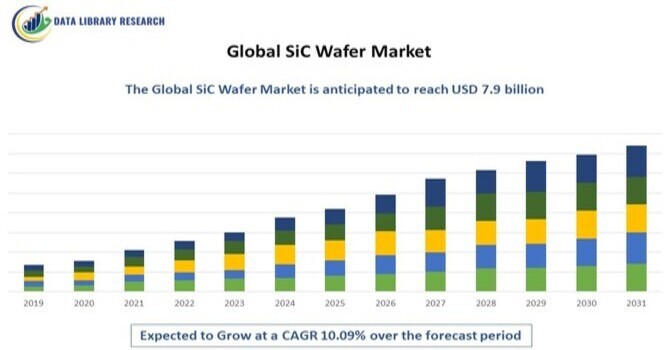

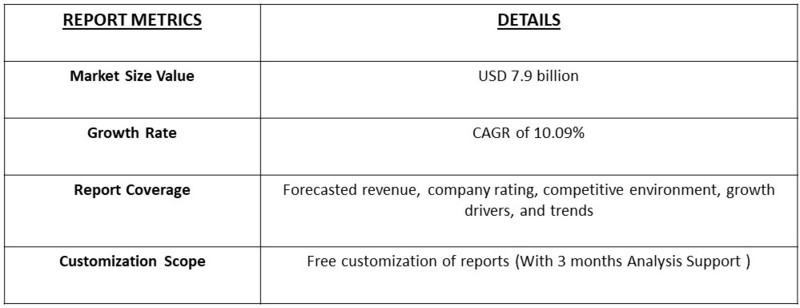

The global SiC Wafer market is expected to reach a value of 1.6 billion in 2023, growing from 1.2 billion in 2020, reaching to USD 7.9 billion in 2031 at a Compound Annual Growth Rate (CAGR) of 10.09%, from 2023-2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

The SiC (Silicon Carbide) wafer market involves the production and distribution of silicon carbide wafers used in various electronic applications, particularly in power electronics, semiconductor devices, and optoelectronics. SiC wafers are favored for their superior thermal conductivity, high breakdown voltage, and ability to operate at elevated temperatures compared to traditional silicon wafers. The market is driven by the increasing demand for energy-efficient devices, advancements in electric vehicles, and the growing adoption of renewable energy technologies. Key applications include power inverters, LED lighting, and high-frequency devices. As industries shift towards more efficient and sustainable solutions, the SiC wafer market is poised for substantial growth in the coming years.

The SiC wafer market is primarily driven by the increasing demand for energy-efficient electronic devices across various sectors, including automotive, telecommunications, and renewable energy. The growing adoption of electric vehicles (EVs) necessitates high-performance power electronics, where SiC wafers offer significant advantages in terms of efficiency and thermal management. Additionally, the push for renewable energy solutions, such as solar inverters and wind turbine converters, is further fueling demand for SiC-based components. Technological advancements in manufacturing processes are also reducing costs and improving the availability of SiC wafers. Moreover, regulatory frameworks promoting energy efficiency and sustainability are enhancing market growth prospects.

The SiC Wafer market is witnessing a surge in demand, driven by the increasing adoption of high-power and high-frequency electronic devices. Key trends include the growing use of SiC-based solutions in power electronics, electric vehicles, and aerospace and defense industries. Additionally, advancements in manufacturing technology and the development of larger-diameter wafers are expected to improve yield and reduce costs. Furthermore, the increasing focus on sustainability and energy efficiency is driving demand for SiC-based solutions that can reduce energy consumption and emissions. As a result, we expect to see continued growth and innovation in the SiC Wafer market.

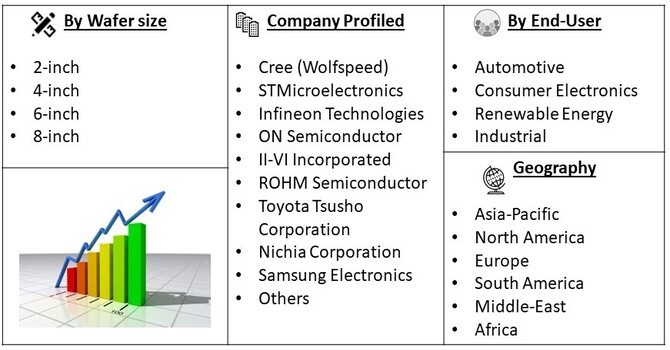

Market Segmentation: The Global SiC Wafer Market is segmented Wafer size (2-inch, 4-inch, 6-inch, 8-inch) End-User Industry (Automotive, Consumer Electronics, Renewable Energy, Industrial) and geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report offers the market size and forecasts for revenue (USD million) for all the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

Growing demand for electric vehicles:

The growing demand for electric vehicles is driving the need for high-performance power electronics, which are critical components of electric vehicle systems. SiC wafers are ideal for these applications due to their high thermal conductivity, high breakdown voltage, and high-frequency switching capabilities. As a result, we expect to see significant growth in the demand for SiC wafers in the electric vehicle industry. In fact, according to a recent report by BloombergNEF, the global electric vehicle market is expected to reach 140 million units by 2030, up from just 2 million units in 2020. This growth will drive demand for SiC wafers and other power electronics components.

Increasing adoption of renewable energy:

The increasing adoption of renewable energy sources, such as solar and wind power, is driving the need for high-efficiency power electronics that can convert and control the flow of energy. SiC wafers are well-suited for these applications due to their high thermal conductivity, high breakdown voltage, and high-frequency switching capabilities. As a result, we expect to see significant growth in the demand for SiC wafers in the renewable energy industry. In fact, according to the International Energy Agency (IEA), the global renewable energy market is expected to reach 30% of the global energy mix by 2050, up from just 20% in 2020. This growth will drive demand for SiC wafers and other power electronics components.

Market Restraints:

Despite the growing demand for SiC wafers, high production costs and limited supply remain significant restraints on the market. The production process for SiC wafers is complex and energy-intensive, which drives up costs. Additionally, the limited availability of high-quality SiC materials and the need for specialized equipment and expertise further constrain supply. As a result, we expect to see continued price volatility and supply chain disruptions in the SiC wafer market. Furthermore, the high costs of production and limited supply are likely to slow the adoption of SiC wafers in certain applications, such as electric vehicles and renewable energy systems.

The COVID-19 pandemic significantly impacted the global SiC wafer market, leading to both challenges and opportunities. Initially, the crisis caused disruptions in supply chains, manufacturing operations, and project timelines, resulting in delays for various semiconductor applications. However, the pandemic also accelerated the digital transformation across industries, increasing demand for high-performance electronics, including power management solutions and electric vehicles. As companies adapted to remote work and increased reliance on digital infrastructure, the need for energy-efficient devices became more pronounced, driving interest in SiC technology. Moreover, government initiatives aimed at promoting green technologies and sustainability post-pandemic are expected to boost investments in the SiC wafer market. Overall, while the pandemic presented obstacles, it also highlighted the importance of SiC wafers in enabling a more sustainable and efficient future.

Segmental Analysis:

Power Electronics Segment is Expected to Witness Significant Growth Over the Forecast Period:

The power electronics sub-segment is a critical driver of the SiC wafer market, primarily due to the increasing demand for efficient energy conversion systems in various applications. Industries are increasingly turning to SiC technology for power inverters, converters, and chargers, as it allows for smaller, lighter, and more efficient designs compared to traditional silicon devices. Recent developments, such as the use of SiC in the Tesla Model 3’s inverter system, highlight the technology's capability to enhance performance and reliability in electric vehicles. Additionally, the growing focus on renewable energy sources, like solar and wind, requires advanced power electronics for energy management, further boosting the demand for SiC wafers. The drive for energy efficiency and reduced operational costs continues to propel investments in power electronics, positioning this sub-segment as a significant growth area in the SiC wafer market.

N-Type SiC Wafers Segment is Expected to Witness Significant Growth Over the Forecast Period

N-type SiC wafers are gaining prominence due to their superior electron mobility and efficiency in high-performance applications. This sub-segment is particularly relevant for industries focusing on advanced semiconductor devices, such as those used in electric vehicles and renewable energy systems. Companies like ON Semiconductor are investing heavily in the development of N-type SiC wafers to meet the growing demands for high-voltage and high-temperature applications. For instance, the adoption of N-type wafers in power inverters for solar energy systems improves energy conversion efficiency, addressing the need for more sustainable solutions. The increasing trend toward electric mobility and energy efficiency is driving the expansion of this sub-segment, making N-type SiC wafers a key area for innovation and investment in the semiconductor landscape.

Asia Pacific Region is Expected to Witness Significant Growth Over the Forecast Period

The Asia-Pacific region is poised for significant growth in the SiC wafer market over the forecast period, driven by several key factors. Rapid industrialization and urbanization in countries like China, India, and Japan are leading to increased demand for energy-efficient electronics, particularly in the automotive and consumer electronics sectors. The region's strong commitment to renewable energy initiatives, including solar and wind power, further fuels the adoption of SiC technology for improved energy conversion and efficiency. For example, the Chinese government has set ambitious targets for electric vehicle production, which is expected to drive the integration of SiC wafers in power electronics. Additionally, advancements in semiconductor manufacturing capabilities and investments in R&D are enhancing the competitiveness of local players. As the region continues to focus on sustainable growth and reducing carbon emissions, the SiC wafer market is set to flourish, making Asia-Pacific a critical hub for innovation and development in this field.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the global SiC wafer market is characterized by a mix of established semiconductor companies and emerging players focused on advancing SiC technology.

Key competitors include:

Recent Development:

1) Cree (Wolfspeed) - 2023: Cree announced the expansion of its silicon carbide wafer production facility in Durham, North Carolina, to meet the surging demand for SiC-based power devices. This $1 billion investment aims to increase manufacturing capacity by over 30%, enabling the production of larger wafers and higher-quality substrates. The expansion is expected to support various applications, including electric vehicles, renewable energy systems, and 5G telecommunications. By scaling up its operations, Cree is positioning itself to capture a significant share of the growing SiC market, particularly as industries shift toward more efficient and sustainable solutions.

2) STMicroelectronics - 2024: STMicroelectronics unveiled a new line of 8-inch SiC wafers aimed at enhancing the performance of power electronic devices. The company’s latest offerings focus on improving energy efficiency and thermal performance in applications such as electric vehicle chargers and industrial power supplies. This development is part of ST's strategy to meet the increasing demand for advanced power management solutions. Additionally, the company has committed to investing in research and development to further enhance SiC technology, reinforcing its position as a key player in the SiC wafer market as it aligns with global trends toward electrification and sustainability.

Q1. What are the driving factors for the Global SiC Wafer Market?

The Global SiC Wafer Market is primarily driven by the increasing demand for high-performance semiconductors in various applications, particularly in electric vehicles (EVs), power electronics, and renewable energy systems. SiC wafers are favored for their superior thermal conductivity, high electric field strength, and efficiency in power conversion, making them ideal for applications that require reliability and durability under extreme conditions. The growing trend towards energy-efficient solutions and the rising need for faster charging infrastructure for EVs further accelerate the market. Additionally, government initiatives promoting green technologies and renewable energy sources contribute to the expanded adoption of SiC wafers in power management applications.

Q2. What are the restraining factors for the Global SiC Wafer Market?

Despite its growth potential, the Global SiC Wafer Market faces several restraining factors. The high production costs associated with SiC wafers can be a significant barrier, especially for small and medium-sized enterprises looking to enter the market. The complex manufacturing processes and the need for specialized equipment also add to these costs. Furthermore, the availability of alternative materials, such as silicon and gallium nitride (GaN), may pose competitive challenges. The market may also be hindered by limited supplier networks and potential technological hurdles in scaling production to meet increasing demand.

Q3. Which segment is projected to hold the largest share in the Global SiC Wafer Market?

The 150 mm SiC wafer segment is projected to hold the largest share in the Global SiC Wafer Market. This size is favored for a wide range of applications, particularly in power electronics and automotive sectors, due to its balance of cost and performance. The growing adoption of 150 mm wafers in manufacturing processes is driven by the demand for higher efficiency and reliability in devices such as power converters, inverters, and chargers. As more companies invest in scaling up their production capabilities, the 150 mm segment is expected to continue dominating the market.

Q4. Which region holds the largest share in the Global SiC Wafer Market?

North America holds the largest share in the Global SiC Wafer Market, primarily due to its strong automotive and semiconductor industries. The region is home to key players and leading technology companies actively investing in SiC wafer production and R&D, particularly in the context of electric vehicles and energy-efficient solutions. Additionally, supportive government policies and initiatives aimed at promoting green technologies and sustainable energy further bolster market growth. As the demand for EVs and renewable energy applications continues to rise, North America's dominance in the SiC wafer market is expected to persist.

Q5. Which are the prominent players in the Global SiC Wafer Market?

Prominent players in the Global SiC Wafer Market include Wolfspeed, Inc., STMicroelectronics, Infineon Technologies AG, Nexperia, and SICC. These companies are recognized for their innovation and extensive experience in the semiconductor industry, focusing on the development and production of high-quality SiC wafers. They invest heavily in research and development to enhance their manufacturing processes and product offerings. Additionally, strategic partnerships and collaborations with automotive and renewable energy companies are common practices among these players to expand their market reach and solidify their positions in the growing SiC wafer landscape.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model