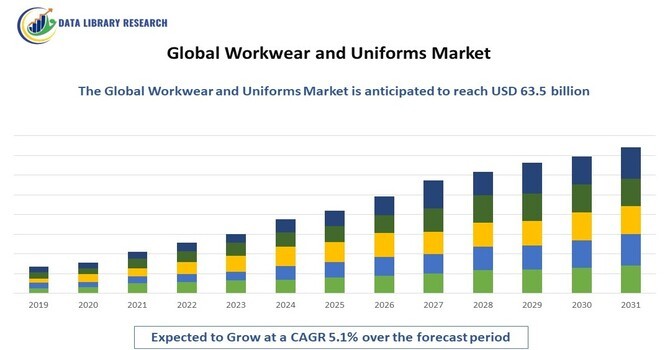

The global workwear and uniforms market is projected to reach a market value of USD 43.3 billion in 2023 and is expected to grow to USD 63.5 billion by 2031, registering a Compound Annual Growth Rate (CAGR) of 5.1% during the forecast period, 2023-2031.

Get a Complete Analysis Of The Report - Download a Free Sample PDF

The Global Workwear and Uniforms Market encompasses the production, distribution, and sale of specialized clothing designed for various professional environments, including industrial, service, and healthcare sectors. This market includes a range of products such as safety workwear, corporate uniforms, and specialized apparel tailored for specific job functions and industry standards. Growth is driven by increasing regulatory requirements for workplace safety, the rising demand for branded and standardized corporate attire, and advancements in fabric technology for enhanced comfort and durability. The market is supported by trends toward customization, sustainability, and functional design innovations.

The Global Workwear and Uniforms Market is driven by several key factors. Increasing regulatory requirements for workplace safety are prompting organizations to invest in compliant workwear solutions. The demand for branded and standardized corporate uniforms is rising as companies seek to enhance brand identity and employee professionalism. Technological advancements in fabric and garment manufacturing are improving comfort, durability, and functionality of workwear. Additionally, the growing emphasis on sustainability and eco-friendly materials is influencing market dynamics, as companies adopt more environmentally responsible practices. These factors collectively contribute to the robust growth of the workwear and uniforms sector.

The Global Workwear and Uniforms Market include a growing focus on sustainability, with increasing adoption of eco-friendly materials and manufacturing processes. There is also a rising demand for smart workwear incorporating wearable technology for improved safety and efficiency. Customization and personalization are becoming more prevalent, allowing companies to tailor uniforms to specific brand identities and employee needs. The market is seeing a shift towards multifunctional and ergonomic designs that enhance comfort and performance. Additionally, the integration of digital platforms for uniform management and ordering is streamlining procurement processes and improving supply chain efficiency.

Market Segmentation: The Global Workwear and Uniforms Market is segmented by technology Type of Workwear (Safety Workwear, Corporate Uniforms, Healthcare Uniforms, Industrial Workwear, Hospitality Uniforms) End-User Industry (Construction, Construction, Healthcare, Retail, Hospitality) and geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report offers the market size and forecasts for revenue (USD million) for all the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

Growing demand for high-quality workwear:

The global workwear and uniforms market is driven by the growing demand for high-quality workwear that meets the needs of workers in various industries. Consumers are seeking durable, comfortable, and functional workwear that can withstand the rigors of their daily tasks. For instance, a leading workwear manufacturer has reported a 15% increase in sales of high-quality workwear in the past year, driven by consumer demand for premium products. This trend is expected to continue, driving demand for high-quality workwear and uniforms. As a result, the market is expected to see increased investment in research and development, as well as marketing and distribution efforts.

Increasing adoption of sustainable workwear:

The global workwear and uniforms market is driven by the growing demand for high-quality workwear that meets the needs of workers in various industries. Consumers are seeking durable, comfortable, and functional workwear that can withstand the rigors of their daily tasks. For instance, a leading workwear manufacturer has reported a 15% increase in sales of high-quality workwear in the past year, driven by consumer demand for premium products. This trend is expected to continue, driving demand for high-quality workwear and uniforms. As a result, the market is expected to see increased investment in research and development, as well as marketing and distribution efforts.

Market Restraints:

The global workwear and uniforms market is restrained by high production costs. The production of workwear and uniforms requires significant investments in materials, labor, and equipment, which can be a barrier to entry for new manufacturers. Additionally, the cost of sourcing high-quality materials, such as cotton and polyester, can be high. For instance, a leading workwear manufacturer has reported that the cost of producing a single workwear item can range from 5 to 15, which can make it challenging to maintain profitability. This high production cost can be a significant restraint on the market, limiting the ability of manufacturers to invest in research and development, marketing, and distribution. As a result, the market is expected to be characterized by a focus on efficiency and cost reduction.

The COVID-19 pandemic significantly impacted the Global Workwear and Uniforms Market, initially disrupting supply chains and causing delays in production and distribution. The pandemic accelerated the need for healthcare uniforms, including personal protective equipment (PPE), as frontline workers required enhanced protection. Concurrently, many businesses reduced their uniform purchases due to operational shutdowns and remote work arrangements, leading to a temporary decline in demand. However, as economies reopened and safety regulations evolved, there was a resurgence in demand for workwear across various sectors, particularly for hygiene and safety-related products. The market adapted by incorporating new safety features into uniforms and increasing the use of digital platforms for uniform management and procurement, driving a rebound in growth.

Segmental Analysis:

Safety Workwear Segment is Expected to Witness Significant Growth Over the Forecast Period

The automatic wash systems segment in the Global Car Washing Market has seen significant advancements with the introduction of sophisticated tunnel washers, conveyor systems, and robotic washers. These systems are designed to provide efficient, high-throughput washing solutions that cater to both individual and fleet needs. Recent developments include the integration of smart technology, which allows for real-time monitoring and automated adjustments to optimize wash quality and resource usage. The driving factors for this segment include increasing consumer demand for convenience, the desire for consistent and high-quality wash results, and the efficiency of automated systems in reducing labor costs and time. Additionally, technological innovations such as touchless and hybrid wash systems are enhancing customer satisfaction by minimizing vehicle damage and improving overall wash performance.

Healthcare Uniforms Segment is Expected to Witness Significant Growth Over the Forecast Period

Healthcare uniforms have seen significant innovation and demand growth, driven by the global focus on infection control and hygiene in medical settings. In 2024, companies like Barco Uniforms and FIGS launched new lines of antimicrobial scrubs and lab coats designed to enhance durability and comfort while providing enhanced protection against pathogens. The driving factors for this sub-segment include the ongoing global health crises, increased awareness of hygiene standards, and the need for comfortable, functional attire for medical professionals. Advances in fabric technology and a growing emphasis on healthcare worker well-being contribute to the expansion of this segment within the workwear market.

Asia Pacific Region is Expected to Witness Significant Growth Over the Forecast Period

The Asia-Pacific region is projected to experience significant growth in the workwear and uniforms market over the forecast period. This growth is driven by rapid industrialization and urbanization in key markets like China, India, and Southeast Asia, which are increasing the demand for both industrial and corporate workwear. Additionally, stringent safety regulations and rising standards for employee attire across various industries are contributing to market expansion. The growing middle class and rising disposable incomes in the region are leading to greater spending on quality workwear and uniforms. Furthermore, the development of retail and distribution networks, including the expansion of e-commerce platforms, is enhancing accessibility and driving market growth.

To Learn More About This Report - Request a Free Sample Copy

The Global Workwear and Uniforms Market is characterized by a diverse range of key players focused on innovation, brand differentiation, and market expansion. Companies are investing in advanced materials, technology, and customization to meet the evolving needs of various industries.

Leading competitors include:

Recent Development:

1) In 2023, VF Corporation launched a new line of eco-friendly workwear under its Dickies brand, focusing on sustainability and reducing environmental impact. This product line features garments made from recycled materials and incorporates advanced, environmentally responsible manufacturing processes. The initiative reflects VF Corporation’s commitment to sustainability and responds to the increasing demand for eco-conscious workwear solutions. The new line aims to cater to companies and organizations looking to enhance their corporate social responsibility and reduce their carbon footprint.

2) In early 2024, Cintas Corporation unveiled a new range of smart workwear integrating wearable technology. These garments include embedded sensors that monitor workers' vital signs and environmental conditions, providing real-time safety alerts and health data. This development aims to enhance worker safety and productivity, particularly in high-risk industries. By leveraging advancements in wearable technology, Cintas is positioning itself as a leader in the innovation of workwear, addressing growing concerns about occupational health and safety.

Q1. What are the driving factors for the Global Workwear and Uniform Market?

The global workwear and uniform market is primarily driven by the increasing demand for corporate branding and employee identification across various industries. Companies recognize that uniforms can enhance brand visibility and create a professional image, which is particularly important in sectors like hospitality, healthcare, and retail. Additionally, the focus on employee safety and comfort is prompting organizations to invest in high-quality, functional workwear that complies with safety regulations. The growth of e-commerce platforms has also made it easier for businesses to source customized uniforms. Moreover, the rising trend of remote work is influencing organizations to rethink their uniform policies, leading to a demand for more versatile workwear options.

Q2. What are the restraining factors for the Global Workwear and Uniform Market?

Despite its growth potential, the global workwear and uniform market faces several restraining factors. One of the main challenges is the high cost associated with sourcing high-quality materials and custom designs, which can deter smaller businesses from investing in uniforms. Additionally, the market is susceptible to fluctuations in raw material prices, affecting overall production costs. The increasing preference for casual wear in some workplaces may also reduce the demand for traditional uniforms. Furthermore, the lack of standardization in sizing and design can create challenges for manufacturers and customers alike. Finally, economic downturns can lead businesses to cut costs, including expenditures on workwear.

Q3. Which segment is projected to hold the largest share in the Global Workwear and Uniform Market?

The protective clothing segment is projected to hold the largest share in the global workwear and uniform market. This segment includes garments designed to ensure worker safety in hazardous environments, such as construction, manufacturing, and healthcare settings. The rising awareness of occupational safety and health regulations is driving demand for protective workwear, as companies seek to comply with legal requirements and protect their employees. Furthermore, innovations in fabric technology are enhancing the functionality and comfort of protective clothing, making it more appealing to businesses. As safety regulations become increasingly stringent, the protective clothing segment is expected to continue dominating the market.

Q4. Which region holds the largest share in the Global Workwear and Uniform Market?

North America is anticipated to hold the largest share in the global workwear and uniform market, primarily driven by the region's robust industrial sector and stringent safety regulations. The United States, in particular, has a strong demand for workwear across various industries, including construction, manufacturing, and healthcare. The increasing focus on employee safety and corporate branding further propels the demand for uniforms in North America. Additionally, the presence of key players and established supply chains enhances market accessibility. As companies increasingly invest in employee identity and safety measures, North America is well-positioned to maintain its leading position in the workwear and uniform market.

Q5. Which are the prominent players in the Global Workwear and Uniform Market?

Prominent players in the global workwear and uniform market include well-established companies such as Aramark, Cintas Corporation, and VF Corporation. These companies are recognized for their extensive range of workwear solutions and commitment to quality. Additionally, firms like Dickies, Carhartt, and Engelbert Strauss have gained significant market presence by focusing on specific sectors and offering durable, functional products. These players are actively investing in innovation and sustainability initiatives to cater to evolving consumer preferences. Collaborations with businesses for custom uniform solutions further enhance their market positions, allowing them to adapt to diverse industry needs.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model