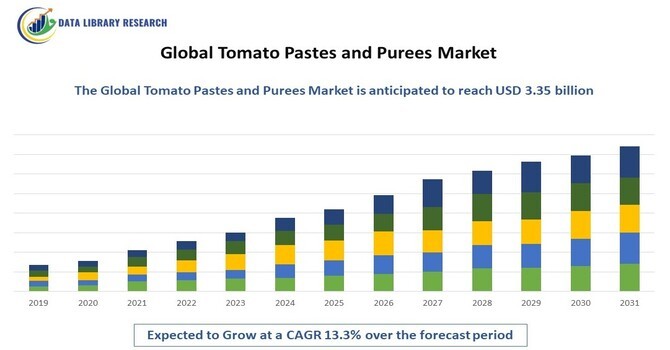

The Global Tomato Pastes and Purees Market is expected to reach a market value of approximately 1.43 billion in 2023, which is projected to reach around 3.35 billion by 2031, representing a CAGR of over 13.3% from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

Tomato pastes and purees are concentrated forms of tomatoes that have been cooked and blended to create a smooth, thick paste or puree. They are often used as a base for sauces, soups, and other recipes, and can be found in a variety of flavors, including plain, garlic, and herb-infused. Tomato pastes and purees are a popular ingredient in many cuisines, including Italian, Mexican, and Indian cooking.

The growth of the Global Tomato Pastes and Purees Market is driven by the increasing demand for convenient and shelf-stable food products, particularly among busy consumers who are seeking easy and healthy meal options. Additionally, the market is driven by the growing popularity of international cuisine, particularly in Asia and Latin America, where tomato-based sauces are a staple ingredient.

Market Segmentation

The Global Tomato Pastes and Purees Market is Segmented by Type (Tomato Paste, Tomato Puree, Tomato Sauce, Tomato Coulis and others (including tomato concentrate and tomato juice)), Application (Food Processing, Food Service, Retail, Institutional, and Other (including catering and food manufacturing)) and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report offers the market size and forecasts for revenue (USD million) for all the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

The Global Tomato Pastes and Purees Market is witnessing several trends, including the increasing demand for organic and natural products, the growing popularity of international cuisine, and the rising use of tomato pastes and purees as a base for sauces, soups, and other recipes. Additionally, the market is seeing a shift towards online sales, with many consumers opting for the convenience of purchasing tomato pastes and purees online. Furthermore, the market is also witnessing a trend towards sustainability, with many manufacturers focusing on reducing their environmental impact through eco-friendly packaging and production methods.

Market Drivers

The growing trend toward convenience foods significantly drives the Global Tomato Pastes and Purees Market. As lifestyles become busier, consumers increasingly seek quick and easy meal solutions, leading to a higher consumption of processed food products. Tomato pastes and purees serve as essential ingredients in a variety of dishes, from sauces and soups to ready-to-eat meals, making them a staple in many kitchens. This demand is particularly pronounced in urban areas, where time constraints often limit cooking time. Additionally, the expansion of the food service industry, including restaurants and fast-casual dining, further boosts the need for tomato-based products. With manufacturers continuously innovating packaging and product offerings to enhance convenience—such as single-serving pouches and ready-to-use options—the market is poised for sustained growth as consumers prioritize both quality and ease of use.

Growing health consciousness among consumers is another significant driver for the Global Tomato Pastes and Purees Market. As people become more aware of the health benefits associated with tomatoes, such as their rich antioxidant content and potential to reduce the risk of chronic diseases, there is an increasing inclination to incorporate tomato-based products into daily diets. Tomato pastes and purees offer a concentrated source of nutrients, including vitamins A and C, and lycopene, which has been linked to various health benefits. This shift toward healthier eating is reflected in the rising demand for organic and natural tomato products, which cater to consumers seeking minimally processed foods without artificial additives. Furthermore, the popularity of plant-based diets and the emphasis on fresh, wholesome ingredients further enhance the appeal of tomato pastes and purees as versatile components in both cooking and meal preparation. As a result, producers are focusing on quality, sustainability, and health-related marketing strategies to align with this growing consumer trend.

Market Restraints

One significant restraint affecting the Global Tomato Pastes and Purees Market is the price volatility of raw materials, particularly fresh tomatoes. Fluctuations in tomato prices can be attributed to various factors, including weather conditions, pest infestations, and changes in agricultural practices. For instance, adverse weather events such as droughts or floods can lead to reduced crop yields, driving up prices and impacting the overall cost of production. This unpredictability can create challenges for manufacturers in maintaining profit margins and pricing stability, making it difficult to offer competitive prices in the market. Additionally, higher raw material costs can lead to increased retail prices for consumers, potentially diminishing demand for tomato pastes and purees, especially among budget-conscious shoppers. Furthermore, reliance on a limited number of suppliers can exacerbate this issue, creating supply chain vulnerabilities. As a result, companies in the market need to develop strategies to mitigate these risks, such as diversifying sourcing options or investing in alternative supply chain models.

The COVID-19 pandemic had a notable impact on the Global Tomato Pastes and Purees Market, initially causing disruptions in supply chains and production as manufacturers faced lockdowns and labor shortages. This led to temporary shortages of products in retail outlets and increased prices due to supply constraints. However, the pandemic also spurred a significant shift in consumer behavior, with more people cooking at home and seeking convenient, shelf-stable ingredients, which bolstered demand for tomato sauces and purees. The rise of online grocery shopping further facilitated access to these products, allowing consumers to stock up on essentials. As restaurants and food service establishments adapted to new health regulations, many turned to tomato products for takeout and delivery options, sustaining demand in the food service sector. Overall, while the pandemic presented challenges, it also accelerated trends toward home cooking and online shopping, contributing to a gradual recovery and growth in the tomato pastes and purees market.

Segmental Analysis

The tomato puree segment is anticipated to experience significant growth over the forecast period, driven by its versatility and increasing applications in various culinary contexts. Tomato puree serves as a foundational ingredient in a wide range of dishes, including sauces, soups, and stews, making it a staple in both home kitchens and commercial food establishments. As consumers seek convenient cooking solutions, the demand for ready-to-use tomato puree continues to rise. Additionally, the growing trend of home cooking and meal preparation, spurred by the recent global focus on healthier eating habits, further enhances its appeal. Manufacturers are also innovating with packaging and formulation to cater to consumer preferences for organic and high-quality products. As culinary trends evolve, the ability of tomato puree to enrich flavors and enhance nutritional profiles positions it as a favored choice among chefs and home cooks alike, ensuring its robust market growth.

The food processing segment is projected to witness substantial growth over the forecast period, primarily due to the increasing demand for processed food products. As urbanization and busy lifestyles drive consumers toward convenience foods, food processors are turning to tomato pastes and purees as essential ingredients for a variety of products, including sauces, ready meals, and snacks. The versatility of tomato-based ingredients allows for enhanced flavors, nutritional benefits, and cost-effectiveness in product formulation. Additionally, the rising popularity of ethnic cuisines that incorporate tomato-based sauces—such as Italian and Mexican—further boosts demand in the food processing sector. Innovations in food preservation and processing techniques are also facilitating the incorporation of high-quality tomato pastes and purees into diverse applications, thereby supporting the growth of this segment. As the food processing industry continues to expand, the need for reliable, high-quality tomato ingredients is set to increase significantly.

The North American segment of the tomato pastes and purees market is expected to experience significant growth over the forecast period, driven by a combination of rising consumer demand for convenience foods and an expanding food service industry. As lifestyles become increasingly hectic, consumers are gravitating toward ready-to-use tomato products that facilitate quick meal preparation. Additionally, the popularity of Italian and Mediterranean cuisines, which heavily rely on tomato-based ingredients, is contributing to the growing market. North America is also seeing a shift toward health-conscious eating, with many consumers opting for organic and natural tomato products, further enhancing market prospects. The presence of major food manufacturers and a well-established distribution network in the region also play critical roles in driving growth. Furthermore, innovations in packaging and product quality are making tomato pastes and purees more accessible to a broader audience, positioning the North American segment for robust expansion in the coming years.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global Tomato Pastes and Purees Market is characterized by a mix of established players and emerging companies, each vying for market share through innovation, quality, and strategic partnerships. Major companies such as Conagra Brands, H.J. Heinz Company, and Del Monte Foods dominate the market, leveraging their extensive distribution networks and strong brand recognition. These companies are focusing on product diversification, introducing organic and specialty variants to cater to the increasing consumer demand for healthier options. Smaller, niche players are also gaining traction by emphasizing quality and artisanal production methods, appealing to health-conscious consumers and culinary enthusiasts. Additionally, collaborations with food service providers and retailers enhance market visibility and consumer access. As sustainability becomes a growing concern, many companies are adopting eco-friendly practices in sourcing and packaging, further differentiating their offerings. The market is expected to see ongoing competition as players strive to meet evolving consumer preferences and capitalize on emerging trends in the food industry.

Here are the major players in the Global Tomato Pastes and Purees Market:

Recent Development

Q1. What are the driving factors for the Global Tomato Pastes and Purees Market?

The Global Tomato Pastes and Purees Market is primarily driven by the increasing demand for processed food products, particularly in developing regions where urbanization and changing lifestyles are leading to higher consumption of convenience foods. The growing popularity of Italian cuisine, which heavily utilizes tomato-based products, has also bolstered market growth. Additionally, the rising awareness of health benefits associated with tomatoes, such as their antioxidant properties and rich nutrient profile, is encouraging consumers to incorporate tomato pastes and purees into their diets. The expansion of food service sectors, including restaurants and fast-food chains, further contributes to the demand for these products. Innovations in packaging and preservation techniques are enhancing product shelf life and quality, making tomato pastes and purees more appealing to consumers.

Q2. What are the restraining factors for the Global Tomato Pastes and Purees Market?

Despite the favorable growth prospects, the Global Tomato Pastes and Purees Market faces several challenges. Fluctuations in raw material prices, driven by climatic changes and agricultural practices, can affect production costs and pricing strategies. Moreover, the growing preference for fresh ingredients among health-conscious consumers may limit the appeal of processed tomato products. Regulatory challenges regarding food safety and quality standards can also pose hurdles for manufacturers, especially in emerging markets. Additionally, the presence of a wide variety of substitutes, such as fresh tomatoes and other sauces, can create stiff competition, potentially hindering market growth.

Q3. Which segment is projected to hold the largest share in the Market?

The canned tomato pastes segment is projected to hold the largest share in the Global Tomato Pastes and Purees Market. Canned products offer convenience and extended shelf life, making them a preferred choice among consumers and food manufacturers. The ability to maintain flavor and nutritional value during the canning process enhances their appeal in both household and commercial kitchens. This segment is further supported by increasing urbanization, which drives demand for quick and easy meal solutions, as well as the rising trend of meal preparation and cooking at home.

Q4. Which region holds the largest share in the Global Tomato Pastes and Purees Market?

North America is expected to hold the largest share of the Global Tomato Pastes and Purees Market. The region's robust food processing industry and high consumer demand for convenience foods contribute significantly to this growth. Additionally, the popularity of Italian cuisine, which frequently uses tomato-based products, supports sustained demand. The presence of major food companies and an established distribution network also facilitate market expansion in North America. Furthermore, health-conscious trends and the growing preference for organic and natural food products are encouraging consumers to choose tomato pastes and purees as healthier cooking alternatives.

Q5. Which are the prominent players in the Global Tomato Pastes and Purees Market?

Prominent Players in the Global Tomato Pastes and Purees Market

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model