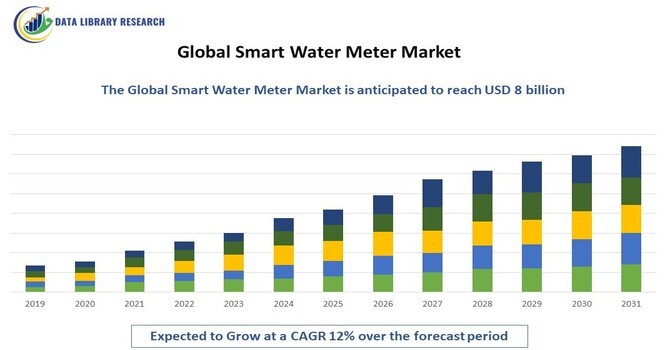

The global smart water meter market was valued at approximately $3 billion in 2023 and is projected to reach around $8 billion by 2031, reflecting a compound annual growth rate (CAGR) of about 12% from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

Smart water meters are integral components of advanced metering infrastructure (AMI), enabling utilities and consumers to monitor water usage in real time, enhance billing accuracy, and improve resource management. The rising concerns over water scarcity and the need for efficient water management systems are driving the demand for smart water meters globally. Increasing adoption of Internet of Things (IoT) technologies and smart city initiatives in urban areas further bolster market growth. As utilities and municipalities strive for sustainability, the integration of smart water meters facilitates better water conservation, leakage detection, and operational efficiency, making them essential for modern water management strategies.

Moreover, smart water meters offer significant benefits beyond just consumption tracking and billing accuracy. They empower consumers with detailed insights into their water usage patterns, enabling them to identify opportunities for conservation and cost savings. For utilities, the data collected from smart meters aids in predictive maintenance, allowing for timely interventions that reduce the risk of leaks and system failures. Additionally, these devices can integrate with smart home systems, providing users with real-time alerts and analytics through mobile applications. This synergy between technology and consumer engagement not only promotes responsible water usage but also enhances the overall resilience of water infrastructure, ensuring a sustainable supply for future generations. As cities around the world grapple with the challenges of urbanization and climate change, the role of smart water meters in fostering efficient water management practices becomes increasingly vital.

Key trends influencing the smart water meter market include the increasing adoption of IoT-based solutions for remote monitoring and management of water resources. Utilities are investing in advanced analytics and data-driven decision-making to optimize water distribution and reduce waste. Furthermore, the shift toward smart city infrastructure is driving the implementation of smart water meters, as municipalities seek to enhance their operational efficiency and sustainability. The growing awareness of water conservation and environmental impact is also prompting consumers to adopt smart water metering solutions, leading to a more informed and proactive approach to water usage.

Additionally, advancements in communication technologies, such as 5G and LPWAN (Low Power Wide Area Network), are significantly enhancing the capabilities of smart water meters. These technologies enable faster and more reliable data transmission, facilitating real-time monitoring and immediate response to water management issues. The integration of machine learning and artificial intelligence into smart water metering systems is further optimizing resource management by predicting demand patterns and identifying potential leaks or inefficiencies before they escalate. As regulatory bodies increasingly emphasize sustainability and efficient resource management, utilities are motivated to adopt smart water metering solutions that not only comply with standards but also contribute to broader environmental goals. This convergence of technology, regulatory support, and consumer awareness is propelling the smart water meter market toward a more sustainable and efficient future.

Market Segmentation

The global smart water meter market is segmented by type (ultrasonic, mechanical, electromagnetic, and others), by application (residential, commercial, and industrial), and by geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). This segmentation provides valuable insights into market dynamics, enabling stakeholders to identify growth opportunities in specific areas.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The increasing need for efficient water management solutions is a key factor driving the smart water meter market. As water scarcity becomes a pressing global issue, utilities and municipalities are seeking advanced technologies to optimize water usage and reduce wastage. Smart water meters provide real-time data on water consumption, enabling users to identify trends, detect leaks, and implement conservation measures effectively. This heightened focus on sustainable water management is encouraging investments in smart metering technologies, facilitating growth in the market.

In addition, the push for regulatory compliance regarding water conservation is further fueling the adoption of smart water meters. Governments around the world are implementing stricter policies aimed at reducing water waste and promoting sustainable resource management practices. By utilizing smart water metering systems, utilities can ensure compliance with these regulations while providing transparent reporting on water usage and conservation efforts. Furthermore, the rising prevalence of digital technology among consumers is driving demand for interactive water management solutions, allowing users to track their consumption through user-friendly apps and platforms. This shift not only empowers consumers to take control of their water usage but also fosters a culture of accountability and stewardship over precious water resources. As a result, the smart water meter market is positioned for substantial growth as it aligns with global sustainability goals and the increasing demand for innovative water management solutions.

Rapid advancements in smart metering technology are further propelling the smart water meter market. Innovations in IoT, cloud computing, and data analytics enable utilities to gather and analyze vast amounts of data related to water consumption patterns. This data-driven approach facilitates better decision-making, allowing utilities to improve operational efficiency, optimize resource allocation, and enhance customer service. The integration of mobile applications and user-friendly interfaces also empowers consumers to monitor their water usage, leading to more conscious consumption and cost savings.

Moreover, the increasing focus on customer engagement and education is reshaping the landscape of the smart water meter market. Utilities are leveraging smart metering systems not only to track consumption but also to provide personalized insights and recommendations to consumers. By offering tailored alerts about usage patterns and potential savings, utilities can encourage proactive water management among customers. This enhanced communication fosters stronger relationships between utilities and consumers, driving greater transparency and trust. Additionally, as more households adopt smart water meters, communities can benefit from aggregated data that highlights trends in water usage, empowering municipalities to implement targeted conservation initiatives. This holistic approach to water management, driven by technology and consumer participation, is expected to significantly enhance water sustainability efforts and further stimulate the growth of the smart water meter market.

Market Restraints

High installation and maintenance costs associated with smart water meters pose a significant restraint on market growth. While the long-term benefits of smart metering solutions are evident, the initial capital investment required for deployment can be a barrier for smaller utilities and municipalities, particularly in developing regions. Additionally, concerns regarding data privacy and security related to smart water metering systems may hinder adoption, as consumers and utilities seek assurances regarding the protection of their sensitive information.

Furthermore, the lack of standardized regulations and interoperability among different smart water meter technologies can complicate adoption and integration efforts. Utilities often face challenges in selecting compatible systems that can seamlessly work together, leading to potential inefficiencies and increased operational costs. This fragmentation in the market can discourage smaller entities from investing in smart water metering solutions, as they may fear being locked into proprietary systems that limit future upgrades or expansions. Moreover, the need for ongoing training and support for utility personnel to effectively manage and analyze the data generated by these systems adds another layer of complexity and cost. Addressing these challenges through collaborative industry standards and robust support frameworks will be essential for unlocking the full potential of the smart water meter market and promoting widespread adoption across various regions.

The COVID-19 pandemic had a mixed impact on the smart water meter market. While the initial disruptions in supply chains and project timelines delayed the deployment of smart metering solutions, the pandemic also highlighted the need for remote monitoring and digital solutions. Utilities recognized the importance of adopting advanced technologies to enhance operational resilience, leading to an increased focus on smart water meter implementation. As the market recovers, the emphasis on automation and data-driven management is expected to drive future growth in the sector.

Additionally, the pandemic accelerated the shift towards digital transformation in the water sector, prompting utilities to prioritize investments in smart technologies that facilitate real-time monitoring and remote access. With many organizations operating under social distancing protocols, the demand for solutions that minimize the need for on-site interactions became paramount. As a result, smart water meters, with their capabilities for remote data collection and management, gained traction as utilities sought to enhance service delivery while ensuring the safety of their personnel and customers. This growing recognition of the value of smart water metering solutions not only helped mitigate the immediate challenges posed by the pandemic but also set the stage for a long-term shift towards more resilient and efficient water management practices. Moving forward, the integration of smart technologies will likely remain a key strategy for utilities aiming to adapt to evolving consumer needs and environmental challenges.

Segmental Analysis

The ultrasonic water meters segment is poised to hold a significant share of the smart water meter market, primarily due to their accuracy and reliability. Unlike mechanical meters, ultrasonic water meters use sound waves to measure flow, providing highly precise readings and reducing the risk of inaccuracies caused by wear and tear. This technology is particularly advantageous for utilities aiming to enhance billing accuracy and minimize revenue loss due to unaccounted water usage. Moreover, the ability of ultrasonic meters to support advanced functionalities, such as remote monitoring and real-time data transmission, further strengthens their position in the market.

In addition to their accuracy and reliability, ultrasonic water meters offer several operational benefits that make them increasingly appealing to utilities. Their non-intrusive design eliminates moving parts, significantly reducing maintenance requirements and extending the lifespan of the meters. This durability is crucial for utilities seeking to optimize their operational efficiency and reduce long-term costs associated with meter replacement and repairs. Furthermore, the integration of ultrasonic water meters with IoT platforms enhances their capabilities, allowing for advanced data analytics and predictive maintenance. This technological synergy enables utilities to proactively manage their water distribution networks, identify potential issues before they escalate, and ensure better resource allocation. As water management becomes more data-driven, the adoption of ultrasonic water meters is expected to rise, solidifying their prominent role in the smart water meter market.

The residential application segment is anticipated to dominate the smart water meter market, as homeowners increasingly seek efficient water management solutions. The rising awareness of water conservation and the desire to lower utility bills are driving consumers to adopt smart water meters that provide real-time insights into water usage. Additionally, utilities are incentivizing the installation of smart meters in residential areas to enhance billing accuracy and reduce operational costs. The integration of mobile applications enables consumers to track their water consumption, encouraging more responsible usage patterns and contributing to overall market growth.

Furthermore, the growing trend of home automation and the increasing adoption of smart home technologies are also propelling the residential application segment of the smart water meter market. As more households invest in interconnected devices, the ability to integrate smart water meters with existing home automation systems allows consumers to monitor and control their water usage seamlessly alongside other utilities. This synergy not only enhances user experience but also fosters a comprehensive approach to resource management within the home. Additionally, as cities and municipalities implement smart city initiatives, residents benefit from improved infrastructure, including better leak detection and response services. As a result, the combination of consumer awareness, technological advancements, and utility incentives positions the residential segment for robust growth in the smart water meter market.

Regional Analysis

North America is poised to maintain a dominant position in the global smart water meter market, largely due to its advanced infrastructure and regulatory support for water conservation initiatives. The region has seen significant investments in smart metering technologies, with many utilities actively upgrading their systems to incorporate advanced solutions. Additionally, the increasing focus on sustainable water management practices, coupled with government incentives for adopting smart technologies, is driving the growth of the smart water meter market in North America.

Moreover, the presence of established technology providers and a robust research and development ecosystem in North America further enhances the region's leadership in the smart water meter market. Companies are continually innovating to develop cutting-edge solutions that address the specific needs of utilities and consumers alike, such as enhanced data analytics, user-friendly interfaces, and improved connectivity options. Furthermore, rising public awareness about water scarcity issues and the importance of resource conservation has prompted municipalities to prioritize smart water metering initiatives. As urbanization continues to accelerate, the demand for efficient water management systems in North America is expected to grow, positioning the region as a key player in the ongoing evolution of the smart water meter market.

To Learn More About This Report - Request a Free Sample Copy

The smart water meter market features several prominent players, including Itron, Sensus (Xylem), Kamstrup, and Badger Meter. These companies are focused on innovation, expanding their product portfolios, and forming strategic partnerships to enhance market presence. Emerging players are also entering the market, fostering competition and driving advancements in smart water metering technologies. Research and development initiatives aimed at improving efficiency and sustainability are central to the competitive strategies of leading firms.

Here are ten key players in the smart water meter market

These companies play significant roles in the development and implementation of smart water metering technologies, contributing to the overall growth of the market.

Recent Developments

Q1. What are the driving factors for the Global Smart Water Meter Market?

The global smart water meter market is primarily driven by the increasing demand for efficient water management solutions, technological advancements in IoT and data analytics, and a growing emphasis on sustainability and water conservation. The integration of Internet of Things (IoT) technologies and advancements in data analytics are enhancing the functionality and efficiency of smart water meters. These innovations enable utilities to monitor consumption patterns remotely, analyze data for better decision-making, and optimize resource allocation.

Q2. What are the restraining factors for the Global Smart Water Meter Market?

Key challenges facing the smart water meter market include high installation and maintenance costs, regulatory hurdles, and concerns regarding data privacy and security. Varying regulations across different regions can complicate the implementation of smart water metering solutions. Utilities may face challenges in complying with local laws and standards, which can delay project timelines.

Q3. Which segment is projected to hold the largest share in the Global Smart Water Meter Market?

The ultrasonic water meters segment is projected to hold the largest share of the smart water meter market due to their accuracy, reliability, and support for advanced functionalities. Ultrasonic water meters provide highly precise measurements by utilizing sound waves to gauge flow, which minimizes inaccuracies associated with mechanical meters. This is particularly important for utilities looking to enhance billing accuracy and reduce revenue loss from unaccounted water usage.

Q4. Which region holds the largest share of the Global Smart Water Meter Market?

North America is expected to hold the largest share of the global smart water meter market, driven by advanced infrastructure and strong regulatory support for water conservation initiatives. North America boasts a well-developed infrastructure, enabling the seamless integration of smart metering technologies into existing water distribution systems. Utilities in North America are actively investing in smart metering technologies to upgrade their systems, enhance operational efficiency, and improve customer service.

Q5. Who are the prominent players in the Global Smart Water Meter Market?

Prominent players in the smart water meter market include Itron, Sensus (Xylem), Kamstrup, and Badger Meter, all recognized for their commitment to innovation and sustainability in water management solutions. These companies are leading the charge in developing and implementing smart water metering technologies, significantly contributing to the overall growth and evolution of the market. Their commitment to innovation and sustainability positions them favorably as demand for smart water solutions continues to rise globally.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model