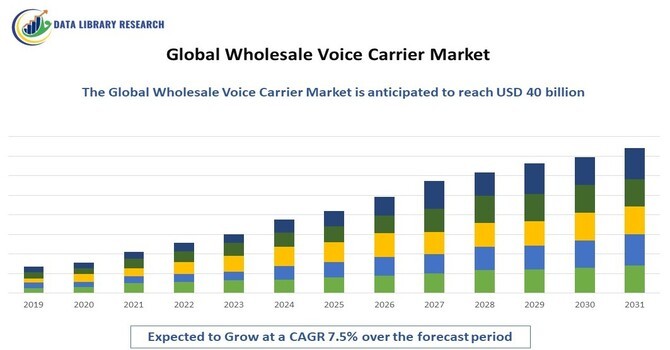

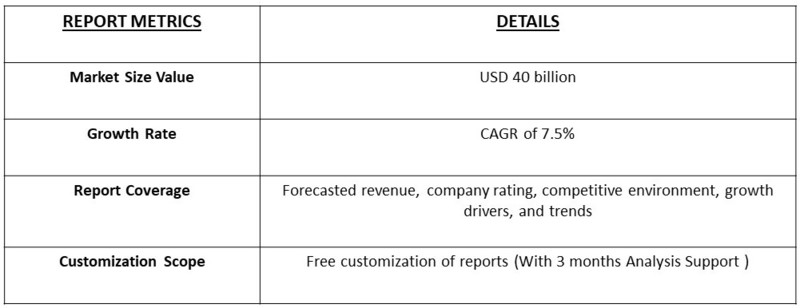

The global wholesale voice carrier market was valued at approximately $23 billion in 2023 and is projected to reach around $40 billion by 2031, representing a compound annual growth rate (CAGR) of about 7.5% from 2023 to 2031.

Get Complete Analysis Of The Report - Download Free Sample PDF

The wholesale voice carrier market is integral to the telecommunications landscape, acting as a backbone for voice services provided to enterprises and telecom operators worldwide. With the rise of VoIP technology, there's been a marked shift towards more efficient and cost-effective communication solutions. Businesses are increasingly adopting these technologies to enhance their voice service offerings, driven by the demand for high-quality calls and reliable connectivity. The surge in smartphone usage and internet penetration has also accelerated this trend, as users seek seamless voice communication.

Furthermore, the transition from traditional PSTN networks to IP-based systems allows for more efficient routing of voice traffic, significantly reducing costs and improving service quality. Emerging markets, supported by favorable regulatory environments and advancing infrastructure, are witnessing robust growth in this sector. This shift not only fosters competition among providers but also enhances service accessibility and reliability for end-users. As digital communication platforms continue to evolve, the wholesale voice carrier market is poised for sustained growth, adapting to the changing needs of a global audience.

Key trends are significantly shaping the wholesale voice carrier market, reflecting the industry's evolution in response to emerging technologies and customer demands. The rapid adoption of VoIP and cloud-based communication solutions stands out, as businesses increasingly leverage these technologies to enhance operational efficiency and cut costs. By migrating to cloud platforms, companies can scale their communication needs flexibly while accessing advanced features that traditional systems often lack. Quality of Service (QoS) and customer experience have become paramount, pushing carriers to invest in cutting-edge technologies that guarantee reliable and high-quality voice services. This focus on QoS is not only about call clarity but also about minimizing latency and enhancing overall user satisfaction.

Additionally, the convergence of voice and data services is prompting wholesale carriers to diversify their offerings. By integrating voice solutions with data services, carriers can provide comprehensive packages that meet the evolving needs of their clients, from unified communications to advanced analytics. Collaborative partnerships between carriers and technology providers are further driving innovation in the market. These collaborations enable the sharing of expertise and resources, fostering the development of new services and enhancing market competitiveness. As the landscape continues to shift, these trends are essential for carriers aiming to stay relevant and responsive to customer expectations.

Market Segmentation

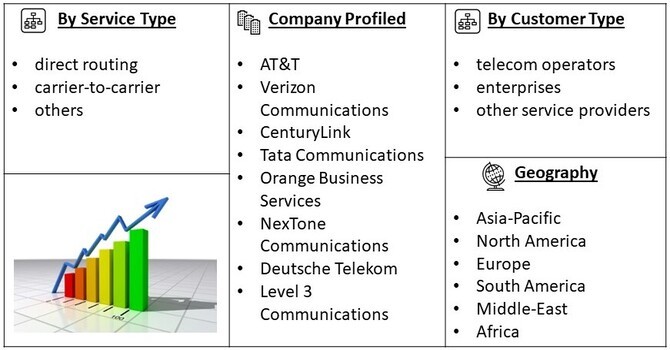

The global wholesale voice carrier market is segmented by service type (direct routing, carrier-to-carrier, and others), geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa), and customer type (telecom operators, enterprises, and other service providers). This segmentation offers insights into market dynamics, helping stakeholders identify opportunities for growth and development in specific areas.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers

The demand for reliable voice communication solutions is a key driver of growth in the wholesale voice carrier market. As businesses depend more on voice services for both internal collaboration and external client interactions, the need for high-quality, dependable communication channels has become critical. With voice remaining a fundamental aspect of business operations, organizations are increasingly seeking solutions that minimize downtime and ensure clear, uninterrupted conversations. The rise of remote work and digital communication has further amplified this need. As employees work from various locations, often using different devices, companies require a robust voice infrastructure that can seamlessly support diverse communication needs. This shift has led telecom operators to actively seek wholesale carriers that offer not only reliable services but also scalable solutions capable of adapting to fluctuating demands.

Moreover, the focus on integrating voice with other digital communication tools—like video conferencing and instant messaging—has become essential. Carriers that can provide comprehensive voice solutions within a unified communications framework are particularly attractive to businesses aiming to enhance productivity and maintain effective communication.

In this evolving landscape, wholesale carriers must prioritize service reliability and quality to meet the escalating expectations of enterprises. This trend underscores the importance of investing in advanced technologies and infrastructure that can support the increasing complexity and volume of voice communications, ultimately fostering greater business agility and resilience.

Technological advancements in VoIP solutions are fundamentally transforming the wholesale voice carrier market. Innovations in call quality—such as HD voice and enhanced audio codecs—are making VoIP an increasingly appealing alternative to traditional telephony. These improvements ensure clearer, more reliable conversations, which are essential for businesses that depend on effective communication for customer interactions and internal collaboration. Reduced latency is another significant advancement that enhances the user experience. Lower delays in voice transmission lead to more natural conversations, critical in environments where real-time communication is essential. Additionally, cost-effective routing options, enabled by IP-based networks, allow carriers to optimize traffic management, significantly lowering costs for both providers and end-users. This financial efficiency is particularly attractive to businesses looking to cut operational expenses without compromising service quality.

The shift toward IP-based networks has also ushered in greater flexibility and scalability in voice solutions. Carriers can now offer customizable packages that adapt to the specific needs of businesses, allowing them to scale services up or down as required. This agility is crucial in today’s fast-paced market, where business needs can change rapidly.

As businesses become more familiar with the numerous benefits of VoIP—such as integration with other digital communication tools, enhanced mobility, and advanced features like voicemail-to-email and call analytics—adoption rates continue to soar. This growing acceptance is driving further investment in VoIP technologies, which in turn fuels market expansion. Overall, these technological advancements position VoIP as a transformative force in the wholesale voice carrier market, reshaping how voice services are delivered and consumed.

Market Restraints

One significant market restraint for the wholesale voice carrier market is the intense competition and price pressure among providers. As more players enter the market, especially with the rise of VoIP technology, carriers are compelled to offer increasingly competitive pricing to attract and retain customers. This race to the bottom can lead to diminished profit margins, making it challenging for carriers to invest in the necessary infrastructure and technology enhancements needed to improve service quality. Additionally, the proliferation of low-cost communication solutions can make it difficult for traditional carriers to differentiate themselves, further intensifying the competitive landscape.

Furthermore, the reliance on third-party providers for certain technological components can create vulnerabilities in service delivery and affect overall reliability. As customer expectations for quality and uptime rise, carriers must balance competitive pricing with the need to maintain high standards of service. This delicate equilibrium presents a significant challenge, potentially limiting growth opportunities and innovation within the wholesale voice carrier market.

The COVID-19 pandemic significantly influenced the wholesale voice carrier market, creating both challenges and opportunities. As organizations rapidly shifted to remote work environments, the demand for reliable voice services surged. Companies found themselves relying heavily on voice communication for daily operations, client interactions, and team collaboration, which resulted in increased traffic volumes across networks. This sudden spike in demand translated into higher revenues for wholesale carriers, who played a crucial role in supporting the increased need for connectivity. The pandemic acted as a catalyst for digital transformation across industries. Many organizations turned to cloud-based solutions to facilitate communication and collaboration, recognizing that traditional infrastructure was inadequate for the new remote work paradigm. This shift led to a growing interest in VoIP and other digital communication tools, prompting wholesale carriers to enhance their service offerings and ensure they could accommodate this increased usage.

While the pandemic did introduce some disruptions—such as network congestion and challenges in service delivery—the overall trend was one of resilience and recovery. Businesses began to understand the critical importance of a robust communication infrastructure, leading to renewed investments in voice services and technology. As the world adjusted to the realities of hybrid and remote work models, the demand for high-quality, scalable voice solutions became evident.

In the aftermath of the pandemic, many businesses are now better equipped to handle future disruptions, having recognized that strong communication capabilities are essential for operational continuity. This awareness is expected to sustain the momentum in the wholesale voice carrier market, as organizations continue to prioritize reliable voice services as a cornerstone of their communication strategies.

Segmental Analysis

The direct routing segment is poised to capture a significant share of the wholesale voice carrier market, largely due to the growing preference among telecom operators and enterprises for establishing direct connections. This approach significantly reduces the risk of call quality degradation that can occur when voice traffic passes through multiple intermediary routes. By minimizing hops and potential bottlenecks, direct routing ensures clearer, more reliable voice communications, which is critical for businesses that rely on high-quality interactions with clients and partners.

Moreover, enhanced security and greater control over voice traffic are vital considerations for organizations handling sensitive information. Direct routing provides businesses with the ability to manage their voice communications more effectively, enabling them to implement robust security measures and maintain compliance with regulatory standards. This level of control is increasingly important as cyber threats continue to evolve, prompting companies to seek solutions that can safeguard their communication channels.

As more organizations become aware of these advantages, the demand for direct routing is expected to rise, driving substantial growth in this segment. Companies are recognizing that investing in direct routing not only improves call quality but also enhances their overall communication infrastructure, leading to better operational efficiency and customer satisfaction. This trend underscores a shift towards more streamlined, secure, and high-performance voice solutions, positioning the direct routing segment as a key player in the wholesale voice carrier market's future.

The telecom operators segment is set to dominate the wholesale voice carrier market, primarily due to their pivotal role within the broader telecommunications ecosystem. As the main service providers, telecom operators are tasked with delivering high-quality voice solutions to a diverse customer base, including both residential and business clients. This essential function drives the demand for reliable and scalable voice services, as operators must ensure seamless communication experiences to meet customer expectations. The increasing competition within the telecom industry further propels operators to seek innovative solutions that enhance service delivery and improve customer satisfaction. In a saturated market, distinguishing themselves through superior voice quality, advanced features, and efficient service delivery is crucial for operators aiming to retain and grow their customer base. This has led many to explore wholesale voice services as a means to bolster their offerings and maintain competitive advantages.

Additionally, the rise in mobile subscribers and the growth of international traffic are significant factors fueling demand for wholesale voice services. As mobile connectivity becomes more ubiquitous and global communication needs expand, telecom operators are finding it essential to partner with wholesale carriers to manage the increasing volume of voice traffic efficiently. This partnership not only facilitates better routing and cost management but also allows operators to offer comprehensive, high-quality services that cater to the evolving demands of their customers.

As a result, the telecom operators segment is well-positioned for substantial growth, driven by the dual imperatives of enhancing service quality and adapting to the dynamic telecommunications landscape. This growth trajectory highlights the integral role of wholesale voice services in empowering telecom operators to meet contemporary communication challenges effectively.

Regional Analysis

North America is expected to maintain a dominant position in the global wholesale voice carrier market, driven by a combination of advanced infrastructure, high adoption rates of VoIP technologies, and robust demand for voice services. The region's telecommunications infrastructure is among the most sophisticated in the world, enabling seamless connectivity and high-quality service delivery. This strong foundation supports the increasing use of VoIP, which has become a standard for both businesses and consumers seeking reliable and cost-effective voice solutions.

Moreover, North America is home to several leading telecom operators and wholesale carriers, which play a crucial role in driving market innovation and service diversification. These key players are continually exploring new technologies and approaches to enhance their offerings, ensuring they meet the evolving needs of their customers. As the emphasis on high-quality voice services intensifies, these operators are investing in advanced solutions that prioritize clarity and reliability, further bolstering market growth.

The transition to cloud-based solutions is another significant factor supporting the wholesale voice carrier market in North America. As businesses increasingly adopt cloud technologies for greater flexibility and scalability, the demand for integrated voice solutions that complement these systems is rising. This shift not only enhances operational efficiency but also fosters a more dynamic communication environment. Additionally, favorable regulatory policies in the region encourage competition and innovation, creating a conducive environment for growth. Investments in next-generation technologies, such as 5G and enhanced fiber-optic networks, further enhance the competitive landscape, allowing carriers to deliver faster, more reliable services. Together, these factors position North America as a leader in the wholesale voice carrier market, setting the stage for continued expansion and innovation in the years to come.

To Learn More About This Report - Request a Free Sample Copy

The wholesale voice carrier market is characterized by a number of prominent players, including industry giants like AT&T, Verizon Communications, CenturyLink, Tata Communications, and Orange Business Services. These companies play a critical role in shaping the market landscape, focusing on innovation and the continuous expansion of their service portfolios. By leveraging their extensive networks and resources, these established firms aim to enhance their market presence and meet the diverse needs of their customers. To maintain a competitive edge, these leading players prioritize strategic collaborations and partnerships. By teaming up with technology providers, software developers, and other telecom companies, they can introduce cutting-edge solutions and expand their service offerings, ensuring they remain relevant in a rapidly evolving industry. This collaborative approach also allows for the sharing of expertise and resources, which is essential for developing advanced voice carrier technologies.

Emerging players are increasingly entering the market, contributing to heightened competition and driving advancements in voice communication solutions. These newcomers often bring innovative ideas and agile business models that challenge traditional approaches, prompting established companies to adapt and innovate in response. This dynamic environment fosters a spirit of continuous improvement and encourages all players to enhance their service quality and customer experience.

Research and development (R&D) initiatives are central to the competitive strategies of leading firms. These companies invest significantly in R&D to explore new technologies, improve voice clarity, reduce latency, and enhance overall service reliability. By focusing on innovations that enhance user experience, they can better meet customer demands and address the complexities of modern communication needs.

In summary, the wholesale voice carrier market is marked by a blend of established giants and emerging challengers, all of whom are committed to innovation, collaboration, and the pursuit of excellence in service delivery. This competitive landscape not only drives advancements in technology but also ensures that customers benefit from increasingly sophisticated and reliable voice communication solutions.

Key Players:

Recent Developments

Q1. What are the driving factors for the Global Wholesale Voice Carrier Market?

The global wholesale voice carrier market is experiencing significant growth, driven by several key factors. One of the primary drivers is the increasing demand for high-quality voice services. As businesses and consumers alike prioritize clear and reliable communication, there is a pressing need for voice solutions that minimize call drops, reduce latency, and enhance overall audio quality. This focus on quality has led many organizations to seek out wholesale carriers that can provide superior service and support.

Q2. What are the restraining factors for the Global Wholesale Voice Carrier Market?

Despite the growth potential of the wholesale voice carrier market, several challenges pose significant obstacles to its expansion. One major issue is the presence of regulatory hurdles, which can vary significantly across regions. Compliance with diverse regulations concerning privacy, security, and telecommunications can complicate operations for wholesale carriers, particularly those operating in multiple jurisdictions. Navigating these regulatory landscapes often requires substantial resources and expertise, which can slow down the pace of market entry and innovation.

Q3. Which segment is projected to hold the largest share in the Global Wholesale Voice Carrier Market?

The direct routing segment is expected to dominate the global wholesale voice carrier market, primarily because it offers significant advantages in terms of call quality, security, and control over voice traffic. By enabling direct connections between telecom operators and enterprises, this approach minimizes the number of intermediaries involved in the communication process. This reduction in intermediaries not only decreases latency but also enhances call clarity and reliability, which are critical factors for businesses that depend on high-quality voice communication.

Q4. Which region holds the largest share of the Global Wholesale Voice Carrier Market?

North America is poised to hold the largest share of the global wholesale voice carrier market, fueled by several key factors that highlight its leadership in the telecommunications sector. One of the most significant drivers is the region's advanced telecommunications infrastructure. North America boasts a well-developed network of fiber-optic lines, data centers, and switching facilities, enabling high-capacity and reliable voice communication services. This robust infrastructure supports the increasing demand for high-quality voice services, positioning the region as a preferred hub for both providers and consumers.

Q5. Which are the prominent players in the Global Wholesale Voice Carrier Market?

The global wholesale voice carrier market is home to several prominent players, including AT&T, Verizon Communications, CenturyLink, Tata Communications, and Orange Business Services. These companies are at the forefront of the industry, leveraging their extensive networks and resources to provide a wide range of voice communication solutions tailored to meet the diverse needs of their customers. AT&T and Verizon Communications, as two of the largest telecommunications companies in North America, are heavily invested in enhancing their service offerings. They focus on innovation through the integration of advanced technologies, such as cloud-based solutions and VoIP, enabling businesses to optimize their communication strategies. Their comprehensive portfolios not only include traditional voice services but also encompass value-added features like analytics, call management, and unified communications, ensuring they remain competitive in a rapidly evolving market.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model