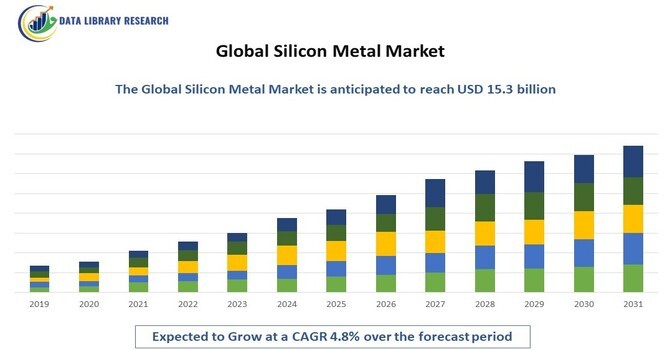

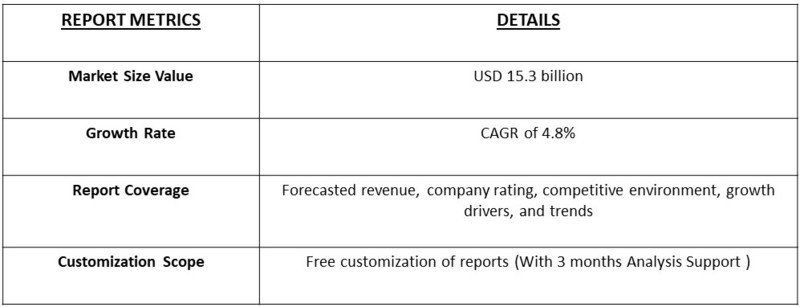

The global silicon metal market is anticipated to reach a market value of USD 10.7 billion in 2023 and is projected to grow to USD 15.3 billion by 2031, with a compound annual growth rate (CAGR) of 4.8% from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

This growth is driven by increasing demand in various industries, particularly in the production of aluminum, solar cells, and silicones, alongside advancements in production technologies and rising awareness of silicon's versatile applications.

Silicon metal is a key raw material primarily used in the manufacturing of aluminum alloys, solar panels, and silicones. It is produced through the reduction of silica in a furnace, yielding a high-purity product. Silicon's unique properties, such as high melting point, thermal conductivity, and corrosion resistance, make it an essential component in numerous applications, from construction materials to electronics and renewable energy.

The global silicon metal market is propelled by several key factors, including the growing demand for lightweight and energy-efficient materials in the automotive and aerospace sectors, increased investments in renewable energy sources, particularly solar power, and the rising usage of silicones in construction and consumer goods. Moreover, the expansion of electric vehicle (EV) production and advancements in battery technology further amplify the demand for silicon metal, as it is increasingly used in battery anodes. As a result, the silicon metal market is expected to witness robust growth over the coming years.

The global silicon metal market is characterized by several notable trends shaping its future. One prominent trend is the rising demand for sustainable and environmentally friendly materials, driving manufacturers to explore innovative production methods and alternative raw materials. Additionally, advancements in silicon production technologies, including cleaner and more efficient processes, are gaining traction.

There is also an increasing focus on the integration of silicon metal in energy storage solutions, particularly in the burgeoning electric vehicle market, where silicon anodes are being explored to enhance battery performance. Moreover, as the construction industry continues to evolve, the demand for high-performance silicones in construction applications is rising, reflecting a shift towards modern building materials. Furthermore, the growing interest in renewable energy technologies, particularly solar photovoltaic systems, is expected to drive silicon metal consumption in the coming years, positioning the market for continued expansion.

Market Segmentation

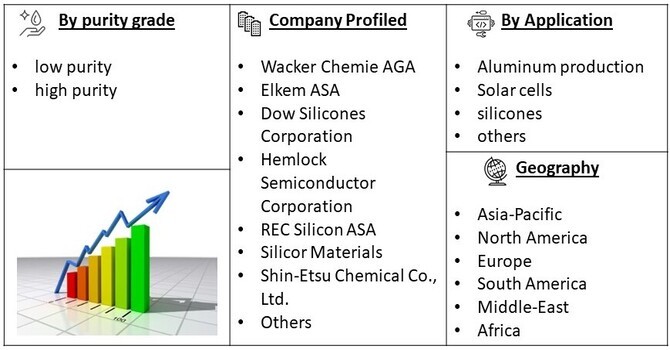

The global silicon metal market is segmented by application (aluminum production, solar cells, silicones, and others), by purity grade (low purity, high purity), and by geography (North America, Europe, Asia-Pacific, South America, and the Middle East and Africa). The report provides market size and forecasts for revenue (USD million) for all these segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The rising demand for aluminum, driven by its lightweight and corrosion-resistant properties, is a significant driver for the silicon metal market. Silicon metal is a key alloying agent in aluminum production, improving the strength and durability of aluminum products used in transportation, construction, and packaging industries. As the global aluminum market expands, particularly in the automotive and aerospace sectors, the demand for silicon metal is expected to increase correspondingly.

The global push towards renewable energy sources, particularly solar power, is fueling the demand for silicon metal. Silicon is the primary material used in the production of solar photovoltaic (PV) cells. As governments and organizations worldwide invest in solar energy to reduce carbon emissions and promote sustainability, the consumption of silicon metal is set to rise. This trend is reinforced by technological advancements that enhance the efficiency and affordability of solar panels, further solidifying silicon’s position in the renewable energy landscape.

Ongoing innovations in silicon production technologies are enhancing the efficiency and sustainability of silicon metal manufacturing. The development of cleaner production processes, such as the use of renewable energy in silicon production, is gaining momentum. These advancements not only reduce the environmental impact of silicon production but also improve profit margins for manufacturers, making silicon metal an increasingly attractive material for various applications.

Market Restraints

The silicon metal market faces challenges due to the volatility of raw material prices, particularly silica. Price fluctuations can impact the profitability of silicon producers and may lead to increased costs for end-users. Such unpredictability in pricing can deter investments in the silicon sector and hinder market growth. Environmental Concerns

The production of silicon metal involves significant energy consumption and carbon emissions, raising environmental concerns among regulators and consumers. As sustainability becomes a critical focus for industries worldwide, producers may face pressure to adopt greener practices and reduce their carbon footprint. Failure to comply with environmental regulations can lead to operational challenges and impact market growth.

The COVID-19 pandemic had a notable impact on the global silicon metal market, disrupting supply chains and production capabilities. Lockdowns led to reduced manufacturing output, particularly in sectors like automotive and electronics, which are key consumers of silicon. Consequently, demand fluctuated, causing price volatility. However, as economies began to recover, the push for renewable energy technologies and electric vehicles spurred renewed interest in silicon for photovoltaic cells and battery applications. Additionally, the pandemic accelerated trends toward digitization and technological advancement, further driving demand for silicon in electronics. Overall, while the market faced short-term challenges, the long-term outlook remains positive, supported by increasing applications in sustainable technologies.

Segmental Analysis

The high purity silicon metal segment is anticipated to experience substantial growth over the forecast period. This segment is primarily driven by the increasing demand for high-performance materials in the electronics and solar industries. High purity silicon is essential for producing high-efficiency solar cells and advanced semiconductor devices, which are crucial for the growing renewable energy and electronics sectors. Additionally, advancements in purification technologies and the increasing trend towards miniaturization in electronics further bolster the demand for high purity silicon metal.

The aluminum production segment is projected to hold the largest share of the global silicon metal market. As the demand for lightweight and durable aluminum products continues to rise in various industries, particularly in automotive and construction, silicon metal’s role as an alloying agent becomes increasingly important. The ongoing growth of the aluminum market, fueled by the shift towards energy-efficient and sustainable materials, ensures a steady demand for silicon metal in aluminum manufacturing.

The Asia-Pacific region is expected to dominate the global silicon metal market, driven by rapid industrialization, rising demand for aluminum, and significant investments in renewable energy projects, particularly solar power. Countries such as China and India are major contributors to the regional market, with their expanding manufacturing sectors and growing population driving demand for silicon metal in various applications. Furthermore, the increasing focus on sustainable energy solutions in these countries is likely to bolster the demand for silicon in solar panel production.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the global silicon metal market features a mix of established players and emerging companies striving for market share through innovation, sustainability initiatives, and enhanced product offerings.

Key industry leaders include:

Recent Developments

Q1. What are the driving factors for the Global Silicon Metal Market?

The global silicon metal market is driven by the increasing demand from the aluminum industry, growth in the renewable energy sector, particularly solar power, and advancements in production technologies that enhance efficiency and sustainability.

Q2. What are the restraining factors for the Global Silicon Metal Market?

The market faces challenges such as fluctuating raw material prices, environmental concerns related to production emissions, and competition from alternative materials and technologies.

Q3. Which segment is projected to hold the largest share in the Global Silicon Metal Market?

The aluminum production segment is projected to hold the largest share, driven by the growing demand for lightweight and durable aluminum products across various industries.

Q4. Which region holds the largest share of the Global Silicon Metal Market?

The Asia-Pacific region is expected to hold the largest share, fueled by rapid industrialization, investments in renewable energy, and significant demand for aluminum products.

Q5. Which are the prominent players in the Global Silicon Metal Market?

Key players include Wacker Chemie AG, Elkem ASA, Dow Silicones Corporation, Hemlock Semiconductor Corporation, REC Silicon ASA, Silicor Materials, Shin-Etsu Chemical Co., Ltd., Norsk Hydro ASA, China National BlueStar (Group) Co., Ltd., Mitsubishi Materials Corporation, Qinghai Yangguang Silicon Co., Ltd., Daqo New Energy Corp., GCL-Poly Energy Holdings Limited, SunEdison, Inc., and Wuxi Shangji Automation Co., Ltd.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model