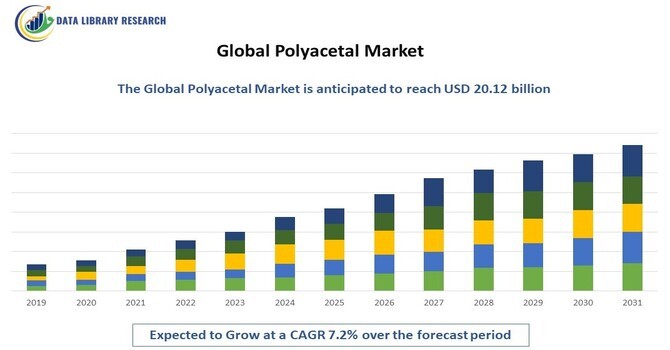

The global polyacetal market is projected to grow significantly, driven by rising demand across various industries such as automotive, electronics, and consumer goods. Polyacetal, also known as polyoxymethylene (POM), is a high-performance engineering thermoplastic known for its excellent mechanical properties, such as high stiffness, low friction, and outstanding dimensional stability. In 2023, the market was valued at around $10.2 billion and is expected to reach approximately $ 20.12 billion by 2031, reflecting a CAGR of 7.2% during the forecast period.

Get Complete Analysis Of The Report - Download Free Sample PDF

The global polyacetal market is experiencing significant growth, driven by increasing demand from industries such as automotive, electronics, and consumer goods. Polyacetal (POM) is a high-performance thermoplastic known for its excellent mechanical properties, including high strength, low friction, and durability, making it ideal for precision components. The automotive industry uses polyacetal in fuel systems, gears, and safety systems, while the electronics sector leverages its electrical insulation capabilities. Key trends include the rise of bio-based polyacetal, driven by environmental regulations and the push for sustainability. Asia-Pacific is the largest market due to rapid industrialization and growth in the automotive and electronics sectors. The market faces challenges from fluctuating raw material prices and hydrolysis issues but is poised for further expansion due to technological innovations and increased adoption of lightweight materials.

As industries continue to seek lightweight, durable materials to enhance product performance and reduce costs, polyacetal is emerging as a preferred choice. Technological advancements, particularly in the production of low-emission and eco-friendly polyacetal resins, are further propelling market growth. The increasing focus on sustainability and stringent regulations regarding emissions have created opportunities for innovation in bio-based polyacetal, positioning the market for substantial expansion.

Key trends in the polyacetal market include a growing shift towards bio-based polyacetals to meet sustainability goals. Rising consumer awareness and regulatory pressures are pushing manufacturers to develop eco-friendly alternatives. Additionally, advancements in polyacetal blends and composites are expanding its applications, especially in automotive and electronics, where lightweight and durable materials are essential for improving fuel efficiency and product longevity. The trend of miniaturization in electronics and automotive components is also driving demand for polyacetal due to its superior performance in small, intricate parts. Moreover, the adoption of Industry 4.0 and smart manufacturing technologies is boosting production efficiency, reducing costs, and ensuring better quality control, thereby accelerating market penetration.

Market Segmentation

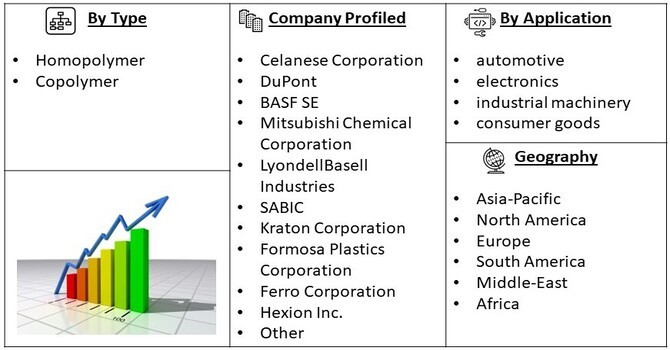

The global polyacetal market is segmented by type (homopolymer and copolymer), application (automotive, electronics, industrial machinery, and consumer goods), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa). This segmentation offers a comprehensive view of the market, highlighting key growth areas in each segment. Automotive remains the largest application sector due to the increasing demand for lightweight, durable materials. In terms of geography, Asia-Pacific is expected to dominate the market, driven by rapid industrialization, rising automotive production, and expanding electronics manufacturing.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The surge in demand for lightweight materials is significantly reshaping the automotive and electronics industries, propelling the growth of the polyacetal market. In the automotive sector, manufacturers are turning to polyacetal for critical components like fuel system parts, gears, and door handles due to its exceptional strength-to-weight ratio and resistance to wear and tear. This shift is driven by the industry's commitment to enhancing fuel efficiency and meeting stringent emissions regulations, as lighter vehicles consume less fuel. Concurrently, in the electronics domain, polyacetal's attributes such as outstanding electrical insulation properties and dimensional stability make it a preferred choice for precision parts, connectors, and switches. As technological advancements lead to the miniaturization of electronic devices, the need for high-performance materials that can withstand rigorous operating conditions is on the rise. Consequently, the ongoing trends towards light-weighting and energy efficiency in both sectors are expected to create a robust demand for polyacetal, ensuring its vital role in the evolution of modern manufacturing processes.

Innovations in polyacetal resins, including the development of high-performance copolymers and bio-based polyacetals, are driving market growth. Manufacturers are focusing on enhancing the material's properties, such as improving its chemical resistance and heat stability, to cater to more demanding applications in various sectors. These technological advancements not only expand polyacetal’s range of applications but also address environmental concerns by offering more sustainable solutions.

The ongoing innovations in polyacetal resins, particularly the introduction of high-performance copolymers and bio-based polyacetals, are significantly contributing to the market's expansion. Manufacturers are increasingly investing in research and development to enhance the properties of polyacetal, such as its chemical resistance, heat stability, and mechanical strength, enabling it to meet the stringent requirements of various demanding applications across multiple industries. These advancements are crucial as industries seek materials that can withstand harsher environments while maintaining performance and reliability. Furthermore, the shift towards bio-based polyacetals aligns with global sustainability initiatives, addressing environmental concerns by reducing dependency on fossil fuels and minimizing the carbon footprint associated with traditional polyacetals. This focus on sustainable alternatives not only attracts environmentally conscious consumers but also positions manufacturers favorably in a market that increasingly prioritizes eco-friendly practices. As a result, these innovations are expected to broaden polyacetal's application scope, reinforcing its relevance in an evolving marketplace.

Market Restraints

The primary challenge in the polyacetal market is its susceptibility to hydrolysis, which limits its use in applications exposed to moisture or high temperatures. Additionally, fluctuations in raw material prices and stringent environmental regulations related to plastic production and disposal pose significant restraints to market growth. These factors can lead to increased production costs and pressure on manufacturers to adopt greener practices, potentially affecting profit margins. The polyacetal market faces notable challenges that could hinder its growth trajectory, primarily stemming from its susceptibility to hydrolysis. This inherent vulnerability limits the material's application in environments where it is exposed to moisture or high temperatures, which can lead to degradation and performance issues over time. Furthermore, the market is affected by fluctuations in raw material prices, which can significantly impact production costs. As the demand for polyacetal increases, manufacturers are also confronted with stringent environmental regulations concerning plastic production and disposal. These regulations not only compel companies to adopt more sustainable manufacturing practices but also necessitate investments in compliance measures that can strain profit margins. As a result, navigating these challenges while meeting the evolving demands of customers and regulatory bodies presents a complex landscape for stakeholders in the polyacetal market, requiring continuous innovation and strategic planning to maintain competitiveness and ensure long-term viability.

The COVID-19 pandemic temporarily slowed down the polyacetal market, with disruptions in supply chains and a decline in demand from key industries such as automotive and electronics. However, as industries recover and economies reopen, the market is expected to regain momentum. The pandemic has also accelerated the adoption of automation and digitalization in manufacturing processes, boosting the demand for polyacetal in advanced machinery and equipment. The post-pandemic recovery is anticipated to be marked by an increased focus on sustainability and efficiency, further fueling the demand for innovative polyacetal solutions.

The COVID-19 pandemic had a notable impact on the polyacetal market, leading to temporary slowdowns due to supply chain disruptions and reduced demand from critical sectors like automotive and electronics. However, as economies gradually reopen and industries rebound, the market is poised for a robust recovery. The pandemic has also catalyzed a shift towards automation and digitalization in manufacturing processes, driving increased demand for polyacetal in advanced machinery and equipment, which require durable and high-performance materials. As businesses seek to enhance operational efficiency and sustainability in the post-pandemic landscape, the demand for innovative polyacetal solutions is expected to rise significantly. This renewed focus on sustainable practices, coupled with the integration of advanced manufacturing technologies, is likely to create new opportunities for growth within the polyacetal market, positioning it to meet the evolving needs of various industries while contributing to broader environmental goals.

Segmental Analysis

The growing use of polyacetal homopolymers is driven by their exceptional mechanical properties, including high strength, rigidity, and low friction, making them ideal for a wide range of applications. These homopolymers are increasingly favored in industries such as automotive, electronics, and consumer goods due to their excellent dimensional stability and resistance to wear. In automotive applications, polyacetal homopolymers are utilized in components like gears, fuel system parts, and structural elements, where performance under stress and temperature variations is crucial. The electronics sector also benefits from these materials for manufacturing precision components, connectors, and switches, capitalizing on their excellent electrical insulation properties. Additionally, the demand for lightweight materials in vehicle manufacturing has led to an increased adoption of homopolymers, contributing to improved fuel efficiency and reduced emissions. As manufacturers focus on enhancing product performance and longevity, the versatility of polyacetal homopolymers positions them as a preferred choice across various industries. Their ability to withstand harsh environments and their inherent chemical resistance further cement their role in advancing technology and innovation, ensuring robust growth in the polyacetal market.

The automotive sector is anticipated to hold the largest share of the polyacetal market, driven by the growing demand for lightweight, high-performance materials. Polyacetal’s use in fuel system components, safety systems, and various mechanical parts is expected to increase as automakers focus on improving vehicle efficiency and reducing emissions. The electronics segment is also expected to witness significant growth, as polyacetal’s excellent electrical insulation and dimensional stability make it ideal for high-precision components.

The industrial applications of polyacetal are also poised for considerable growth, fueled by the material’s exceptional mechanical properties and versatility. Industries such as manufacturing and machinery are increasingly incorporating polyacetal into components like gears, bearings, and guide rails due to its low friction, high wear resistance, and ability to maintain performance under stress. Additionally, the shift towards automation and the use of advanced machinery further amplify the demand for polyacetal in various industrial applications, where reliability and precision are paramount. As industries evolve and seek more efficient solutions, polyacetal’s attributes position it as a favored choice for a wide range of applications, ensuring sustained growth in this segment of the market. This diversification across multiple sectors not only solidifies polyacetal’s presence in the market but also enhances its resilience against economic fluctuations in any single industry.

Regional Analysis

Asia-Pacific is projected to dominate the global polyacetal market, owing to rapid industrial growth, rising automotive production, and expanding electronics manufacturing in countries like China, Japan, and South Korea. The region's strong manufacturing base and increasing investments in technology further boost demand. North America and Europe also represent significant markets, with a strong focus on innovation and sustainability driving demand for advanced polyacetal solutions.

Emerging economies within the Asia-Pacific region, such as India and Southeast Asian countries, are also expected to contribute significantly to the growth of the polyacetal market. As these nations continue to develop their industrial infrastructure and increase their manufacturing capabilities, the demand for high-performance materials like polyacetal will rise. Furthermore, the growing awareness of the need for lightweight and durable materials in various applications will stimulate market expansion. In North America, the automotive industry's shift toward electric vehicles (EVs) and lightweight components presents new opportunities for polyacetal applications, while Europe’s stringent environmental regulations encourage the development of sustainable polyacetal alternatives. Additionally, collaborations between manufacturers and research institutions in these regions are likely to lead to innovative product offerings, further enhancing market growth and competitiveness. Overall, the global polyacetal market is poised for robust growth as key regions leverage technological advancements and respond to changing industry demands.

To Learn More About This Report - Request a Free Sample Copy

The polyacetal market is highly competitive, with several key players investing in research and development to enhance product offerings and maintain market leadership. Major companies include Celanese Corporation, DuPont, Mitsubishi Chemical Holdings, BASF SE, and Polyplastics Co., Ltd. These players are focusing on product innovation, strategic partnerships, and expanding their global presence to capture emerging opportunities in the market. With increasing competition, companies are emphasizing sustainability, developing bio-based polyacetals, and improving product performance to cater to the growing demand from various industries.

Here are ten prominent players in the polyacetal market

These companies are involved in the development, production, and marketing of polyacetal materials, catering to various end-use applications.

Recent Developments

Q1. What are the driving factors for the Global Polyacetal Market?

The primary drivers for the polyacetal market include rising demand from the automotive and electronics sectors, coupled with technological advancements in material science. The push for lightweight, durable materials in various industries and the development of bio-based polyacetal are also key factors contributing to market growth.

Q2. What are the restraining factors for the Global Polyacetal Market?

Key challenges include susceptibility to hydrolysis, fluctuating raw material prices, and stringent environmental regulations, which can impact production costs and limit the application of polyacetal in certain environments.

Q3. Which segment is projected to hold the largest share in the Global Polyacetal Market?

The automotive segment is expected to hold the largest market share due to the increasing use of polyacetal in high-performance, lightweight components aimed at improving vehicle efficiency and reducing emissions.

Q4. Which region holds the largest share of the Global Polyacetal Market?

Asia-Pacific is anticipated to dominate the global polyacetal market, driven by rapid industrialization, expanding automotive and electronics sectors, and increasing technological investments in countries like China, Japan, and South Korea.

Q5. Who are the prominent players in the Global Polyacetal Market?

Prominent players include Celanese Corporation, DuPont, Mitsubishi Chemical Holdings, BASF SE, and Polyplastics Co., Ltd., who are focusing on product innovation and strategic collaborations to strengthen their market position.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model