the treatment of age-related macular degeneration and chronic skin conditions, is contributing to the market's growth and diversification.

Market Segmentation

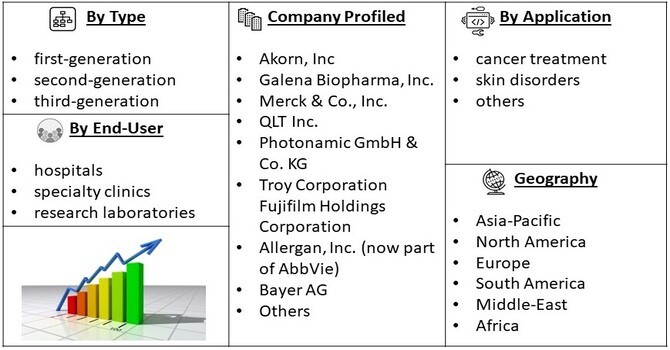

The photodynamic therapy market is segmented by application (cancer treatment, skin disorders, and others), photosensitizer type (first-generation, second-generation, and third-generation), end-user (hospitals, specialty clinics, and research laboratories), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). This segmentation provides valuable insights into market dynamics, enabling stakeholders to identify growth opportunities in specific areas. Among the various applications, cancer treatment is expected to hold the largest market share, driven by the rising incidence of cancer and the increasing adoption of PDT as a standard treatment modality in oncology.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The rising incidence of cancer and skin disorders globally significantly drives the growth of the photodynamic therapy market. According to the World Health Organization (WHO), cancer cases are expected to increase, with projections indicating nearly 30 million new cases annually by 2040. As cancer treatments traditionally involve invasive procedures with significant side effects, there is a growing demand for effective, less invasive alternatives like PDT. This therapy utilizes light-sensitive compounds to selectively target and destroy malignant cells, providing a targeted approach that minimizes harm to surrounding healthy tissues. Moreover, PDT is effective in treating various types of skin disorders, including actinic keratosis and acne, which further expands its market potential. As awareness of PDT's benefits grows among healthcare professionals and patients, the demand for such innovative treatments is anticipated to surge, propelling market growth.

Ongoing advancements in photodynamic therapy technologies are significantly influencing market growth. Innovations in photosensitizers and light delivery systems are enhancing the efficacy and safety of PDT, making it applicable to a broader range of medical conditions. For instance, the development of novel photosensitizers that are more effective and have fewer side effects allows for improved treatment outcomes and patient compliance. Additionally, advancements in light delivery methods, such as the use of targeted laser systems and portable light sources, enable more precise application and customization of therapy based on individual patient needs. This technological progress not only increases the range of treatable conditions but also improves overall patient experiences, leading to higher adoption rates among healthcare providers. As research continues to drive these innovations, the PDT market is expected to witness significant growth and expansion into new therapeutic areas.

Market Restraints

Despite its promising potential, the photodynamic therapy market faces several challenges, including limitations related to photosensitizer stability and light delivery efficiency. The effectiveness of PDT is often dependent on the precise activation of photosensitizers, which can be hindered by factors such as tissue penetration and the availability of optimal light sources. Additionally, the high cost of PDT equipment and treatments may restrict access for some patients, particularly in emerging markets with budget constraints. Regulatory hurdles and the lengthy approval process for new photosensitizers can also impede the introduction of innovative products in the market. Furthermore, the lack of awareness and understanding of PDT among healthcare professionals and patients may limit its adoption, necessitating educational initiatives to highlight its benefits and applications.

The COVID-19 pandemic has had a multifaceted impact on the photodynamic therapy (PDT) market, both presenting challenges and creating opportunities. Initially, the pandemic led to the postponement of non-emergency medical procedures, including cancer treatments, as healthcare systems focused on managing COVID-19 cases. This resulted in a temporary decline in the demand for PDT, as patients faced delays in diagnosis and treatment. However, as the situation evolved, there has been a renewed emphasis on developing and utilizing less invasive and more efficient treatment modalities to accommodate the growing backlog of patients needing care. PDT has gained attention as a promising alternative, particularly due to its minimal invasiveness and ability to target specific cancer cells while preserving healthy tissue. Additionally, the pandemic highlighted the need for innovative therapies that can be administered in outpatient settings, further bolstering interest in PDT as a viable option for cancer and skin disorder treatment. As healthcare systems adapt to the post-pandemic landscape, the PDT market is poised for recovery and growth, driven by the demand for advanced treatment solutions.

Segmental Analysis

Cancer treatment is poised to maintain a dominant position in the photodynamic therapy (PDT) market, driven by the increasing prevalence of cancer globally and the demand for innovative therapeutic options. As traditional cancer treatments like chemotherapy and radiation often come with severe side effects, PDT offers a minimally invasive alternative that targets tumor cells while sparing healthy tissue. This precision not only improves patient outcomes but also enhances the overall quality of life during treatment. The ongoing research and development in novel photosensitizers and light delivery systems are further expanding the applications of PDT in various cancer types, including skin, lung, and bladder cancers. Additionally, the rising awareness among healthcare professionals about the effectiveness and safety of PDT is fueling its adoption in clinical settings. Supportive government initiatives and favorable reimbursement policies are also contributing to the growth of PDT in cancer care. As healthcare providers seek more effective and less harmful treatment modalities, photodynamic therapy is expected to solidify its position as a cornerstone in modern oncology.

First-generation photodynamic therapy (PDT) agents are expected to maintain a dominant position in the market due to their established efficacy and safety profiles. These agents, primarily based on hematoporphyrin derivatives, have been extensively studied and are widely used in clinical applications, particularly for the treatment of superficial cancers and certain skin disorders. Their long history of use has built significant clinician and patient confidence, facilitating their continued preference in clinical practice. Additionally, first-generation photosensitizers exhibit strong absorption characteristics in the red light spectrum, allowing for effective light penetration into tissues. This makes them particularly suitable for treating tumors located close to the skin surface. The ongoing development of combination therapies, integrating first-generation PDT with other treatment modalities, is also enhancing their effectiveness and broadening their therapeutic applications. As a result, first-generation agents are likely to remain a cornerstone in the photodynamic therapy landscape, supported by their proven clinical outcomes and familiarity among healthcare professionals.

Hospitals are expected to maintain a dominant position in the photodynamic therapy (PDT) market, primarily due to their role as key providers of advanced cancer treatments and specialized care. These healthcare facilities are equipped with state-of-the-art technologies and trained medical professionals who can administer PDT effectively, ensuring optimal patient outcomes. The rising prevalence of cancer and skin disorders is driving an increased patient influx to hospitals, where comprehensive treatment options are available. Additionally, hospitals often serve as centers for clinical research, fostering innovation in PDT techniques and facilitating the development of new photosensitizers and light delivery systems. The integration of PDT into hospital oncology departments is further supported by growing awareness among healthcare providers about the benefits of minimally invasive treatment options. Moreover, hospitals benefit from established reimbursement frameworks, making PDT more accessible to patients. This combination of factors positions hospitals as critical players in the photodynamic therapy market, enabling them to address the rising demand for effective and less invasive treatment modalities.

Regional Analysis

North America is expected to maintain a dominant position in the photodynamic therapy market, driven by a well-established healthcare infrastructure and significant investments in research and development. The presence of leading pharmaceutical companies and academic institutions in the region facilitates innovation in PDT technologies and treatment approaches. Furthermore, the rising prevalence of cancer and skin disorders, coupled with increasing awareness of advanced treatment options, is fueling demand for photodynamic therapy in North America.

Additionally, the region benefits from a strong regulatory framework that supports the approval and commercialization of new photodynamic therapy products, further enhancing market growth. Pioneering clinical studies and trials conducted by renowned institutions contribute to the validation and refinement of PDT techniques, ensuring their effectiveness and safety in diverse applications. The increasing focus on personalized medicine also plays a crucial role in shaping the photodynamic therapy landscape, as healthcare providers seek tailored treatments that align with individual patient needs. Moreover, rising disposable incomes and a growing emphasis on preventive healthcare measures are leading more patients to explore advanced therapeutic options like PDT. As a result, North America is poised to continue its leadership in the photodynamic therapy market, setting trends that influence global practices and innovations in cancer treatment and beyond.

To Learn More About This Report - Request a Free Sample Copy

The photodynamic therapy market is characterized by a competitive landscape comprising several key players focused on innovation and strategic partnerships to enhance their market presence. Companies are investing in research and development to improve photosensitizer formulations, light delivery systems, and combination therapies. The competitive environment encourages collaborations with healthcare institutions and research organizations to advance clinical applications and broaden product offerings. Prominent players in the market include companies such as BioVex, Inc., Galderma S.A., Sirtex Medical Limited, and Photomedex, Inc., known for their extensive portfolios and commitment to developing effective PDT solutions. The competitive dynamics are expected to intensify as new entrants and established players strive to capitalize on the growing demand for photodynamic therapy across various medical applications.

Here are ten major players in the photodynamic therapy market

These companies are key contributors to the growth and advancement of photodynamic therapy, focusing on research, product development, and commercialization of innovative treatment options.

Recent Developments

Q1. What are the primary drivers of the photodynamic therapy market?

The photodynamic therapy market is driven by the increasing incidence of cancer and skin disorders, the demand for minimally invasive treatment options, and ongoing advancements in PDT technologies. The focus on personalized medicine and the growing awareness of PDT among healthcare providers and patients also contribute to market growth. Additionally, the photodynamic therapy market is benefiting from a surge in clinical research and development activities aimed at enhancing treatment efficacy and expanding the range of applications for PDT. The introduction of novel photosensitizers and improved light delivery systems is enabling more targeted and effective therapies, further appealing to both patients and healthcare professionals.

Q2. Which segment is anticipated to hold the largest market share?

The cancer treatment segment is expected to dominate the photodynamic therapy market, driven by the rising prevalence of various cancers and the increasing adoption of PDT as an effective therapeutic option in oncology. Moreover, the cancer treatment segment's dominance in the photodynamic therapy market is further fueled by ongoing advancements in PDT technologies, which enhance the precision and effectiveness of cancer treatments. Researchers are continuously developing new photosensitizers with improved targeting capabilities, leading to better patient outcomes and minimizing side effects.

Q3. What challenges does the market face?

Key challenges for the photodynamic therapy market include limitations related to photosensitizer stability, high treatment costs, regulatory hurdles, and a lack of awareness among healthcare professionals and patients. In addition to the aforementioned challenges, the photodynamic therapy market faces difficulties related to the specificity and depth of light penetration required for effective treatment. While certain photosensitizers can target cancerous tissues, ensuring adequate light exposure to these areas can be problematic, particularly in deeper tumors or complex anatomical regions. Furthermore, the variability in individual patient responses to PDT can lead to inconsistent treatment outcomes, creating hesitancy among healthcare providers to fully adopt this modality.

Q4. Which region is expected to hold the largest share of the market?

North America is projected to hold the largest share of the photodynamic therapy market, supported by a robust healthcare infrastructure, significant investments in research, and a rising prevalence of cancer and skin disorders. In addition to its established healthcare infrastructure, North America benefits from a collaborative environment among leading pharmaceutical companies, academic institutions, and research organizations, which fosters innovation in photodynamic therapy (PDT) technologies. The region's commitment to advancing cancer treatment through cutting-edge research and clinical trials has resulted in the development of novel photosensitizers and improved light delivery systems, enhancing the efficacy of PDT.

Q5. Who are the prominent players in the market?

Prominent players in the photodynamic therapy market include BioVex, Inc., Galderma S.A., Sirtex Medical Limited, and Photomedex, Inc., known for their innovative PDT solutions and commitment to advancing treatment efficacy.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model