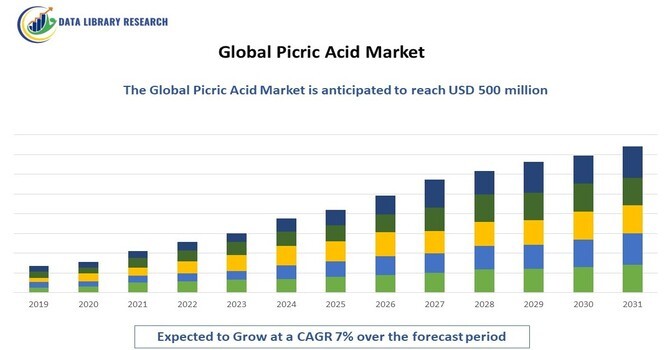

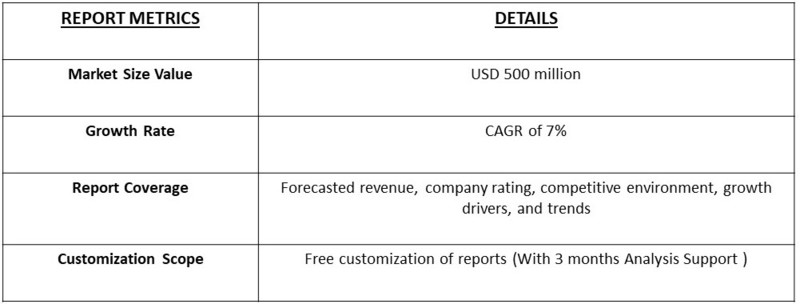

The global picric acid market was valued at approximately $300 million in 2023 and is projected to reach around $500 million by 2031, reflecting a compound annual growth rate (CAGR) of about 7% from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

Picric acid, a yellow crystalline compound, is primarily known for its applications in the production of explosives, dyes, and pharmaceuticals. Its significance in various industrial applications, coupled with the increasing demand for military-grade explosives and specialty chemicals, is driving market growth.

The picric acid market is also witnessing significant growth due to its applications beyond explosives, particularly in the pharmaceutical and agricultural sectors. In pharmaceuticals, picric acid is utilized as an important intermediate in the synthesis of various drugs, including anti-inflammatory and antiseptic agents, which are gaining traction in modern medicine. Moreover, in agriculture, its derivatives are being explored for use as herbicides and pesticides, contributing to improved crop yields and pest management. This diversification of applications is driving additional demand and encouraging manufacturers to innovate and adapt their production processes. Furthermore, as sustainability becomes increasingly important, companies are investing in greener alternatives and eco-friendly practices within the picric acid supply chain. This dual focus on innovation and compliance with environmental standards positions the picric acid market for resilient growth, catering to the evolving needs of multiple industries in a rapidly changing economic landscape.

Key trends influencing the picric acid market include the rising demand for explosives in military applications and mining operations, as well as the growth of the pharmaceutical industry where picric acid is utilized in the synthesis of drugs. Additionally, increasing investments in research and development for safer manufacturing practices and the development of eco-friendly alternatives are shaping market dynamics. The trend toward automation and efficiency in production processes is also leading to improved yields and reduced waste, enhancing the overall sustainability of picric acid production.

Another significant trend in the picric acid market is the increasing regulatory scrutiny surrounding chemical safety and environmental impact. Governments worldwide are implementing stricter regulations governing the handling, storage, and disposal of hazardous chemicals, including picric acid. This has prompted manufacturers to adopt more stringent safety protocols and invest in advanced monitoring and control systems to ensure compliance. Furthermore, companies are actively seeking certifications and endorsements to demonstrate their commitment to safety and environmental sustainability, which can enhance their market reputation and competitive edge. As awareness grows about the potential risks associated with chemical production, stakeholders in the picric acid market are prioritizing sustainable practices, which not only mitigate regulatory risks but also appeal to environmentally conscious consumers and investors. This proactive approach is expected to drive innovation in manufacturing techniques and promote the development of safer, more sustainable picric acid derivatives

Market Segmentation

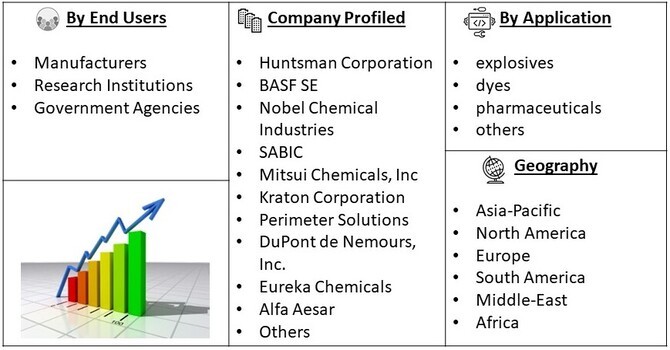

The global picric acid market is segmented by form (Powder, Liquid & Granules), application (explosives, dyes, pharmaceuticals, and others), End Users (Manufacturers, Research Institutions, and Government Agencies), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). This segmentation offers valuable insights into market dynamics, enabling stakeholders to identify growth opportunities in specific areas.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The rising demand for explosives, particularly in the defense and construction sectors, is a significant driver of the picric acid market. Picric acid is an essential ingredient in the formulation of military-grade explosives, making it crucial for various applications, including artillery shells and demolition explosives. The ongoing geopolitical tensions and increased defense budgets in several countries are contributing to the growth of this segment. Additionally, the mining industry’s requirement for efficient blasting agents to extract minerals is propelling the demand for picric acid. As mining operations expand globally, the need for effective and reliable explosives will drive the market forward.

In addition to the growing demand in defense and mining, the pharmaceutical sector is emerging as a vital contributor to the picric acid market. The compound is increasingly recognized for its role as an intermediate in the synthesis of various therapeutic agents, including anti-inflammatory drugs and antiseptics. As the global healthcare landscape evolves, there is a heightened focus on developing innovative pharmaceutical products that utilize picric acid, thus expanding its application range. The rising prevalence of chronic diseases and the subsequent demand for effective treatments are further fueling the pharmaceutical industry, leading to increased investments in drug development. Moreover, as research progresses into new formulations that harness the properties of picric acid, the market is likely to benefit from new opportunities and applications, enhancing its growth potential in a diversified landscape. This trend underscores the importance of picric acid beyond explosives, highlighting its versatility and relevance in addressing contemporary health challenges.

The pharmaceutical industry's expansion is another key factor propelling the picric acid market. Picric acid is used as an intermediate in the synthesis of various drugs and pharmaceutical products, including antiseptics and anti-inflammatory agents. The increasing prevalence of diseases and the rising focus on healthcare infrastructure are driving the demand for pharmaceuticals, thereby increasing the consumption of picric acid. Furthermore, advancements in drug formulations and the development of novel therapeutics are anticipated to create new opportunities for picric acid utilization in the pharmaceutical sector.

Moreover, the trend toward sustainability and eco-friendly practices in the pharmaceutical industry is also influencing the picric acid market. As companies prioritize green chemistry principles, there is a growing interest in optimizing synthetic routes that utilize picric acid in a more environmentally responsible manner. Researchers are exploring methods to minimize waste and reduce the environmental impact of picric acid production while maintaining efficiency and efficacy in drug development. This shift not only aligns with global sustainability goals but also enhances the market appeal of picric acid among manufacturers committed to responsible practices. Additionally, collaborations between chemical suppliers and pharmaceutical companies are fostering innovation in using picric acid to develop more sustainable products. As a result, the picric acid market is positioned to benefit from the dual trends of pharmaceutical growth and sustainability, highlighting its critical role in the future of drug development.

Market Restraints

The toxicity and environmental concerns associated with picric acid pose significant restraints on the market. The compound is highly explosive and hazardous if not handled properly, leading to stringent regulatory frameworks governing its production, storage, and transportation. These regulations can increase compliance costs for manufacturers and restrict market growth, particularly for small to medium-sized enterprises. Additionally, competition from alternative compounds used in similar applications, such as ammonium nitrate in explosives, may limit market expansion.

The COVID-19 pandemic had a notable impact on the global picric acid market, disrupting supply chains and manufacturing processes. Lockdowns and restrictions led to temporary shutdowns of production facilities, resulting in decreased output and delays in project timelines, particularly in defense and construction sectors. However, the pandemic also prompted an increased focus on safety and regulatory compliance, pushing manufacturers to adopt safer and more sustainable practices. As the market recovers, a renewed emphasis on innovation and efficiency is expected to drive future growth in the picric acid sector.

As the global economy gradually recovers from the effects of the COVID-19 pandemic, the picric acid market is witnessing a rebound in demand across various sectors. The defense sector, in particular, is poised for growth as nations ramp up their military capabilities and invest in modernizing their arsenals, which includes the procurement of advanced explosives. Similarly, the construction industry is picking up momentum, leading to increased requirements for blasting agents in large-scale infrastructure projects. This resurgence is further supported by an uptick in research and development efforts aimed at enhancing the safety and efficiency of picric acid production. Moreover, as manufacturers adapt to the post-pandemic landscape, there is a concerted effort to implement innovative technologies that optimize production processes while adhering to stricter safety regulations. This combination of renewed demand and a focus on technological advancement positions the picric acid market for robust growth in the coming years, as industries seek reliable and effective solutions to meet their operational needs.

Segmental Analysis

The powder form of picric acid is anticipated to experience significant growth over the forecast period, driven by its wide range of applications in both military and industrial sectors. As a crucial ingredient in the formulation of explosives, the powdered variant offers advantages such as enhanced stability and ease of handling, making it preferable for various uses. The increasing demand for precision in military-grade explosives and mining operations is propelling the adoption of powdered picric acid. Additionally, advancements in manufacturing processes are improving the quality and purity of powdered picric acid, further boosting its appeal. As industries continue to seek efficient and effective solutions for their explosive needs, the powdered form of picric acid is well-positioned for robust market expansion.

The pharmaceuticals segment is anticipated to exhibit robust growth, driven by the expanding healthcare sector and the rising demand for novel drug formulations. As the global population ages and the prevalence of chronic diseases increases, the need for effective medications will fuel the demand for picric acid as a key intermediate in drug synthesis. Furthermore, ongoing research into new therapeutic applications is likely to enhance the role of picric acid in the pharmaceutical landscape.

In addition to the growing demand for pharmaceuticals, the picric acid market is also benefitting from an increase in collaborations and partnerships between pharmaceutical companies and research institutions. These alliances aim to explore innovative applications and improve the efficacy of existing drug formulations, thereby expanding the utilization of picric acid in various therapeutic areas. Moreover, the rising focus on personalized medicine is likely to create new opportunities for picric acid in developing tailored drug therapies that cater to individual patient needs. As regulatory bodies continue to support advancements in drug development and safety, picric acid is expected to play a pivotal role in the synthesis of next-generation therapeutics. This synergy between the pharmaceutical sector's growth and picric acid's versatile applications underscores its potential as a critical component in addressing the evolving healthcare challenges of the global population.

Manufacturers are increasingly recognizing the versatile applications of picric acid across various industries, driving its growing use in production processes. In the defense sector, picric acid is a vital component in formulating explosives, artillery shells, and demolition agents, making it essential for military applications. Additionally, its role as an intermediate in the pharmaceutical industry has gained traction, as it is utilized in synthesizing drugs, antiseptics, and anti-inflammatory agents. Manufacturers are also exploring eco-friendly alternatives and safer production methods to meet stringent regulatory standards and address environmental concerns. Moreover, the mining industry’s reliance on effective blasting agents is propelling demand for picric acid as extraction operations expand globally. The trend towards innovation and enhanced manufacturing processes further boosts picric acid's appeal, enabling manufacturers to optimize production efficiency and reduce waste. This growing adoption underscores the importance of picric acid as a key resource for manufacturers aiming to meet evolving market demands while ensuring compliance with safety and sustainability standards.

Regional Analysis

The Asia-Pacific region is expected to witness rapid growth in the global picric acid market, attributed to the increasing demand for explosives in mining and construction industries, along with the expanding pharmaceutical sector. Countries such as China and India are investing heavily in infrastructure development and military modernization, leading to heightened demand for explosives and specialty chemicals. Furthermore, the growing population and rising healthcare needs in this region are anticipated to bolster the pharmaceutical application of picric acid.

In addition to infrastructure and military investments, the Asia-Pacific region benefits from a favorable regulatory environment that encourages domestic production and innovation in the chemical industry. Governments are implementing policies to enhance safety standards and promote sustainable manufacturing practices, which are crucial for the picric acid market. Moreover, the presence of several key players in the chemical manufacturing sector, along with increasing research and development activities, is fostering competitive growth. The region’s strategic location, coupled with improving supply chain logistics, is also expected to enhance the availability and distribution of picric acid, further driving market expansion. As these trends continue, the Asia-Pacific region is poised to become a significant hub for picric acid production and consumption.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the global picric acid market is characterized by a diverse array of manufacturers and suppliers, ranging from large multinational corporations to smaller regional players. Key companies are focusing on strategic partnerships, mergers, and acquisitions to enhance their market presence and expand their product offerings. Innovation in production techniques and the development of safer, more sustainable manufacturing processes are critical competitive strategies, as regulatory compliance and environmental concerns become increasingly important. Additionally, players are investing in research and development to explore new applications of picric acid in pharmaceuticals and explosives, which is vital for maintaining a competitive edge. The market dynamics are further influenced by regional demand variations, with companies tailoring their strategies to address specific needs in emerging economies like Asia-Pacific, where growth potential is high. As competition intensifies, companies that can effectively balance quality, safety, and sustainability are likely to emerge as leaders in the picric acid market.

The picric acid market features several prominent players, including

These companies are key contributors to the picric acid market, driving innovation and offering a range of solutions to meet the needs of various industries worldwide.

Recent Developments

Q1. What are the driving factors for the Global Picric Acid Market?

The global picric acid market is primarily driven by increasing demand for explosives in military and construction applications, as well as growth in the pharmaceutical sector where picric acid is used as an intermediate in drug synthesis. The rising investments in defense infrastructure and advancements in healthcare are further propelling market growth.

Q2. What are the restraining factors for the Global Picric Acid Market?

Key challenges facing the picric acid market include toxicity and environmental concerns associated with the compound, which lead to stringent regulations that can increase compliance costs for manufacturers. Additionally, competition from alternative compounds in explosives applications may limit market expansion.

Q3. Which segment is projected to hold the largest share in the Global Picric Acid Market?

The explosives application segment is projected to hold the largest share of the picric acid market, driven by its essential role in military and commercial explosives, supported by ongoing defense modernization efforts.

Q4. Which region holds the largest share of the Global Picric Acid Market?

The Asia-Pacific region is expected to hold the largest share of the global picric acid market, bolstered by increasing demand for explosives in mining and construction industries, along with the expanding pharmaceutical sector.

Q5. Who are the prominent players in the Global Picric Acid Market?

Prominent players in the picric acid market, such as Huntsman Corporation, BASF SE, and Nobel Chemical Industries, are recognized for their commitment to innovation and sustainability in the production of picric acid and its applications. These companies are at the forefront of developing advanced solutions to meet the growing needs of various industries.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model