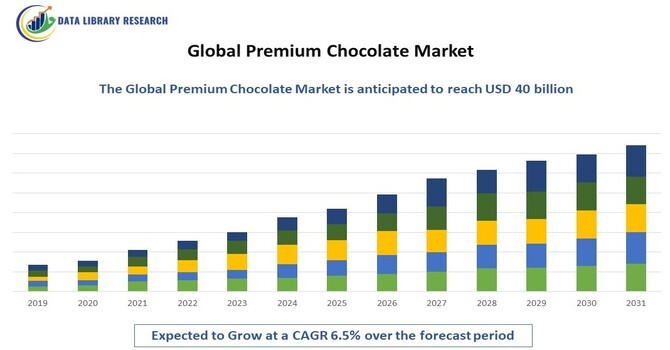

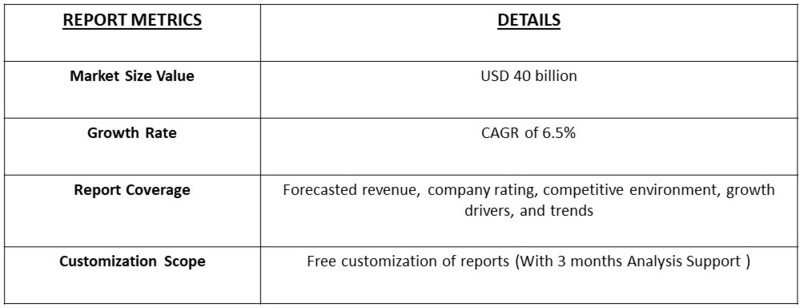

The global premium chocolate market is poised for substantial growth, with an anticipated market value of USD 25 billion in 2023, projected to reach USD 40 billion by 2031, representing a compound annual growth rate (CAGR) of 6.5% from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

This growth is driven by increasing consumer demand for high-quality, ethically sourced chocolates, along with a growing preference for indulgent treats and premium confectionery experiences.

Premium chocolate refers to high-quality chocolate products that typically contain a higher percentage of cocoa solids, are made from superior ingredients, and often emphasize artisanal craftsmanship. These chocolates often come in various forms, including dark, milk, and white varieties, and are frequently enriched with unique flavors and textures. The market is characterized by a shift toward gourmet offerings, with consumers willing to pay a premium for products that offer superior taste, quality, and ethical sourcing.

The premium chocolate market is witnessing several notable trends shaping its future landscape. One prominent trend is the rising demand for dark chocolate, attributed to its perceived health benefits and rich flavor profile. Additionally, there is a growing interest in ethically sourced and sustainable chocolate, with consumers increasingly preferring brands that demonstrate a commitment to fair trade practices and environmentally friendly production methods.

Another trend is incorporating unique flavors and ingredients, such as spices, fruits, and botanicals, which enhance the sensory experience of chocolate consumption. The rise of vegan and organic chocolate products is also noteworthy, catering to health-conscious consumers and those with dietary restrictions. Furthermore, the online retail channel is expanding rapidly, allowing premium chocolate brands to reach a broader audience while providing convenient purchasing options. Together, these trends indicate a dynamic evolution in the premium chocolate market, driven by consumer preferences for quality, sustainability, and unique experiences.

Market Segmentation:

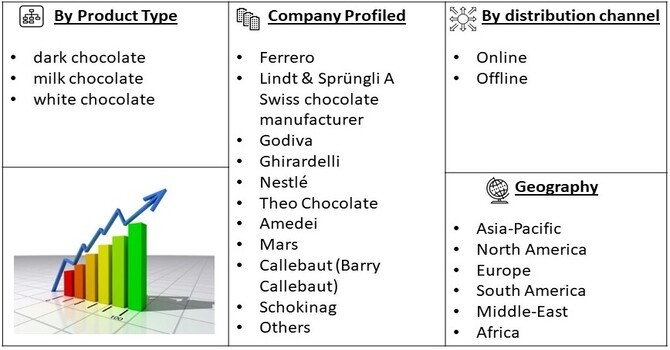

The global premium chocolate market is segmented by product type (dark chocolate, milk chocolate, and white chocolate), distribution channel (online, and offline), and geography (North America, Europe, Asia-Pacific, South America, and the Middle East and Africa). The report offers market size and forecasts for revenue (USD million) across all segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The growing demand for premium chocolate is primarily driven by consumers’ willingness to pay for high-quality products that offer exceptional taste and experience. With an increasing focus on indulgence and self-care, consumers are gravitating towards premium chocolate as a treat or gift option. Additionally, the rise of food tourism and gourmet experiences has popularized the appreciation for artisanal chocolate, further fueling demand for premium offerings.

As consumers become more conscious of the social and environmental impact of their purchases, the demand for ethically sourced and sustainably produced chocolate is on the rise. Brands that emphasize transparency in their supply chains and adhere to fair trade practices are increasingly favored by consumers. This focus on sustainability not only drives brand loyalty but also attracts a segment of environmentally-conscious consumers willing to invest in premium chocolate that aligns with their values.

Market Restraints

The premium chocolate market faces challenges due to the high cost of raw materials and production processes. The sourcing of high-quality cocoa and other ingredients often results in higher prices, which can limit accessibility for price-sensitive consumers. This pricing dynamic may restrict market growth, particularly in emerging economies where affordability is a key concern.

The premium chocolate market also contends with competition from a variety of alternative snacks and confectionery products. With a growing array of options, including healthier snack bars, nuts, and other indulgent treats, consumers may opt for alternatives that offer similar satisfaction at a lower price point.

The COVID-19 pandemic significantly impacted the global premium chocolate market, altering consumer behaviors and production dynamics. Lockdowns and restrictions initially disrupted supply chains, leading to shortages and increased costs for raw materials. However, as consumers sought comfort in indulgent treats during stressful times, demand for premium chocolate saw a resurgence, particularly in e-commerce channels. The shift toward online shopping and direct-to-consumer models became prominent, allowing brands to reach customers more effectively. Additionally, health and wellness trends prompted interest in chocolate with functional benefits, like reduced sugar or enhanced flavors. Overall, while the pandemic posed challenges, it also accelerated innovation and adaptation in the premium chocolate sector.

Segmental Analysis

The dark chocolate segment is projected to witness significant growth over the forecast period, driven by its popularity among health-conscious consumers who appreciate its potential health benefits, such as antioxidants and heart health support. This growing awareness, combined with the increasing variety of dark chocolate offerings, including those infused with exotic flavors, is likely to attract a broader consumer base.

The online distribution channel for premium chocolate is expected to experience rapid growth, fueled by the convenience of e-commerce and the expanding online presence of premium brands. As consumers increasingly turn to digital platforms for their shopping needs, brands that leverage effective online marketing strategies and provide direct-to-consumer options are well-positioned for growth in this segment.

North America is projected to hold a significant share of the premium chocolate market, driven by a strong demand for high-quality confectionery products and a growing preference for gourmet offerings. The presence of major premium chocolate brands, along with a well-established retail network, supports the region's market leadership. Additionally, rising disposable incomes and changing consumer preferences are expected to further bolster the growth of the premium chocolate market in North America.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the global premium chocolate market is characterized by a mix of established brands and emerging artisanal producers. Key players such as Ferrero, Lindt & Sprüngli, and Godiva are prominent in the market, leveraging their brand heritage and expertise in crafting high-quality chocolate products. These companies invest heavily in innovation, focusing on unique flavors and sustainable sourcing to meet evolving consumer demands. Emerging players, particularly artisanal and craft chocolate makers, are also gaining traction, appealing to niche markets that prioritize quality and local production. The emphasis on branding and storytelling around ethical sourcing and craftsmanship is becoming increasingly important in differentiating products within the competitive landscape.

Key Players

Recent Developments

Q1. What are the driving factors for the Global Premium Chocolate Market?

The global premium chocolate market is driven by increasing consumer demand for high-quality products, a growing interest in ethically sourced and sustainable chocolates, and the rising popularity of dark chocolate for its health benefits. Additionally, consumers' willingness to invest in indulgent experiences and the trend toward unique flavors and artisanal craftsmanship further contribute to market growth.

Q2. What are the restraining factors for the Global Premium Chocolate Market?

Despite its growth potential, the premium chocolate market faces challenges such as high production costs, competition from alternative snacks, and fluctuating cocoa prices. These factors may limit accessibility and deter price-sensitive consumers. Furthermore, regulatory challenges regarding food safety and labeling can also impact market dynamics.

Q3. Which segment is projected to hold the largest share in the Global Premium Chocolate Market?

The dark chocolate segment is projected to hold the largest share in the global premium chocolate market. Its popularity, driven by health-conscious consumers and the increasing variety of high-quality offerings, solidifies its dominance in the market.

Q4. Which region holds the largest share of the Global Premium Chocolate Market?

North America is expected to hold the largest share of the global premium chocolate market, supported by a strong demand for gourmet offerings, rising disposable incomes, and a well-established retail network. The region's consumer preferences for high-quality and ethically sourced products further reinforce its dominant position in the market.

Q5. Which are the prominent players in the Global Premium Chocolate Market?

Key players in the global premium chocolate market include Ferrero, Lindt & Sprüngli, Godiva, Ghirardelli, Nestlé, Theo Chocolate, and Amedei. These companies focus on product innovation, sustainable sourcing, and brand differentiation to maintain a competitive edge in the market.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model