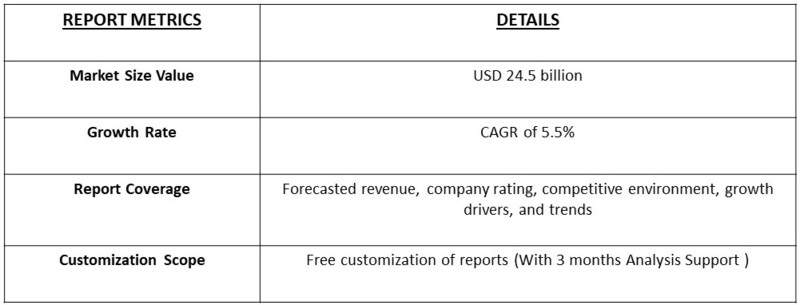

The Global Pumped Storage Hydropower (PSH) market is expected to reach a market value of 14.3 billion in 2023. By 2031, the market is projected to reach a value of 24.5 billion, with a CAGR of 5.5% from 2023 to 2031.

Get a Complete Analysis Of The Report - Download a Free Sample PDF

The Global Pumped Storage Hydropower Market refers to the deployment of large-scale energy storage systems that use the gravitational potential of water to store and generate electricity. These systems pump water to an elevated reservoir during periods of low electricity demand and release it through turbines during peak demand, providing grid stability and energy balancing. Pumped storage hydropower is a critical component for integrating renewable energy sources, such as wind and solar, by offering reliable backup during fluctuations in power generation. The market is driven by the need for flexible, efficient energy storage solutions to support growing renewable energy adoption and grid modernization efforts worldwide.

Global Pumped Storage Hydropower Market is the increasing integration of renewable energy sources, such as wind and solar, which require efficient energy storage solutions to manage intermittent power generation. Pumped storage hydropower offers grid stability by providing peak load balancing and energy storage capacity, helping to meet fluctuating electricity demand. Additionally, growing government initiatives to reduce carbon emissions and promote renewable energy projects are propelling investments in energy storage infrastructure. Technological advancements in turbine efficiency and the expansion of grid modernization projects are further boosting the demand for pumped storage hydropower solutions.

The global Pumped Storage Hydropower (PSH) market is witnessing a surge in demand, driven by the increasing adoption of renewable energy sources and the need for grid stability. Key trends include the growing focus on energy storage solutions, with PSH technology emerging as a viable option to mitigate the intermittency of solar and wind power. Additionally, the market is seeing a shift towards larger-scale PSH projects, with a focus on increasing efficiency and reducing costs. Furthermore, the integration of advanced technologies such as IoT and AI is expected to enhance the operational efficiency of PSH plants. As the market continues to evolve, we anticipate a growing emphasis on sustainability and environmental considerations in PSH project development.

The Global Pumped Storage Hydropwer Market is segmented By Type (Conventional, Open-loop, Closed-loop) By Application (Grid Energy Storage, Renewable Integration, Peak Load Management) and geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report offers the market size and forecasts for revenue (USD million) for all the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

The global Pumped Storage Hydropower (PSH) market is driven by the growing demand for renewable energy. Governments and corporations are setting ambitious targets to reduce carbon emissions and transition to cleaner energy sources. PSH technology is well-positioned to play a critical role in this transition, as it can store excess energy generated by solar and wind power for use during periods of high demand. For instance, the European Union's renewable energy target of at least 32% of gross final energy consumption by 2030 is expected to drive demand for PSH projects. Moreover, the increasing adoption of electric vehicles and the need for grid stability are also driving the demand for PSH technology.

Advancements in PSH technology and cost reductions are another key driver of the market. The development of more efficient turbines and pumps has reduced the cost of PSH projects, making them more competitive with other forms of energy storage. Additionally, the increasing use of digital technologies such as IoT and AI is enhancing the operational efficiency of PSH plants, reducing maintenance costs and increasing output. For instance, a recent study by the International Hydropower Association found that the cost of PSH technology has decreased by 30% over the past decade, making it a more viable option for energy storage. As technology continues to evolve, we expect to see further cost reductions and increased adoption of PSH technology.

One of the key restraints in the global Pumped Storage Hydropower (PSH) market is the growing concern over environmental and social impacts. PSH projects often require the construction of large dams, which can displace communities and disrupt ecosystems. Moreover, the alteration of natural water flows and the potential for water pollution are also major concerns. For instance, the proposed PSH project in the Amazon rainforest has been met with fierce opposition from local communities and environmental groups, highlighting the need for careful consideration of social and environmental impacts. As the market continues to evolve, we expect to see increased scrutiny of PSH projects and a greater emphasis on sustainable development and environmental stewardship.

The COVID-19 pandemic had a mixed impact on the Global Pumped Storage Hydropower Market. On one hand, the pandemic caused delays in project timelines and reduced investment in new infrastructure due to economic uncertainties and supply chain disruptions. On the other hand, the increased focus on renewable energy and grid stability during the recovery phase highlighted the importance of energy storage solutions like pumped storage hydropower. Governments' commitment to sustainability and clean energy goals led to renewed interest in funding and developing pumped storage projects as part of broader recovery efforts. Overall, while short-term challenges were evident, the long-term outlook for the market remains positive as the transition to cleaner energy sources accelerates.

Conventional pumped storage systems remain the backbone of large-scale energy storage in the hydropower market. These systems operate by moving water between two reservoirs at different elevations, generating electricity during peak demand by releasing stored water through turbines. Recent developments include the commissioning of several new conventional pumped storage projects, such as the 1,600 MW storage facility in Oman, which aims to stabilize the national grid and support renewable energy integration. Driving factors for this sub-segment include the increasing demand for reliable energy sources to balance the intermittent nature of renewable energy, along with favorable government policies promoting clean energy investments. Additionally, technological advancements are improving the efficiency and capacity of conventional systems, making them a crucial component of future energy strategies.

Grid energy storage has emerged as a vital application within the pumped storage hydropower market, focusing on stabilizing electricity grids and managing supply and demand fluctuations. Recent projects, such as the 2,000 MW Goldisthal pumped storage facility in Germany, demonstrate the effectiveness of integrating pumped storage with renewable energy sources to ensure grid reliability. This sub-segment is driven by the growing need for energy storage solutions that can respond quickly to changes in electricity demand, especially as more renewable sources come online. The increasing frequency of extreme weather events and power outages has further highlighted the necessity for robust grid energy storage systems. As countries transition toward cleaner energy portfolios, investments in grid energy storage solutions are expected to increase, enhancing energy security and sustainability.

The Asia-Pacific region is poised for significant growth in the pumped storage hydropower market over the forecast period, driven by several critical factors. Rapid urbanization and industrialization in countries like China and India are leading to a surge in electricity demand, necessitating reliable energy storage solutions. Governments in the region are increasingly investing in renewable energy projects, and pumped storage hydropower is seen as an essential technology to balance the intermittent nature of solar and wind energy. Moreover, several countries are introducing favorable policies and financial incentives to promote the development of large-scale energy storage systems. The growing awareness of energy security and the need for grid stability further bolster investments in pumped storage infrastructure. As these trends continue, the Asia-Pacific region is expected to emerge as a key player in the global pumped storage hydropower market.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global Pumped Storage Hydropower Market is marked by a diverse range of players, including established energy companies, engineering firms, and technology providers that are vying for market share in this critical segment. Major companies are focusing on expanding their portfolios through new project developments, technological innovations, and strategic partnerships to enhance operational efficiency and reduce costs.

Key competitors in the market include

Recent Development

Q1. What are the driving factors for the Global Pumped Storage Hydropower Market?

The Global Pumped Storage Hydropower Market is primarily driven by the increasing demand for renewable energy sources and the need for energy storage solutions. As the share of intermittent renewable resources like solar and wind grows, pumped storage hydropower offers a reliable method for balancing supply and demand by storing excess energy and releasing it when needed. Additionally, the growing focus on grid stability and resilience, particularly with the integration of renewable energy, enhances the appeal of pumped storage facilities. Technological advancements that improve efficiency and reduce costs also contribute to market growth. Furthermore, supportive government policies and investments aimed at transitioning to cleaner energy systems are accelerating the development of pumped storage projects worldwide.

Q2. What are the restraining factors for the Global Pumped Storage Hydropower Market?

Despite its advantages, the Global Pumped Storage Hydropower Market faces several restraining factors. One of the main challenges is the high capital investment required for the construction and maintenance of pumped storage facilities, which can deter potential investors. Environmental concerns regarding the ecological impact of damming rivers and altering water bodies can also lead to regulatory hurdles and public opposition. Additionally, the long lead times associated with project development can delay returns on investment. Competition from alternative energy storage technologies, such as lithium-ion batteries, which are often more flexible and quicker to deploy, poses a challenge. Furthermore, the geographical limitations of suitable sites for pumped storage facilities can restrict market growth in certain regions.

Q3. Which segment is projected to hold the largest share in the Global Pumped Storage Hydropower Market?

The conventional pumped storage segment is projected to hold the largest share in the Global Pumped Storage Hydropower Market. This segment involves traditional methods of storing energy by pumping water to an elevated reservoir during periods of low demand and releasing it to generate electricity during peak demand. Conventional pumped storage systems are well-established and have been in use for decades, providing reliable and proven technology. Their ability to offer large-scale energy storage solutions makes them particularly valuable in balancing grid operations and supporting renewable energy integration. As energy storage requirements continue to grow, this segment is expected to maintain its dominance in the market.

Q4. Which region holds the largest share in the Global Pumped Storage Hydropower Market?

Asia-Pacific currently holds the largest share in the Global Pumped Storage Hydropower Market, driven by significant investments in renewable energy infrastructure and energy security. Countries like China and Japan are leading in pumped storage capacity, with extensive projects aimed at integrating renewable energy sources into their grids. China's ambitious plans for renewable energy expansion and grid stability further bolster the region's market position. Additionally, growing energy demands in developing countries in Asia-Pacific are pushing for more efficient energy storage solutions. While Europe and North America are also important markets, the rapid growth and investment in the Asia-Pacific region set it apart as the leader in pumped storage hydropower.

Q5. Which are the prominent players in the Global Pumped Storage Hydropower Market?

Prominent players in the Global Pumped Storage Hydropower Market include General Electric (GE), a key supplier of hydropower technology and services. Siemens is also notable for its innovations in hydropower solutions, including pumped storage systems. Voith Hydro specializes in providing hydropower plants and has extensive experience in pumped storage projects. Andritz Hydro is another significant player, offering a range of hydropower technologies. Alstom, now part of GE, has a strong presence in the pumped storage market. China Three Gorges Corporation and China Huaneng Group are major state-owned enterprises leading the way in pumped storage development in China. These companies are actively involved in expanding capacity and enhancing the efficiency of pumped storage hydropower solutions worldwide.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model